Will VinFast’s Real-World EV Endurance Feats and Vietnam Deliveries Shift VinFast Auto’s (VFS) Narrative

VinFast Auto Ltd. VFS | 0.00 |

- In recent months, VinFast Auto has highlighted its EV capabilities by completing demanding endurance events in France and Germany, while also reporting nearly 100,000 domestic EV deliveries in Vietnam in the first five months of 2026.

- These endurance runs, particularly the VF 6’s 1,674 km drive in challenging heat with competitive efficiency, give investors additional real-world data points on product durability and usability beyond lab or brochure specifications.

- We’ll now examine how this proof of VF 6 and VF 8 real-world performance and growing Vietnam delivery base affects VinFast’s investment narrative.

This technology could replace computers: discover 31 stocks that are working to make quantum computing a reality.

VinFast Auto Investment Narrative Recap

To own VinFast today, you need to believe it can turn strong EV delivery growth and credible products like the VF 6 and VF 8 into a sustainable, cash generative business before its limited cash runway becomes a binding constraint. The latest European endurance runs and nearly 100,000 Vietnam deliveries in early 2026 support the product and demand story, but do little to change the near term catalyst of improving unit economics or the key risk of ongoing high cash burn and potential dilution.

The May 2026 update of 97,961 domestic EV deliveries in the first five months directly links to this news by showing that VinFast’s real world product capabilities are converting into scaled volumes in its core Vietnam market. That volume momentum is central to both the breakeven narrative and liquidity risk, because the company still needs much higher, profitable output to offset persistent losses and justify continued heavy investment in new platforms and international expansion.

Yet beneath this progress, investors should still be aware of how quickly high cash burn and limited liquidity could start to constrain...

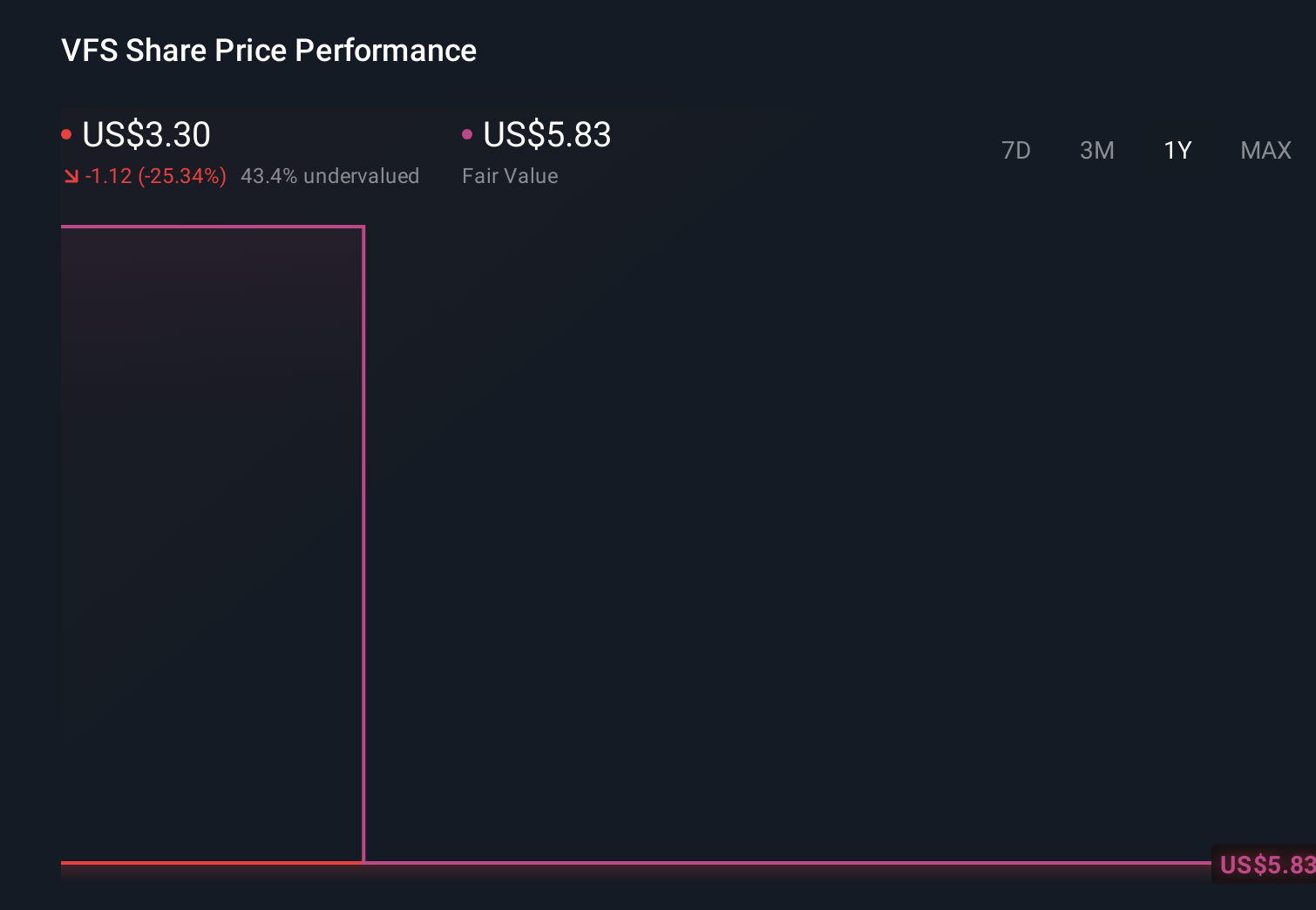

VinFast Auto’s narrative projects ₫239006.9 billion in revenue and ₫6230.1 billion in earnings by 2029. This requires 38.4% yearly revenue growth and an earnings increase of about ₫105615 billion from -₫99384.7 billion today.

Uncover how VinFast Auto's forecasts yield a $6.30 fair value, a 105% upside to its current price.

Exploring Other Perspectives

The most optimistic analysts already assumed revenue could grow about 41% a year and earnings swing by roughly ₫102,817.4 billion, which is far more bullish than the baseline view and could look either more credible or more stretched once we see how these early 2026 delivery gains and real world VF 6 and VF 8 results interact with VinFast’s heavy dependence on Vietnam as its core profit and volume engine.

Explore 5 other fair value estimates on VinFast Auto - why the stock might be worth less than half the current price!

Decide For Yourself

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your VinFast Auto research is our analysis highlighting 1 key reward and 3 important warning signs that could impact your investment decision.

- Our free VinFast Auto research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate VinFast Auto's overall financial health at a glance.

Searching For A Fresh Perspective?

Markets shift fast. These stocks won't stay hidden for long. Get the list while it matters:

- The future of work is here. Discover the 31 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

- Uncover the next big thing with 23 elite penny stocks that balance risk and reward.

- We've uncovered the 7 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.