Will Rising Revenue But Softer Earnings and Flat 2026 Outlook Change CubeSmart's (CUBE) Narrative?

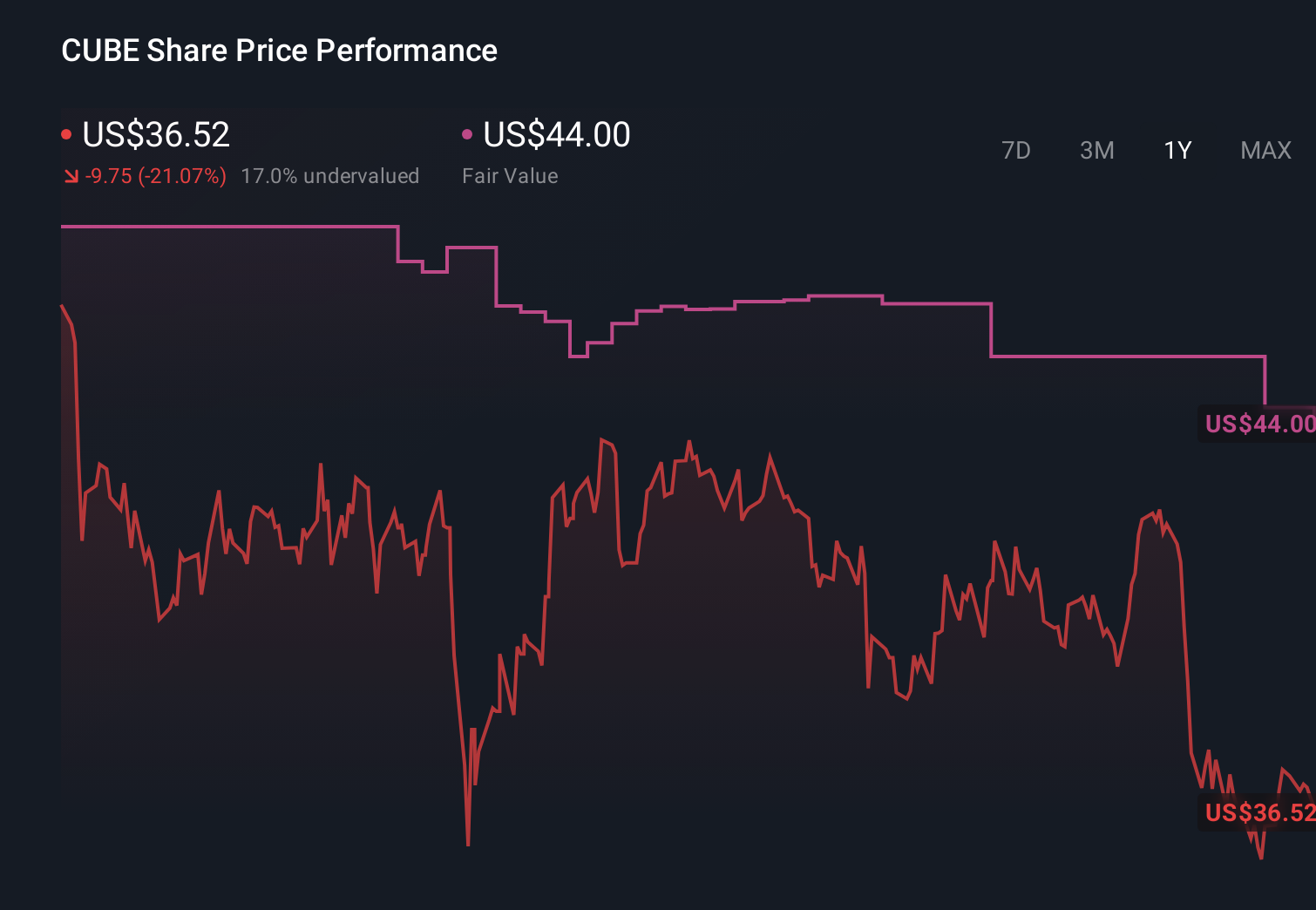

CubeSmart CUBE | 37.19 | +1.81% |

- CubeSmart recently reported fourth-quarter and full-year 2025 results showing higher revenue, as sales rose to US$240.93 million for the quarter and US$956.65 million for the year, but net income and earnings per share declined compared with 2024.

- Alongside affirming a US$0.53 quarterly dividend for April 2026, management issued 2026 guidance that points to flat to slightly negative same-store revenue and net operating income growth, highlighting a more cautious near-term outlook for the self-storage portfolio.

- We’ll now examine how this combination of rising revenue but softer earnings, plus muted 2026 same-store growth guidance, reshapes CubeSmart’s investment narrative.

Uncover the next big thing with 30 elite penny stocks that balance risk and reward.

CubeSmart Investment Narrative Recap

To own CubeSmart, you need to be comfortable with a self storage REIT that is still growing revenue while near term profitability is under pressure. The latest results, with higher top line but lower net income and muted 2026 same store guidance, reinforce that the key short term catalyst is a turn in same store revenue and NOI trends, while the biggest risk remains prolonged softness in demand and pricing. This update makes that risk feel more immediate rather than materially changing the story.

The most directly relevant announcement is management’s 2026 outlook, calling for same store revenue growth between negative 0.25% and positive 1.25%, and NOI between negative 1.75% and positive 0.25%. That guidance lines up with concerns about slower recovery in move in rates and revenue growth, and it is the lens through which I view the recent earnings miss and the affirmed US$0.53 quarterly dividend, as both cash flow resilience and operational traction matter for the next leg of the story.

Yet investors should be aware that if same store revenue stays flat for longer, it could pressure earnings and dividends...

CubeSmart's narrative projects $1.3 billion revenue and $369.9 million earnings by 2028. This requires 4.5% yearly revenue growth and a $4.9 million earnings decrease from $374.8 million today.

Uncover how CubeSmart's forecasts yield a $41.27 fair value, a 3% upside to its current price.

Exploring Other Perspectives

Four members of the Simply Wall St Community currently estimate CubeSmart’s fair value between US$40.00 and about US$58.65, highlighting a wide span of individual expectations. Set against management’s guidance for roughly flat 2026 same store revenue and NOI, these differing views remind you to compare several perspectives before deciding how resilient you think the business really is.

Explore 4 other fair value estimates on CubeSmart - why the stock might be worth as much as 46% more than the current price!

Form Your Own Verdict

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your CubeSmart research is our analysis highlighting 3 key rewards and 2 important warning signs that could impact your investment decision.

- Our free CubeSmart research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate CubeSmart's overall financial health at a glance.

No Opportunity In CubeSmart?

The market won't wait. These fast-moving stocks are hot now. Grab the list before they run:

- AI is about to change healthcare. These 29 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

- Capitalize on the AI infrastructure supercycle with our selection of the 33 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

- The latest GPUs need a type of rare earth metal called Dysprosium and there are only 31 companies in the world exploring or producing it. Find the list for free.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.