Will Positive Phase 2b Hepatitis Delta Data for Brelovitug Change Mirum Pharmaceuticals' (MIRM) Narrative

Mirum Pharmaceuticals MIRM | 0.00 |

- Mirum Pharmaceuticals recently reported that the Phase 2b portion of its AZURE-1 study of brelovitug in chronic hepatitis delta virus met its primary endpoint, with 24-week data showing strong antiviral activity and liver enzyme normalization in both dose arms.

- This positive mid-stage result adds a new potential indication to Mirum’s pipeline in a high-need liver disease, ahead of detailed data at EASL 2026 and Phase 3 readouts expected in the second half of 2026.

- Next, we’ll examine how brelovitug’s Phase 2b success in hepatitis delta could influence Mirum’s rare-disease growth narrative and risk profile.

The future of work is here. Discover the 34 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

Mirum Pharmaceuticals Investment Narrative Recap

To own Mirum, you have to believe its rare disease portfolio can translate current product revenue of US$521.3 million into durable, diversified cash flows, while R&D spending and pricing pressure remain manageable. The AZURE-1 Phase 2b success in hepatitis delta looks directionally positive, but the key near term catalyst is still late stage data from ongoing Phase 3 programs, and the central risk remains Mirum’s reliance on a concentrated orphan liver franchise.

The most relevant recent announcement is Mirum’s March 5 update that Phase 3 AZURE-1 enrollment is complete and AZURE-4 screening is finished in hepatitis delta. That milestone, now paired with positive Phase 2b data, tightens the link between near term HDV readouts and Mirum’s broader growth story, putting more weight on clinical outcomes at EASL 2026 and the second half of 2026 when pivotal data for brelovitug are expected.

Yet against this promising HDV readout, investors should be aware that Mirum’s dependence on a focused rare disease portfolio and heavy R&D spend could...

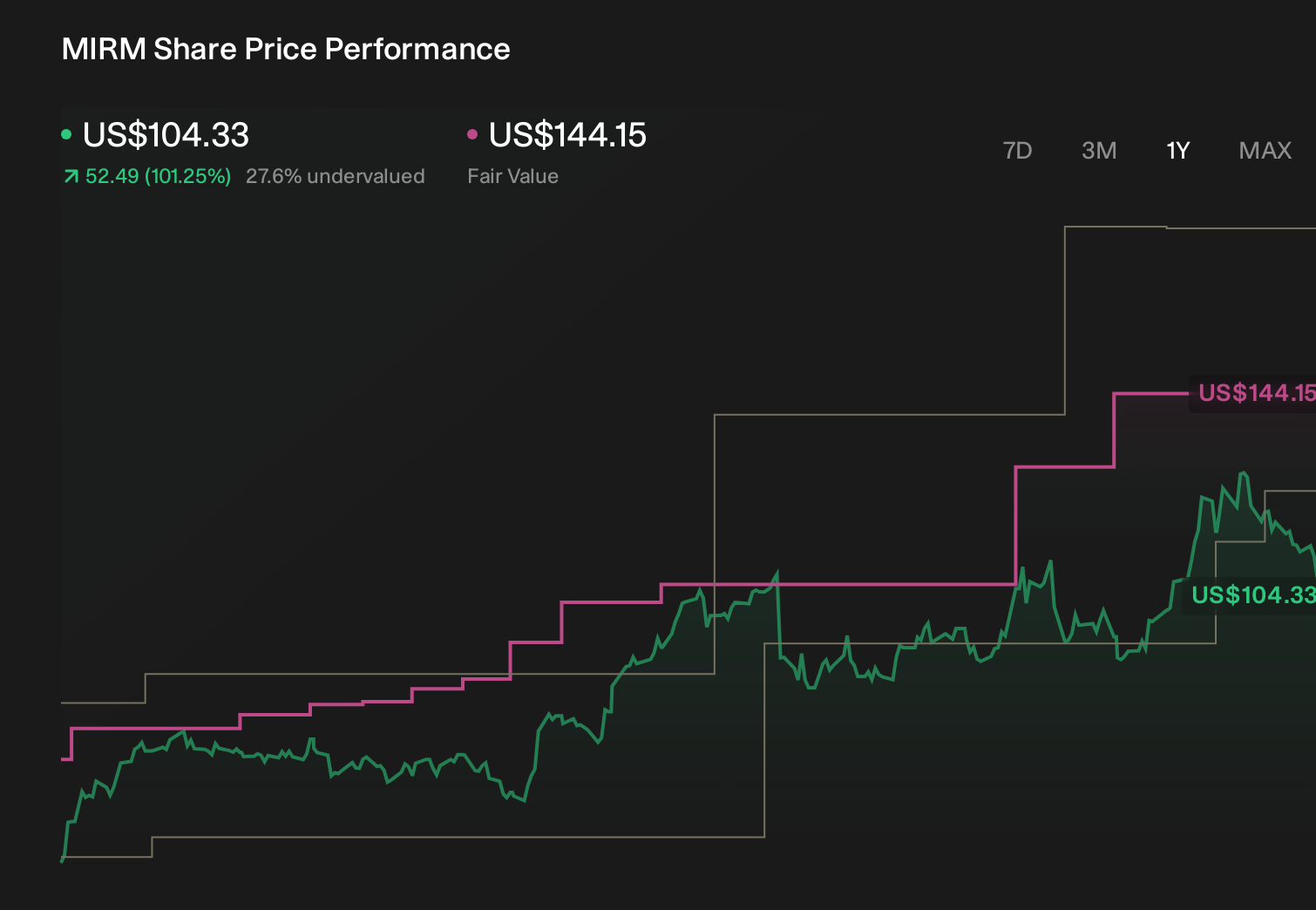

Mirum Pharmaceuticals' narrative projects $794.3 million revenue and $102.1 million earnings by 2028. This requires 22.8% yearly revenue growth and a $160.7 million earnings increase from $-58.6 million today.

Uncover how Mirum Pharmaceuticals' forecasts yield a $106.60 fair value, a 13% upside to its current price.

Exploring Other Perspectives

Some analysts were already projecting around 32 percent annual revenue growth and US$339.2 million in earnings by 2029, so brelovitug’s HDV win could either strengthen that optimistic view or highlight how much expectations may still diverge from more cautious takes on trial risk and portfolio concentration.

Explore 3 other fair value estimates on Mirum Pharmaceuticals - why the stock might be worth over 3x more than the current price!

Decide For Yourself

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your Mirum Pharmaceuticals research is our analysis highlighting 4 key rewards and 2 important warning signs that could impact your investment decision.

- Our free Mirum Pharmaceuticals research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Mirum Pharmaceuticals' overall financial health at a glance.

Looking For Alternative Opportunities?

Right now could be the best entry point. These picks are fresh from our daily scans. Don't delay:

- Find 53 companies with promising cash flow potential yet trading below their fair value.

- Invest in the nuclear renaissance through our list of 91 elite nuclear energy infrastructure plays powering the global AI revolution.

- The latest GPUs need a type of rare earth metal called Neodymium and there are only 31 companies in the world exploring or producing it. Find the list for free.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.