ZTO Express Stock Leads 3 Value Picks For Higher Rate Uncertainty

Compania de Minas Buenaventura SAA Sponsored ADR BVN | 0.00 |

With central banks focused on inflation control and signalling possible rate hikes, value stocks with solid balance sheets and consistent dividends can look relatively interesting for investors who want income and are wary of paying high multiples. This article looks at three stocks from a Value Stocks screener that appear closely tied to the current monetary policy backdrop, where higher borrowing costs and ongoing geopolitical and supply chain pressures are shaping expectations. Each stock has its own mix of valuation, financial strength, and dividend profile. The following sections unpack how these features might help or hurt in the months ahead.

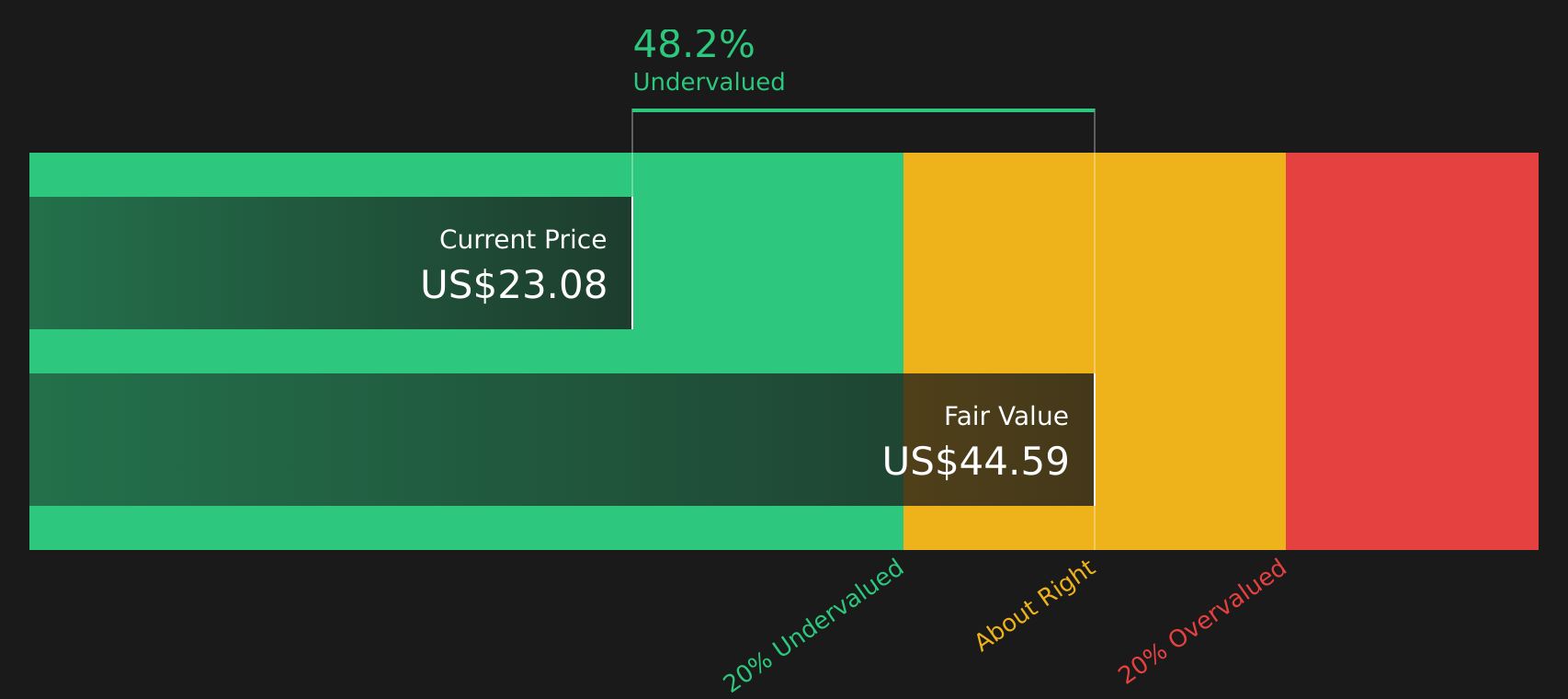

ZTO Express (Cayman) (ZTO)

Overview: ZTO Express (Cayman) is a major Chinese logistics company that focuses on parcel delivery, providing express shipping, less than truckload freight, warehousing, and freight forwarding services across the People’s Republic of China.

