Yum! Brands (YUM) Buyback Puts Fair Value Back In Focus

Yum! Brands, Inc. YUM | 0.00 |

Yum! Brands (YUM) has authorized a new share repurchase program of up to US$4.0b, running through June 30, 2028. This decision is prompting investors to reassess what this capital allocation choice could mean for the stock.

Yum! Brands has seen positive share price momentum recently, with a 7 day share price return of 4.98% and a 30 day share price return of 6.96%. The 1 year total shareholder return of 8.84% and 5 year total shareholder return of 48.60% point to steadier longer term compounding, suggesting the new US$4.0b buyback arrives as sentiment is building rather than fading.

If this buyback has you thinking about where else capital could work hard, it may be a good time to widen your search and check out 20 top founder-led companies

With Yum! Brands trading at US$158.24 and an intrinsic value estimate that sits about 6% higher, while also standing at roughly a 10% discount to analyst price targets, you have to ask: is there still an opportunity here, or is the market already pricing in future growth?

Most Popular Narrative: 8.9% Undervalued

Compared with Yum! Brands' last close at $158.24, the most followed narrative pegs fair value closer to $173.71, anchoring the new buyback in a richer valuation story.

The asset-light, heavily franchised operating model minimizes capital intensity and allows for recurring, predictable cash flows while enabling rapid global expansion, with improved franchisee economics via proprietary tech (Byte) further supporting long-term operating profit and EPS growth.

Curious what backs that higher fair value for Yum! Brands? The narrative leans on compounding revenue, firmer margins, and a richer future earnings multiple. The exact mix of those inputs matters.

Result: Fair Value of $173.71 (UNDERVALUED)

However, Yum! Brands still faces pressure if digital investments do not deliver the expected efficiencies, or if softer demand in weaker KFC and Pizza Hut markets persists.

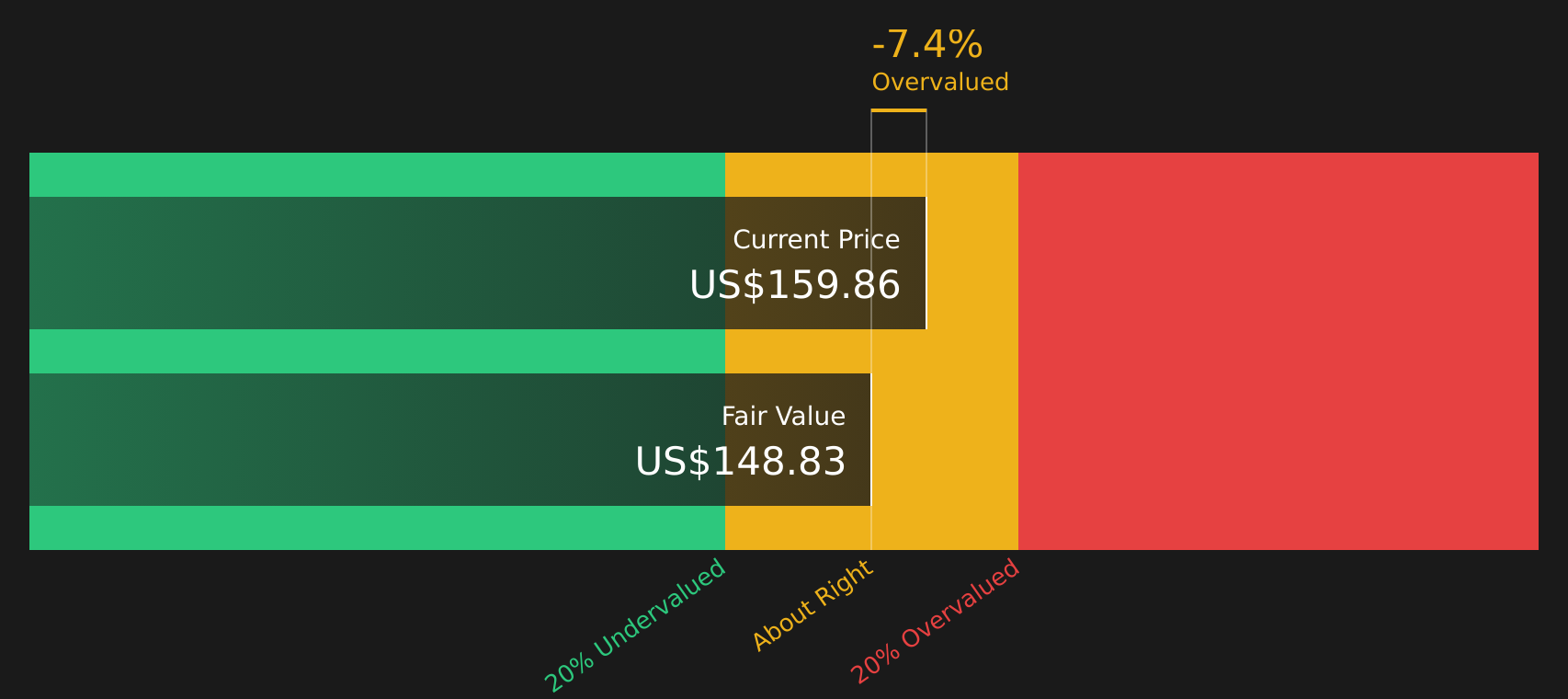

Another View: Yum! Brands Through a Cash Flow Lens

The fair value narrative around Yum! Brands leans on earnings and price targets, but the SWS DCF model tells a different story. On that cash flow based view, the stock at $158.24 sits above an estimated value of $148.92, pointing to an overvalued result rather than an 8.9% discount. Which lens do you trust more when real cash is on the line?

For a closer look at how this cash flow view is built and what would need to change for the gap to close, Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Yum! Brands for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 42 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

With Yum! Brands presenting both appealing upside signals and clear risk flags, it makes sense to move quickly, review the underlying data, and decide where you stand based on 2 key rewards and 3 important warning signs

Looking for more investment ideas beyond Yum! Brands?

If Yum! Brands has sharpened your focus on where capital can work harder, do not stop here. Use the Simply Wall St screener to uncover what you might be missing.

- Spot potential value opportunities early by reviewing 42 high quality undervalued stocks before other investors catch on.

- Strengthen your portfolio's foundations by scanning the solid balance sheet and fundamentals stocks screener (48 results) for companies with sturdier financial footing.

- Hunt for tomorrow's standouts by combing through the screener containing 19 high quality undiscovered gems while they are still off most investors' radars.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.