Williams Sonoma (WSM) Stock Valuation After Sector Rally And Mixed Fair Value Signals

Williams-Sonoma, Inc. WSM | 0.00 |

Williams-Sonoma (WSM) has been back on traders’ screens after a sector wide rally lifted specialty retail stocks, with buying interest supported by its e-commerce footprint and modestly positive earnings estimate revisions.

The stock’s recent jump fits into a broader upswing, with a 24.72% 1 month share price return and 21.53% 3 month share price return. Meanwhile, the 1 year total shareholder return of 43.36% and very large 3 year total shareholder return point to momentum that has been building over time rather than fading.

If this kind of momentum in specialty retail has your attention, it could be a good time to broaden your search and check out the 20 top founder-led companies

With Williams-Sonoma trading at US$218.74, sitting above a consensus analyst price target of US$207.06 yet implying around a 14% discount to one intrinsic value estimate, you have to ask: is there still a buying opportunity here, or is the market already pricing in future growth?

Most Popular Narrative: 5.7% Overvalued

Williams-Sonoma’s most followed narrative pegs fair value at $207, slightly below the last close at $218.74, which sets up a clear valuation tension for investors to unpack.

Continued investment and advances in AI-powered tools and digital platforms are driving higher conversion rates, improved customer experience, and measurable productivity gains, supporting both revenue growth and expanded operating leverage at the margin level.

Curious what kind of revenue profile, margin shape, and future earnings multiple are needed to justify that fair value gap? The full narrative spells out a detailed path that blends modest growth, stable profitability, and a premium earnings ratio into one coherent valuation story.

Result: Fair Value of $207 (OVERVALUED)

However, the narrative can still be knocked off course if tariff costs rise faster than expected or if prolonged housing market weakness keeps pressure on big ticket spending.

Wall Street's queuing for one rocket. While SpaceX counts down to its IPO, other companies tied to the new space race are already in orbit. → 20 Compelling Space Companies watchlist · Global Space Race Investing Ideas screener · Scan the sector by valuation on Rocket Lab's valuation page.

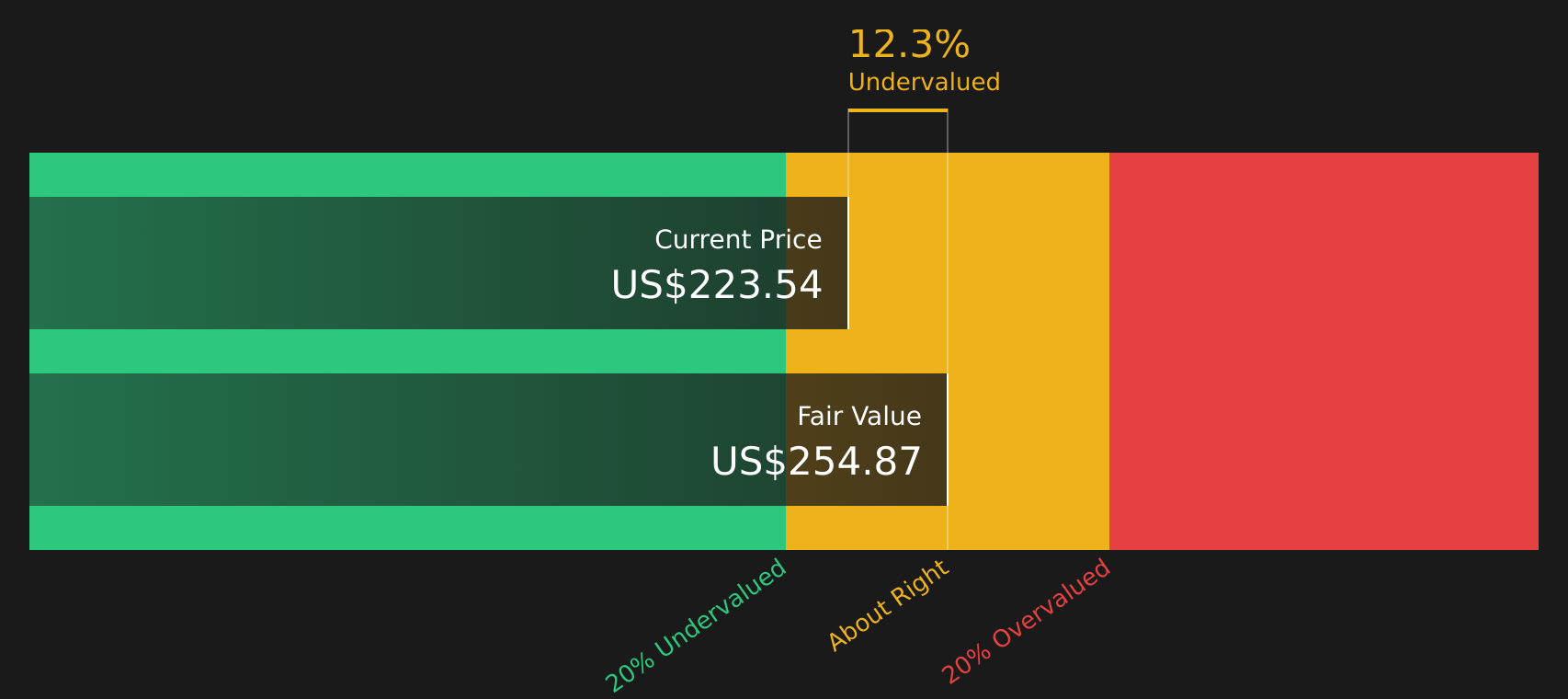

Another View: Cash Flows Tell a Different Story

While the consensus narrative suggests Williams-Sonoma is 5.7% overvalued at a fair value of $207, the SWS DCF model points the other way and indicates the stock is trading about 14.2% below an estimated future cash flow value of $254.89. When multiples suggest the shares are expensive but cash flows indicate they are inexpensive, which signal do you lean on?

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Williams-Sonoma for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 46 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

If these mixed signals have you torn between caution and curiosity, move quickly to test the assumptions, pressure check the numbers, and weigh the 2 key rewards.

Looking for more investment ideas?

Do not stop at a single stock when there are tools built to help you spot opportunities fast, use the screener to see what else fits your criteria.

- Target resilient balance sheets and steady fundamentals by scanning the solid balance sheet and fundamentals stocks screener (47 results) before capital moves elsewhere.

- Hunt for quality at a discount and let the 46 high quality undervalued stocks surface companies that might deserve a closer look.

- Spot potential future standouts early by checking the screener containing 20 high quality undiscovered gems and see which stocks are quietly building solid profiles.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.