Williams Sonoma (WSM) Could Be 10% Overvalued As New Kids Launch Tests Growth Story

Williams-Sonoma, Inc. WSM | 0.00 |

Williams-Sonoma (WSM) is back on investors’ radar after Pottery Barn Kids introduced its first collaboration with children’s clothing brand Rylee + Cru, extending the retailer’s reach across nursery, bedroom, playroom and back-to-school categories.

At a share price of $228.15, Williams-Sonoma has pulled back over the past week but still shows strong momentum, with a 30-day share price return of 12.87% and a 1-year total shareholder return of 33.67%. This performance has been supported by brand collaborations like Rylee + Cru and Hill House Home, which keep its home and kids portfolios in focus for investors.

If the Williams-Sonoma story has you thinking about what else could be setting up for long-term compounding, now is a good time to broaden your search and uncover 20 top founder-led companies

With Williams-Sonoma trading above the average analyst price target yet flagged with an intrinsic discount, investors are left with a key question: is there still a buying opportunity here, or is the market already pricing in future growth?

Most Popular Narrative: 10.2% Overvalued

Compared with the most followed fair value estimate of $207.00, Williams-Sonoma at $228.15 is priced at a premium that the narrative still seeks to explain through earnings and margin assumptions.

Continued investment and advances in AI-powered tools and digital platforms are driving higher conversion rates, improved customer experience, and measurable productivity gains, supporting both revenue growth and expanded operating leverage at the margin level. Successful focus on product innovation, exclusive partnerships, and expanding high-quality, differentiated merchandise is resonating across both core and emerging brands, enabling Williams-Sonoma to capture greater share from more affluent, urban, and younger consumers, a demographic that supports premium positioning and long-term revenue expansion.

The current fair value hinges on how far these digital gains, premium pricing power, and long run margin assumptions can stretch without relying on aggressive growth bets.

Result: Fair Value of $207.00 (OVERVALUED)

However, if tariffs climb or housing demand stays weak, Williams-Sonoma could face pressure on big-ticket sales and margins that challenges this premium narrative.

Another View: SWS DCF Points to Upside

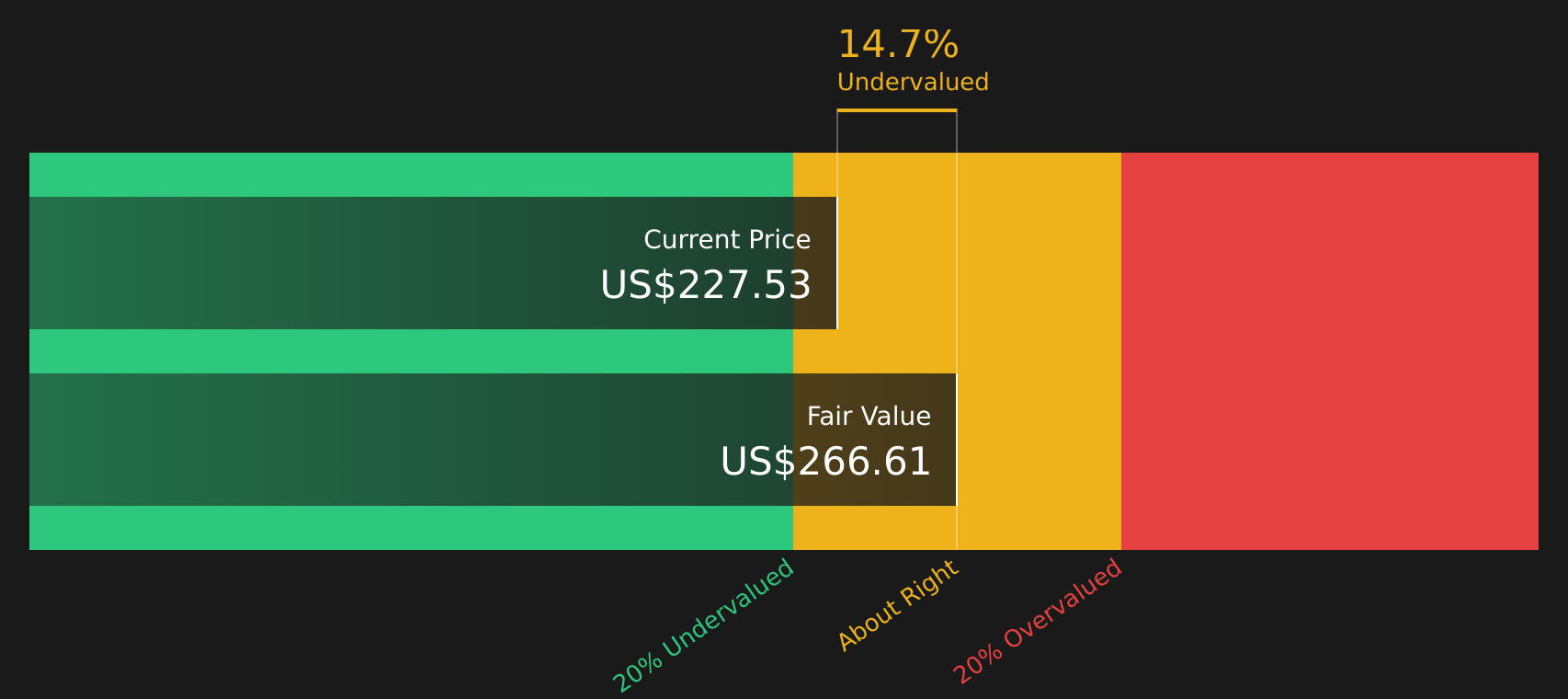

While analyst targets suggest Williams-Sonoma is about 10.2% overvalued at $228.15 versus a $207.00 fair value, the Simply Wall St DCF model tells a different story, with an estimated future cash flow value of $267.74, around 14.8% above the current price. Which set of assumptions appears more reasonable?

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Williams-Sonoma for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 41 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

If the mix of optimism and caution around Williams-Sonoma still feels finely balanced, now is the moment to dig into the numbers yourself and stress test the assumptions that matter most to you, starting with the company’s 2 key rewards

Looking for more investment ideas beyond Williams-Sonoma?

If Williams-Sonoma has sharpened your focus on quality, do not stop here. Your next strong holding might come from a fresh corner of the market uncovered today.

- Target reliable cash flow potential by checking companies built to return income year after year through 8 dividend fortresses.

- Hunt for opportunities where quality and price still line up by scanning 41 high quality undervalued stocks before other investors catch on.

- Spot resilient companies that may hold up when conditions get tougher by reviewing 73 resilient stocks with low risk scores now, not after the next bout of volatility.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.