Operations: ZTO generates its CN¥51.5b in revenue primarily from trucking based transportation services within the People’s Republic of China.

Market Cap: US$17.4b

Investors watching interest rate moves may find ZTO Express (Cayman) interesting because it combines a large scale domestic logistics network with value style traits such as a single country focus, a P/E below many peers, and analyst expectations for steady earnings growth in a sector viewed as essential to China’s e commerce activity. Central bank tightening and higher borrowing costs can put pressure on weaker competitors. At the same time, ZTO is investing heavily in automation and AI to reduce unit costs and support margins, even as parcel growth slows and competition and regulation remain real risks. The tension between its cost efficiency, pricing power signals from management, and those competitive pressures is where the real story starts to get interesting.

ZTO Express (Cayman) looks like a cost efficiency story that could be masking a deeper valuation angle, and the DCF valuation analysis for ZTO Express (Cayman) may show whether that low P/E reflects opportunity or a hidden pressure point investors are missing.

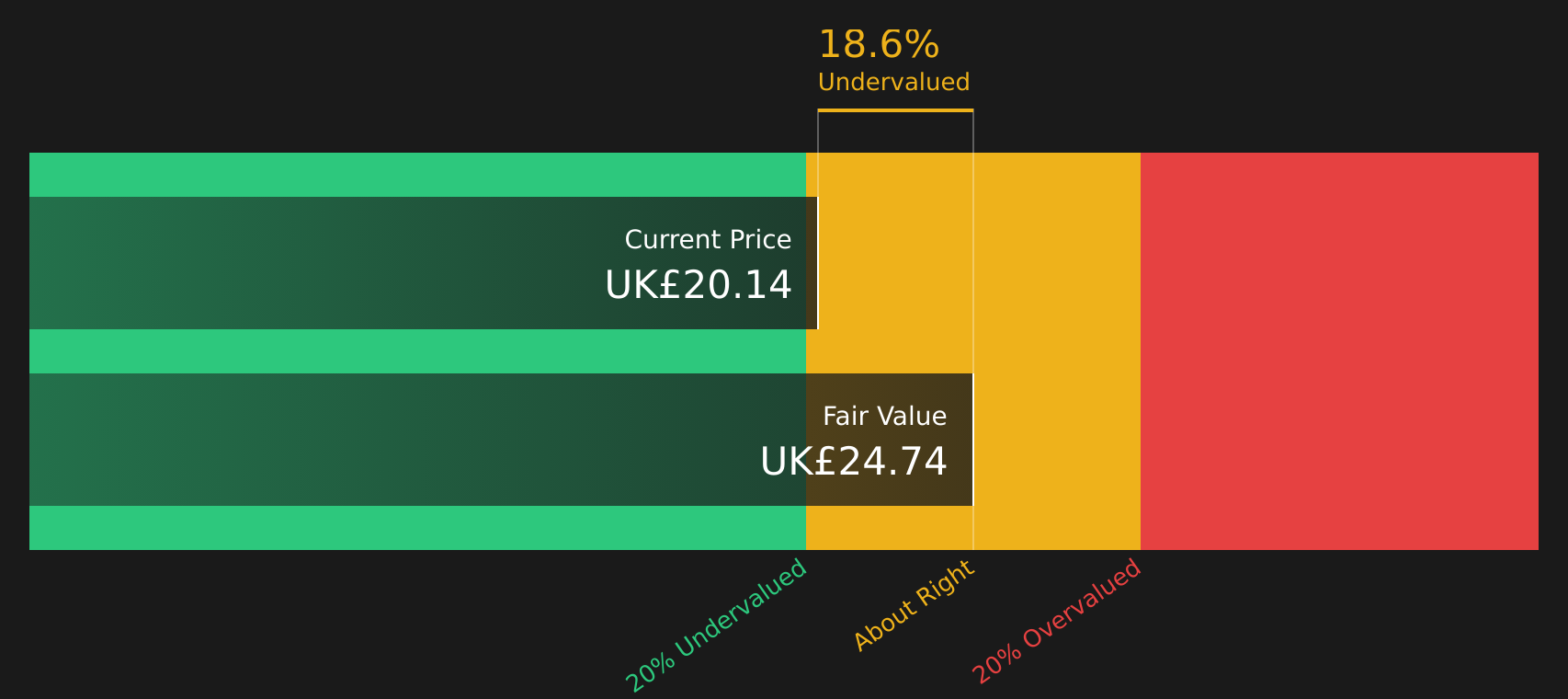

Johnson Matthey (LSE:JMAT)

Overview: Johnson Matthey is a long-established UK chemicals and materials company that focuses on clean air catalysts for combustion engines, platinum group metal refining and recycling, and hydrogen technologies for fuel cells and electrolysers across major global markets.

