Will Leadership Transition And Extended Credit Facility Maturity Change W. R. Berkley’s (WRB) Narrative?

W. R. Berkley Corporation WRB | 0.00 |

- W. R. Berkley Corporation recently extended the maturity of its revolving credit facility to June 9, 2031, while also announcing leadership changes following the passing of founder and Executive Chairman William R. Berkley and appointing W. Robert Berkley, Jr. as Chairman and Kirk A. Parker as president of Berkley North Pacific.

- These developments highlight both continuity in the company’s long-standing leadership framework and an effort to reinforce operational depth across its commercial insurance platforms.

- We’ll now examine how the founder’s passing and consolidation of leadership under W. Robert Berkley, Jr. may influence W. R. Berkley’s investment narrative.

Uncover the next big thing with 24 elite penny stocks that balance risk and reward.

W. R. Berkley Investment Narrative Recap

To own W. R. Berkley, you need to believe in its specialty commercial insurance franchise, disciplined underwriting and careful capital management. The founder’s passing and leadership consolidation under W. Robert Berkley, Jr. introduce governance and execution questions, but the long-tenured management team and extended credit facility do not appear to materially alter the near term earnings catalyst or the core risk around competitive pressure and underwriting discipline.

The extension of the revolving credit facility to June 9, 2031 is the most relevant announcement here, as it underpins liquidity while the company absorbs leadership changes. This added funding visibility may help support ongoing share repurchases and organic initiatives that tie directly into underwriting income and investment returns, even as investors weigh risks from rising catastrophe exposure and intense competition in property and MGA driven markets.

Yet even with this stability, investors should be aware that underwriting discipline could come under pressure if competition and catastrophe trends begin to...

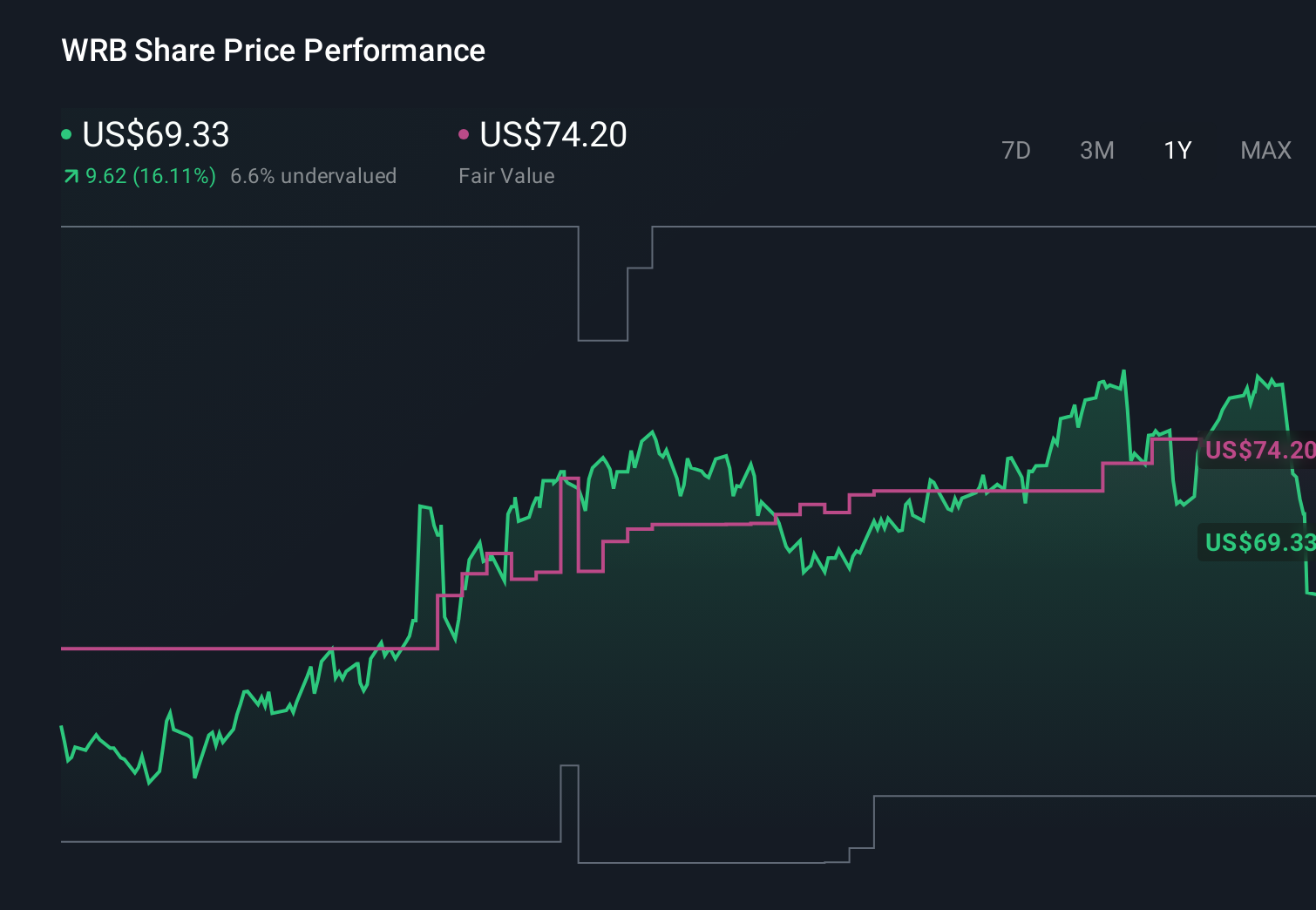

W. R. Berkley's narrative projects $14.3 billion revenue and $2.0 billion earnings by 2028. This requires 0.0% yearly revenue growth and about a $0.2 billion earnings increase from $1.8 billion today.

Uncover how W. R. Berkley's forecasts yield a $68.33 fair value, in line with its current price.

Exploring Other Perspectives

Some of the most optimistic analysts were assuming earnings could reach about US$2.1 billion by 2029, yet the recent leadership transition and credit extension may cause that upbeat view on climate and catastrophe risk to be reassessed, so it is worth comparing these bullish expectations with more cautious scenarios before deciding which story you believe.

Explore 3 other fair value estimates on W. R. Berkley - why the stock might be worth as much as 77% more than the current price!

The Verdict Is Yours

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your W. R. Berkley research is our analysis highlighting 2 key rewards and 1 important warning sign that could impact your investment decision.

- Our free W. R. Berkley research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate W. R. Berkley's overall financial health at a glance.

Interested In Other Possibilities?

The market won't wait. These fast-moving stocks are hot now. Grab the list before they run:

- Capitalize on the AI infrastructure supercycle with our selection of the 49 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

- We've uncovered the 7 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

- Invest in the nuclear renaissance through our list of 89 elite nuclear energy infrastructure plays powering the global AI revolution.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.