Will Strong Q1 Margins And Cash Generation Shift Brink's (BCO) Higher-Value Services Narrative?

Brink's Company BCO | 0.00 |

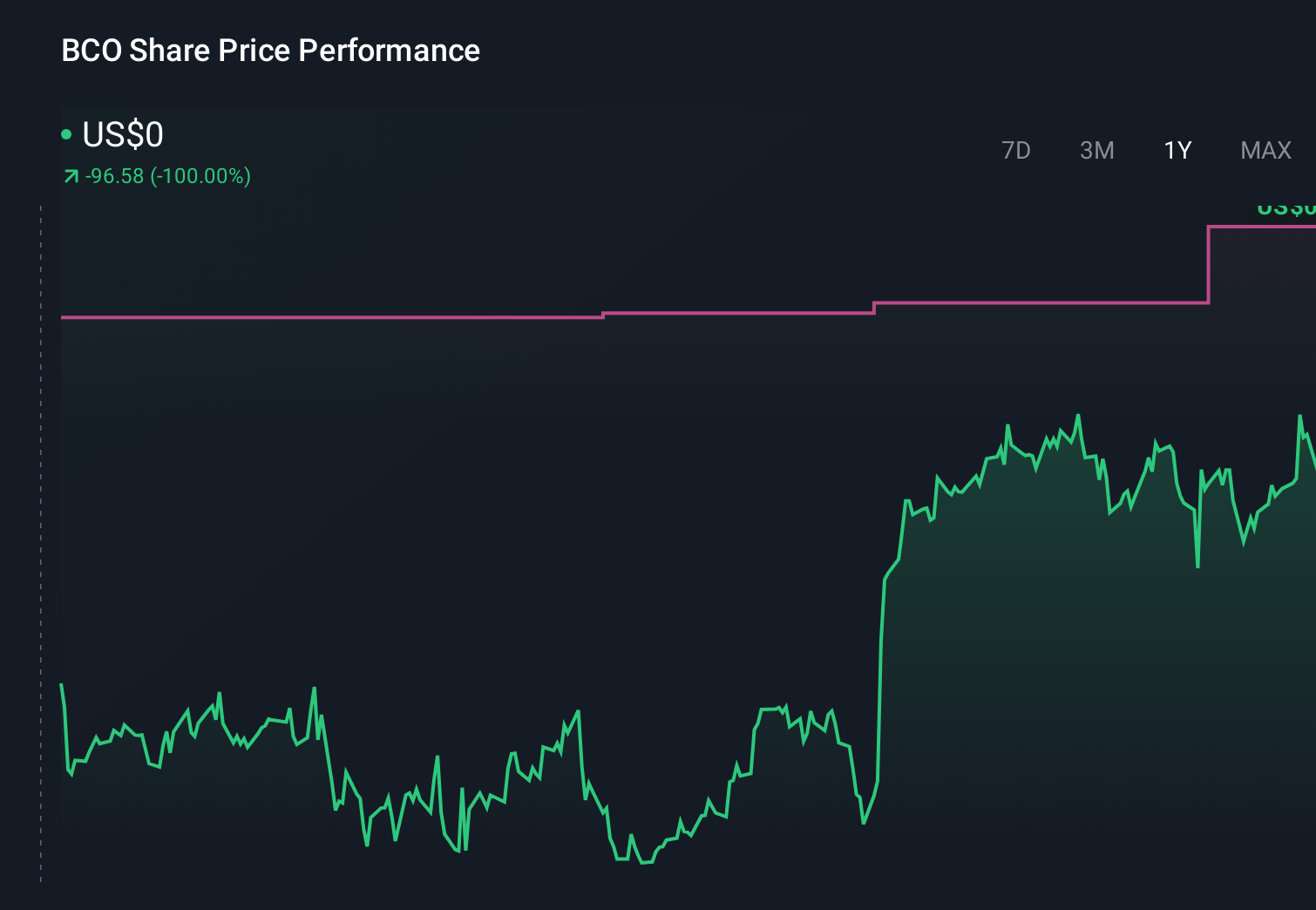

- Earlier this week, Brink's reported a strong first quarter, with double-digit revenue growth, expanding EBITDA margins, and record free cash flow driven by higher-margin AMS, DRS, and global services.

- The results were accompanied by upbeat CEO commentary and reinforced by supportive analyst views, highlighting how higher-value services are increasingly shaping Brink's business mix.

- We’ll now examine how Brink’s robust Q1 margin expansion and cash generation influence the company’s existing investment narrative and outlook.

The best AI stocks today may lie beyond giants like Nvidia and Microsoft. Find the next big opportunity with these 13 smaller AI-focused companies with strong growth potential through early-stage innovation in machine learning, automation, and data intelligence that could fund your retirement.

Brink's Investment Narrative Recap

To own Brink’s, you need to believe its shift toward higher value AMS, DRS and global services can offset structural pressure on cash usage and legacy cash handling. The strong Q1 margin expansion and record free cash flow support that thesis, but they do not materially change the near term catalyst around scaling these newer services or the key risk tied to high leverage and the cost of funding that growth.

Against this backdrop, Brink’s recent amended and restated credit agreement, which refinanced its term loans and expanded total facilities to US$3,850,000,000 for the NCR Atleos acquisition, matters for investors evaluating how growth, debt capacity and interest coverage interact with the Q1 performance.

But alongside Brink’s higher margin growth story, investors should be aware of how its elevated debt load could limit flexibility if...

Brink's narrative projects $6.3 billion revenue and $745.7 million earnings by 2029. This requires 5.4% yearly revenue growth and a $565.1 million earnings increase from $180.6 million today.

Uncover how Brink's forecasts yield a $153.00 fair value, a 46% upside to its current price.

Exploring Other Perspectives

Four Simply Wall St Community fair value views span roughly US$87 to US$356 per share, underlining how far apart individual expectations can sit. Against that spread, Brink’s reliance on AMS and DRS growth raises important questions about how different scenarios might play out for the business over time, so it is worth weighing several of these perspectives before forming a view.

Explore 4 other fair value estimates on Brink's - why the stock might be worth over 3x more than the current price!

Form Your Own Verdict

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your Brink's research is our analysis highlighting 3 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Brink's research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Brink's overall financial health at a glance.

Contemplating Other Strategies?

Early movers are already taking notice. See the stocks they're targeting before they've flown the coop:

- AI is about to change healthcare. These 34 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

- Uncover the next big thing with 25 elite penny stocks that balance risk and reward.

- Invest in the nuclear renaissance through our list of 88 elite nuclear energy infrastructure plays powering the global AI revolution.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.