Operations: Johnson Matthey generates most of its £12.6b in revenue from PGM Services at £10.3b and Clean Air at £3.8b, with Hydrogen Technologies contributing £80m and a large internal eliminations line of £1.6b.

Market Cap: £3.2b

Investors looking at Johnson Matthey in a period of tighter monetary policy may be drawn to its mix of established cash generative businesses and exposure to cleaner technologies, while also recognising some clear execution questions. The stock screens as a value candidate, trading below some estimates of fair value and offering a 4% dividend yield. However, the company reported a loss of £96m on £12.6b of revenue and carries a high debt load, with the dividend not well covered by current earnings. Management is pushing a transformation focused on cost savings, higher margin PGM processing and closer links between Clean Air and Hydrogen Technologies, and is signalling confidence by holding the dividend steady. This sits alongside forecasts for sharp revenue declines and the need to turn losses around in a tougher, higher rate world where funding is more expensive and missteps are punished quickly.

Johnson Matthey looks like a stalled transformation story masking something more interesting, where a 4% yield, heavy PGM exposure and hydrogen ambitions intersect. The analysis report for Johnson Matthey hints at how that mix could reshape the risk reward profile.

Compañía de Minas BuenaventuraA (BVN)

Overview: Compañía de Minas BuenaventuraA is a Peru based precious and base metals group that explores, builds, and operates gold, silver, copper, zinc, lead, and antimony mines, while also running smelting, power generation, and related industrial activities.

Operations: Buenaventura’s revenue is anchored in mining operations at Uchucchacua (US$830.9m), Colquijirca (US$594.4m), Orcopampa (US$260.9m), and equity interests in Cerro Verde (US$5.7b) and Coimolache (US$310.2m), alongside smaller industrial and energy activities.

Market Cap: US$7.4b

Compañía de Minas BuenaventuraA is drawing attention because it mixes sizeable producing assets, exposure to copper and precious metals, and a value style profile in a world where central banks are tightening and investors are rethinking inflation hedges. Recent quarters show high profit margins and strong earnings quality, backed by tangible mines and power assets rather than hopes and concepts. Projects like Yumpag and San Gabriel point to potential future production shifts. At the same time, investors need to weigh higher costs, financing demands for new projects, and sensitivity to metal prices and inflation on equipment and labor. How those moving parts fit with its current valuation and analyst expectations is where the opportunity, and the real debate, starts.

Compañía de Minas BuenaventuraA looks like an earnings quality and asset depth story that many investors may be underestimating. Use the full narrative for Compañía de Minas BuenaventuraA to see how those mines, margins and future projects really fit together before one key twist changes the picture.

The three stocks covered here are just a starting point. The full Value Stocks screener surfaced 7 more companies with equally compelling income and valuation stories that you have not seen yet, all packed into the Value Stocks screener. Use Simply Wall St to identify and analyze the exact catalysts, balance sheet traits, and dividend narratives that matter most so you can focus on the value ideas that best match your conviction level.

Take Control of Your Investment Journey

If Johnson Matthey or any of these companies sound like a great opportunity, register for FREE with Simply Wall St and add your companies to a Watchlist to monitor the share price against the fair value the ideal entry point. Once you've made your move, manage your holdings with our Portfolio Command Center that filters out the noise to deliver only the most critical, actionable updates. Throughout your journey, our Community allows you to filter the best ideas from thousands of investor perspectives. By uncovering hidden catalysts and risks early, you'll accelerate your decision-making and stay one step ahead of the market.

Seeking Alternatives Before Everyone Else?

Fresh stock ideas can move from quiet to crowded quickly, with breakouts flying once momentum is caught and prices dropping back when the story goes stale, so consider acting while conditions still suit your approach.

- Spot under-the-radar potential in resilient companies by scanning a curated 75 resilient stocks with low risk scores while the crowd is still focused on headline volatility.

- Explore the next wave of digital infrastructure demand by screening a hand picked mix of 52 AI infrastructure stocks before valuations reprice and the early window closes.

- Target real asset backing in metal producers by reviewing a tightly filtered group of 33 elite gold producer stocks while these ideas remain under the radar for now.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.