Wynn Resorts (WYNN) Joins Russell Growth Indexes On A Fair Value Debate

Wynn Resorts, Limited WYNN | 0.00 |

Wynn Resorts (WYNN) has just been added to several Russell growth benchmarks, including the Russell 1000 Growth and Russell Midcap Growth. This move can influence how index funds and benchmarked investors treat the stock.

Despite being added to several Russell growth indices, Wynn Resorts’ recent momentum has been weak, with the share price down 9.8% over the past month and year to date. The 1 year total shareholder return has also declined 7.3%, pointing to fading enthusiasm even after index inclusion.

If this index move has you thinking about other opportunities in the market, it could be a useful moment to scan for 20 top founder-led companies

So with Wynn Resorts stock down so far this year, but now sitting in multiple Russell growth indices, is the recent weakness setting up a mispriced opportunity, or is the market already factoring in the company’s future growth?

Most Popular Narrative: 29.3% Undervalued

Against Wynn Resorts' last close of $96.11, the most widely followed narrative pegs fair value at $135.89, framing the recent share price weakness in a very different light.

The imminent launch of Wynn Al Marjan Island, with first-mover advantage and limited near-term competition in a potentially multi-billion-dollar new market, is a major forward catalyst that is currently underappreciated by investors and could drive a meaningful step-change in both consolidated revenue and EBITDAR.

Curious what sits behind that optimism on Wynn Resorts? The narrative leans on measured revenue growth, fatter margins, and a future earnings multiple that assumes investors keep paying up for this cash flow story. The exact mix of those ingredients is where the valuation gets interesting.

Result: Fair Value of $135.89 (UNDERVALUED)

However, Wynn Resorts still faces significant pressures, including heavy exposure to Macau and sizeable capital spending that could strain cash flow if project returns disappoint.

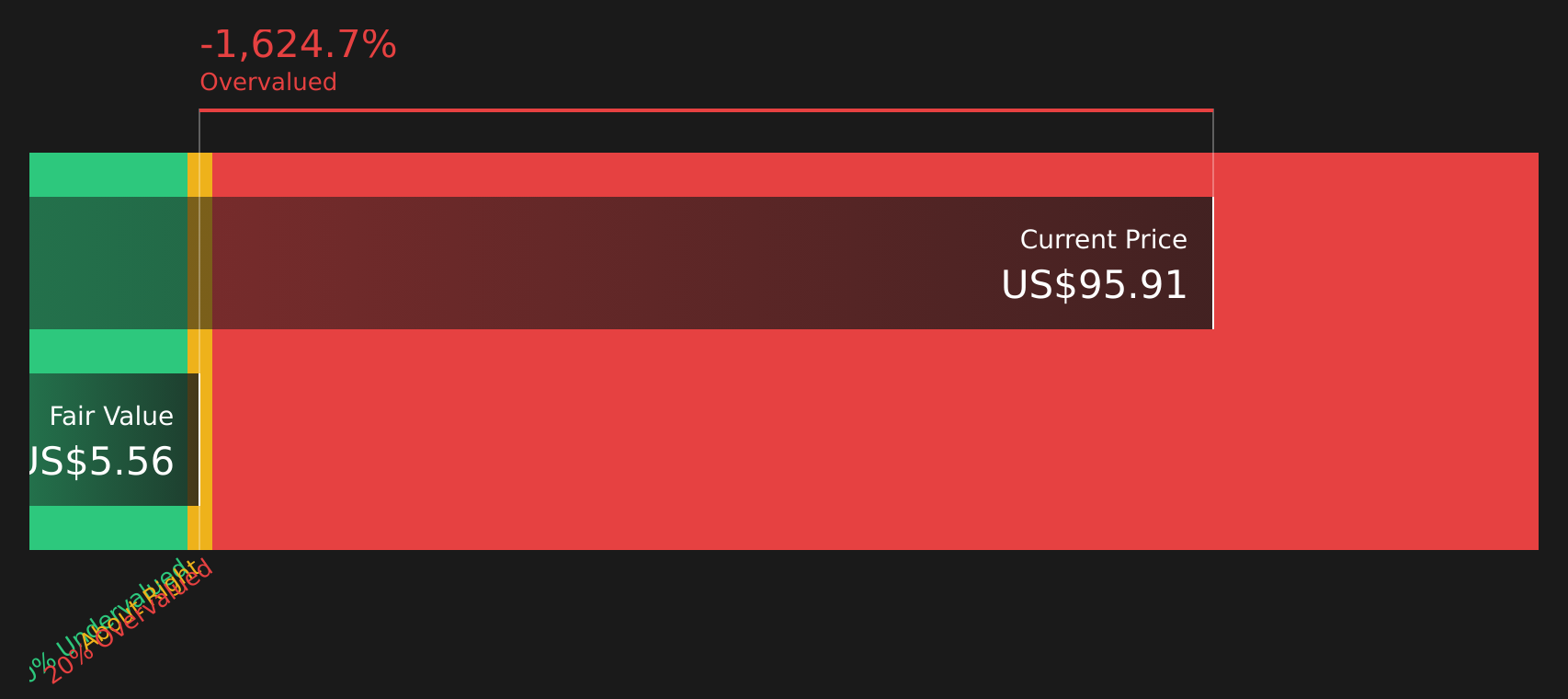

Another View: Wynn Resorts Through A Cash Flow Lens

While the popular narrative around Wynn Resorts leans on earnings and price targets, the SWS DCF model points in the opposite direction. In that framework, the stock at $96.11 sits well above an estimated future cash flow value of $5.49, flagging it as materially overvalued rather than undervalued. For investors, the question is which story feels more realistic: the earnings path or the cash flow profile?

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Wynn Resorts for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 41 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

With sentiment on Wynn Resorts clearly split between opportunity and concern, this is a moment to look at the data yourself and move quickly. To weigh both sides of the story in one place, take a closer look at the 2 key rewards and 2 important warning signs

Looking for more investment ideas beyond Wynn Resorts?

If Wynn Resorts has you thinking harder about where you put your money next, do not sit on the sidelines while other opportunities move ahead.

- Target resilient income by scanning companies that look like potential long term payers with the 8 dividend fortresses.

- Hunt for quality at a discount by checking stocks that combine earnings strength with attractive pricing through the 41 high quality undervalued stocks.

- Prioritise capital preservation by focusing on companies that show stronger balance sheets and fundamentals using the solid balance sheet and fundamentals stocks screener (47 results).

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.