Will Leadership Transition and CFO Accolades Change CACI International's (CACI) Capital Allocation Narrative?

CACI International Inc Class A CACI | 0.00 |

- CACI International recently reported that President, U.S. Operations DeEtte Gray plans to retire at the end of 2026 after serving as a Strategic Advisor for the second half of the year to support a smooth leadership handover.

- At the same time, CFO Jeffrey MacLauchlan’s dual “CFO of the Year” awards are drawing fresh attention to how CACI’s finance function underpins disciplined capital allocation and acquisition execution.

- We’ll now examine how MacLauchlan’s external recognition for financial discipline and deal execution may influence CACI’s existing investment narrative.

We've uncovered the 9 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

CACI International Investment Narrative Recap

To own CACI, you have to believe its deep ties to U.S. national security customers and tech-focused contract wins will keep converting into resilient earnings, despite budget and procurement volatility. The recent leadership news is directionally reassuring rather than transformational: DeEtte Gray’s planned retirement includes a built-in transition period, while Jeffrey MacLauchlan’s finance awards underscore capital discipline. Neither appears to materially change the near term catalyst around contract execution or the key risk of government spending disruption.

The most relevant recent development is MacLauchlan’s dual “CFO of the Year” recognition for 2025, which spotlights his role in executing the ARKA Group acquisition and reinforcing CACI’s balance sheet. That matters for today’s catalysts, because acquisitions, debt-funded or otherwise, are central to CACI’s push into higher value space and electronic warfare work, even as investors weigh the existing risks from heavy federal exposure and potential contract delays.

Yet against this strength, investors should be aware that CACI’s dependence on U.S. government budgets means any prolonged spending squeeze could...

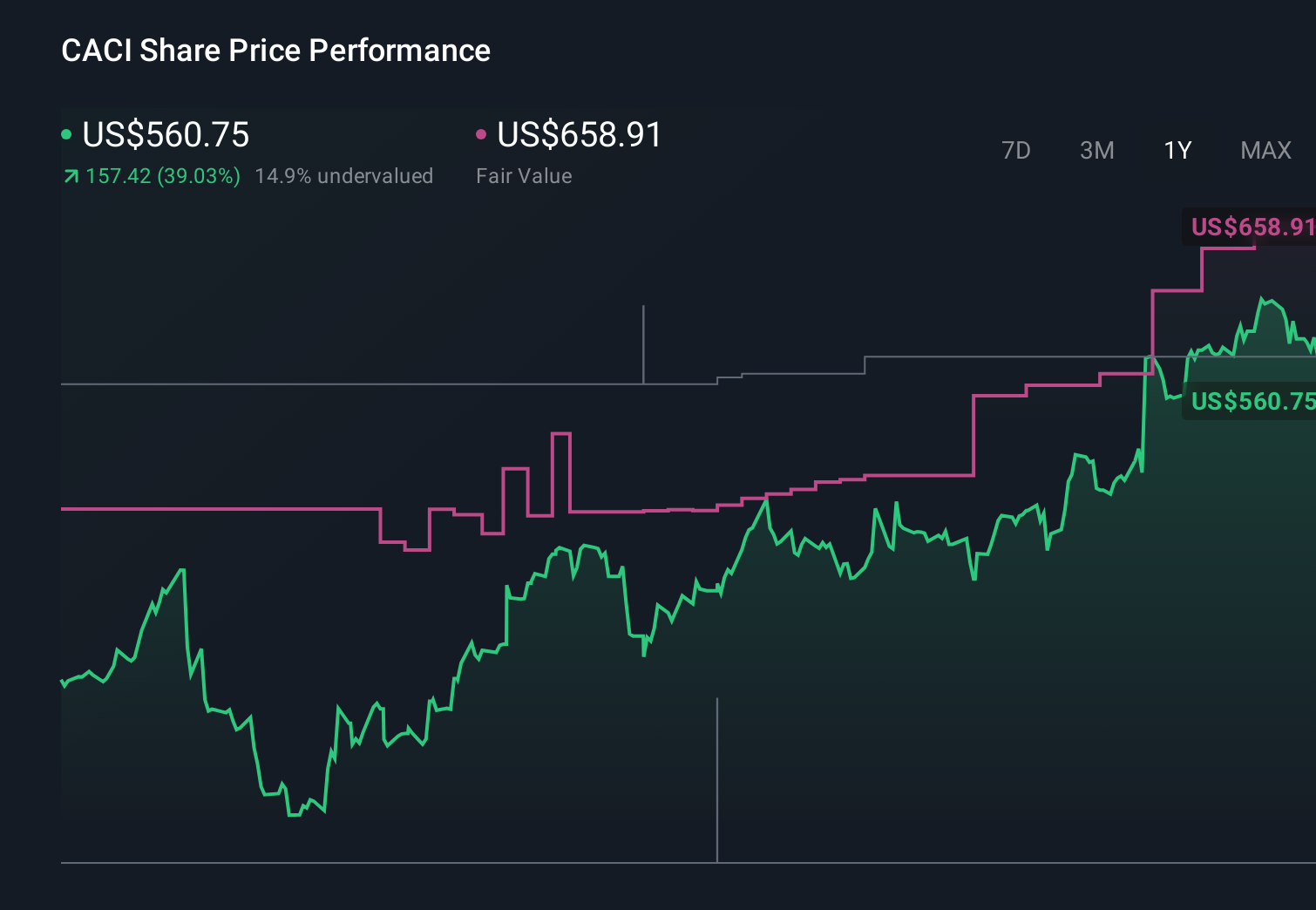

CACI International's narrative projects $11.9 billion revenue and $744.0 million earnings by 2029. This requires 10.0% yearly revenue growth and about a $225.6 million earnings increase from $518.4 million today.

Uncover how CACI International's forecasts yield a $709.23 fair value, a 33% upside to its current price.

Exploring Other Perspectives

Some of the most optimistic analysts already expected CACI to reach about US$12.9 billion in revenue and roughly US$746.8 million in earnings, yet this fresh spotlight on MacLauchlan’s capital discipline may either reinforce that upbeat view or prompt you to question it, especially if you worry that growing reliance on commercial off the shelf solutions could cap the upside they are banking on.

Explore 3 other fair value estimates on CACI International - why the stock might be worth as much as 89% more than the current price!

Form Your Own Verdict

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your CACI International research is our analysis highlighting 4 key rewards and 1 important warning sign that could impact your investment decision.

- Our free CACI International research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate CACI International's overall financial health at a glance.

Looking For Alternative Opportunities?

These stocks are moving-our analysis flagged them today. Act fast before the price catches up:

- Outshine the giants: these 13 early-stage AI stocks could fund your retirement.

- Invest in the nuclear renaissance through our list of 88 elite nuclear energy infrastructure plays powering the global AI revolution.

- AI is about to change healthcare. These 39 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.