Will Record Q1 Profit, Dividend, and Charter Deals Reshape Frontline's (FRO) Investment Narrative?

Frontline Plc FRO | 0.00 |

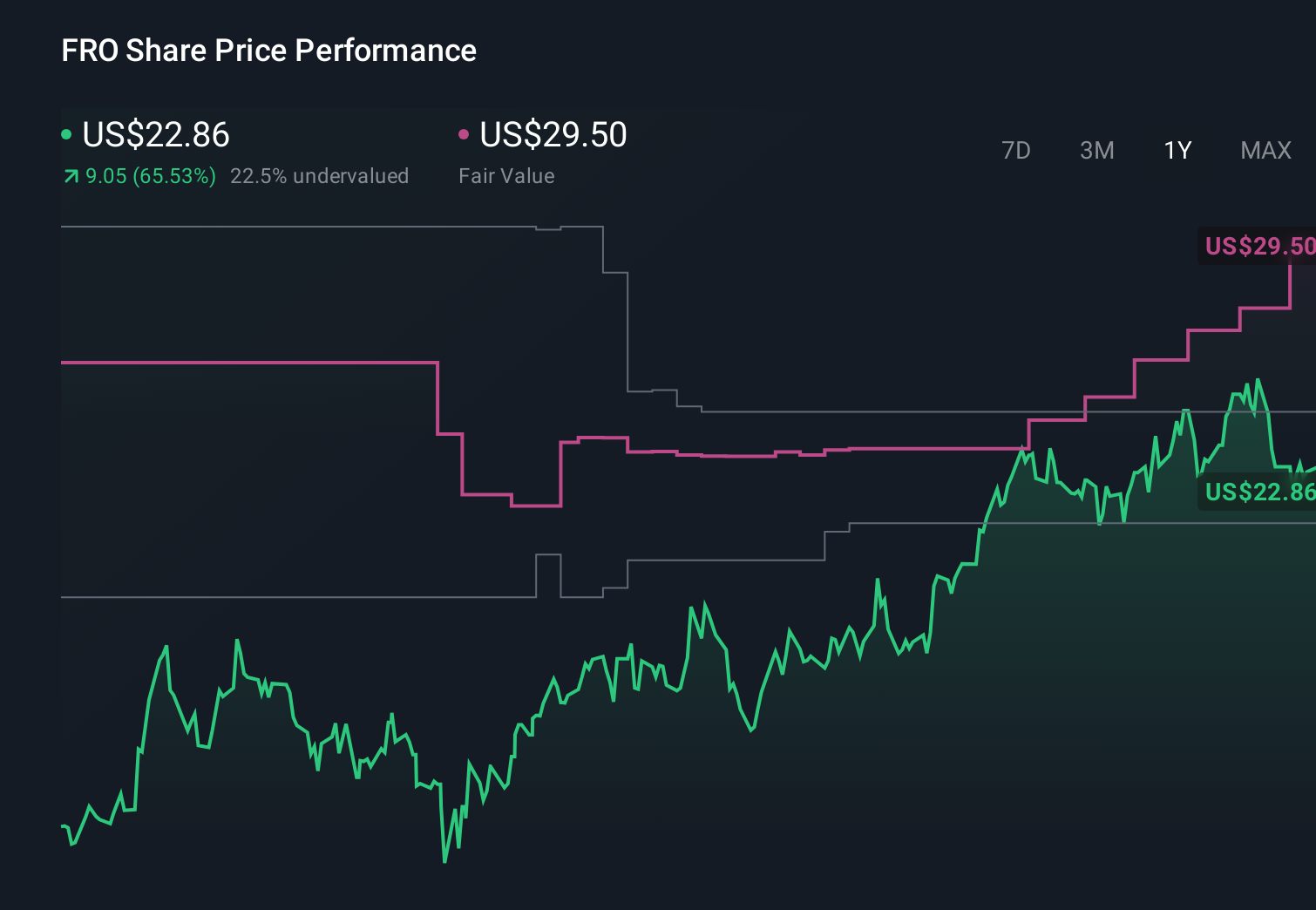

- Frontline plc has already reported first-quarter 2026 results, with sales rising to US$714.24 million and revenue to US$929.33 million, while net income increased to US$559.12 million and basic earnings per share from continuing operations reached US$2.51.

- Alongside its strongest quarterly performance since 2004, Frontline also declared a cash dividend, secured new credit facilities, realized gains from ECO VLCC sales, and locked in future income through time charter-out agreements.

- Now we’ll examine how Frontline’s record quarterly profit and dividend declaration may influence the company’s existing investment narrative.

Uncover the next big thing with 28 elite penny stocks that balance risk and reward.

Frontline Investment Narrative Recap

To own Frontline today you need to believe that its tanker fleet can keep generating attractive cash flows despite cyclical and regulatory pressures on seaborne oil trade. The first quarter 2026 record profit strengthens the short term catalyst of strong earnings translating into shareholder returns, but it does not remove the key risk that spot rate volatility and shifting energy policies could quickly reverse this profitability.

The most relevant recent development is Frontline’s Q1 2026 dividend declaration alongside its record results. This links the current earnings strength directly to cash returns, which matters if your thesis leans on income from the stock. However, the news sits against a backdrop of expected revenue declines over the next few years and dividends that are not fully covered by earnings, so how sustainable this payout path is remains an open question.

Yet beneath these record results, investors should be aware of how exposed Frontline remains to volatile tanker rates and changing oil trade patterns...

Frontline's narrative projects $1.6 billion revenue and $697.7 million earnings by 2029. This implies a 7.1% yearly revenue decline but an earnings increase of about $318.6 million from $379.1 million today.

Uncover how Frontline's forecasts yield a $41.25 fair value, a 7% upside to its current price.

Exploring Other Perspectives

Some of the lowest ranked analysts were already assuming revenue could shrink to about US$1.3 billion by 2029, so if you worry about aging fleets and trade route disruption, their more pessimistic view might feel closer to home than today’s record quarter suggests.

Explore 5 other fair value estimates on Frontline - why the stock might be worth less than half the current price!

The Verdict Is Yours

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your Frontline research is our analysis highlighting 2 key rewards and 2 important warning signs that could impact your investment decision.

- Our free Frontline research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Frontline's overall financial health at a glance.

Curious About Other Options?

Opportunities like this don't last. These are today's most promising picks. Check them out now:

- Find 53 companies with promising cash flow potential yet trading below their fair value.

- AI is about to change healthcare. These 33 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

- The future of work is here. Discover the 34 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.