Will Marine Systems Strength and New Defense Wins Change General Dynamics' (GD) Narrative?

General Dynamics Corporation GD | 0.00 |

- In recent weeks, General Dynamics reported Q1 2026 results showing revenue growth across all four segments, with Marine Systems leading operating earnings growth and a consolidated book-to-bill ratio of 2-to-1 on US$26.60 billion of orders.

- The company also announced new defense wins and partnerships, including a US$229.65 million Stryker vehicle contract and a collaboration with Kodiak AI on autonomous ground systems, underscoring demand for both traditional and emerging platforms.

- Now we will examine how strong Marine Systems earnings and order intake may influence General Dynamics’ existing investment narrative and outlook.

Invest in the nuclear renaissance through our list of 88 elite nuclear energy infrastructure plays powering the global AI revolution.

General Dynamics Investment Narrative Recap

To own General Dynamics, you need to believe in its ability to convert a large, long-cycle defense and aerospace backlog into consistent earnings while managing execution and balance sheet pressures. The Q1 2026 results, with Marine Systems leading operating earnings growth and a 2-to-1 book-to-bill on US$26.60 billion of orders, reinforce the near term catalyst around backlog conversion, but do not materially change the key risk around supply chain and shipyard execution in Marine.

The Marine Systems outperformance in Q1 2026 is the most relevant update, because it directly links to the core catalyst of multi year submarine and shipbuilding programs supported by U.S. Navy funding and industrial base investments. Improved shipyard performance and higher Marine earnings suggest that, for now, operational initiatives are supporting throughput and margins, which matters for how investors weigh the sizable backlog against ongoing concerns about delays, quality issues, and cost inflation in the defense supply chain.

Yet, even with these solid Marine results, investors should be aware that persistent supply chain fragility and shipyard disruptions could still...

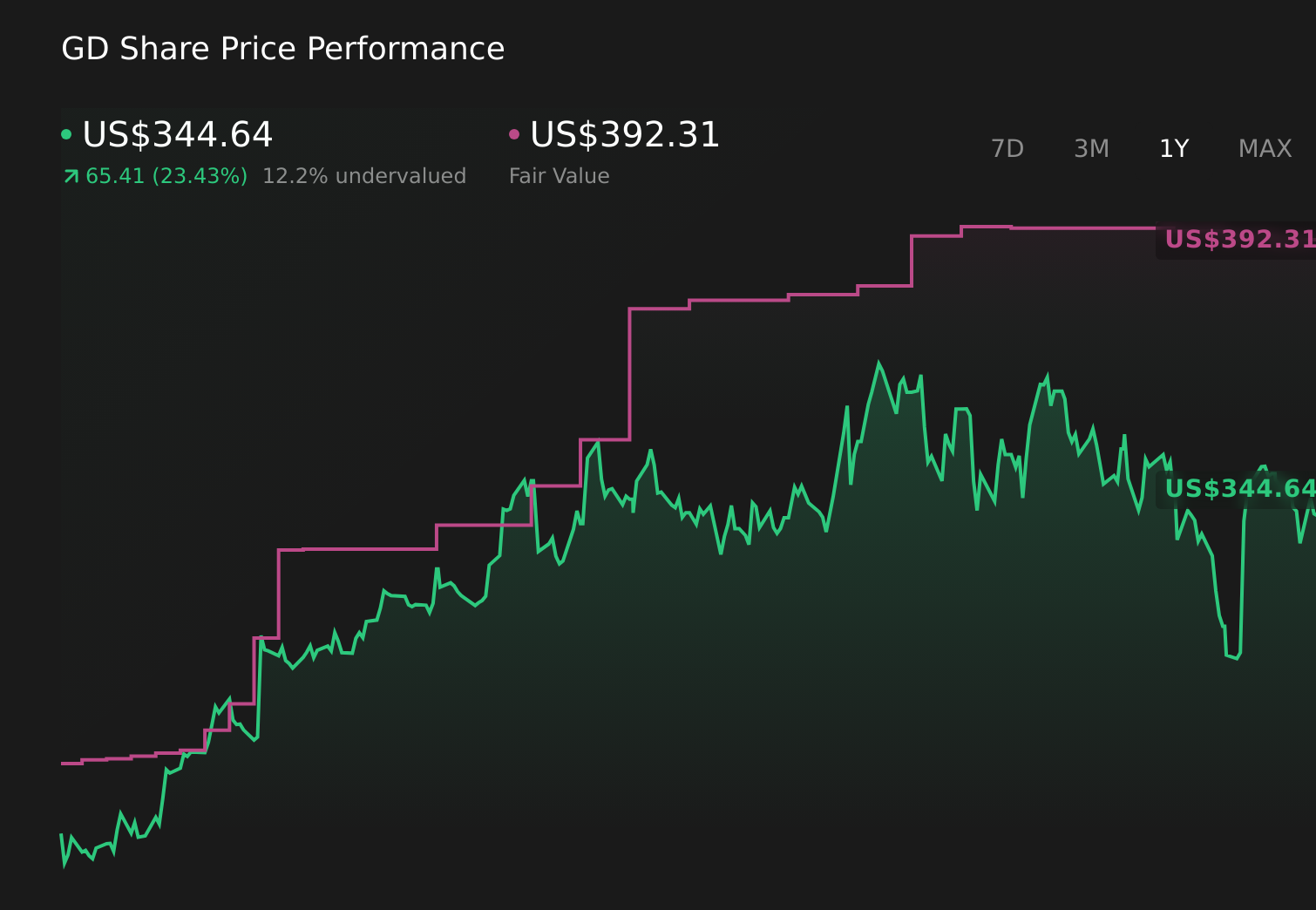

General Dynamics' narrative projects $60.7 billion revenue and $5.4 billion earnings by 2029. This requires 4.1% yearly revenue growth and a $1.1 billion earnings increase from $4.3 billion today.

Uncover how General Dynamics' forecasts yield a $392.31 fair value, a 15% upside to its current price.

Exploring Other Perspectives

Four fair value estimates from the Simply Wall St Community cluster between US$391.55 and about US$409.68, showing how differently individual investors assess upside. You should weigh these views against the central catalyst that Marine Systems backlog conversion and shipyard execution remain critical swing factors for General Dynamics’ future performance.

Explore 4 other fair value estimates on General Dynamics - why the stock might be worth as much as 20% more than the current price!

The Verdict Is Yours

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your General Dynamics research is our analysis highlighting 5 key rewards and 1 important warning sign that could impact your investment decision.

- Our free General Dynamics research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate General Dynamics' overall financial health at a glance.

No Opportunity In General Dynamics?

Early movers are already taking notice. See the stocks they're targeting before they've flown the coop:

- Capitalize on the AI infrastructure supercycle with our selection of the 43 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

- Find 54 companies with promising cash flow potential yet trading below their fair value.

- This technology could replace computers: discover 26 stocks that are working to make quantum computing a reality.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.