Zurn Elkay Water Solutions (ZWS) Margin Improvement Reinforces Bullish Narratives Despite Rich P E

Zurn Elkay Water Solutions Corporation ZWS | 47.39 47.39 | -3.97% 0.00% Pre |

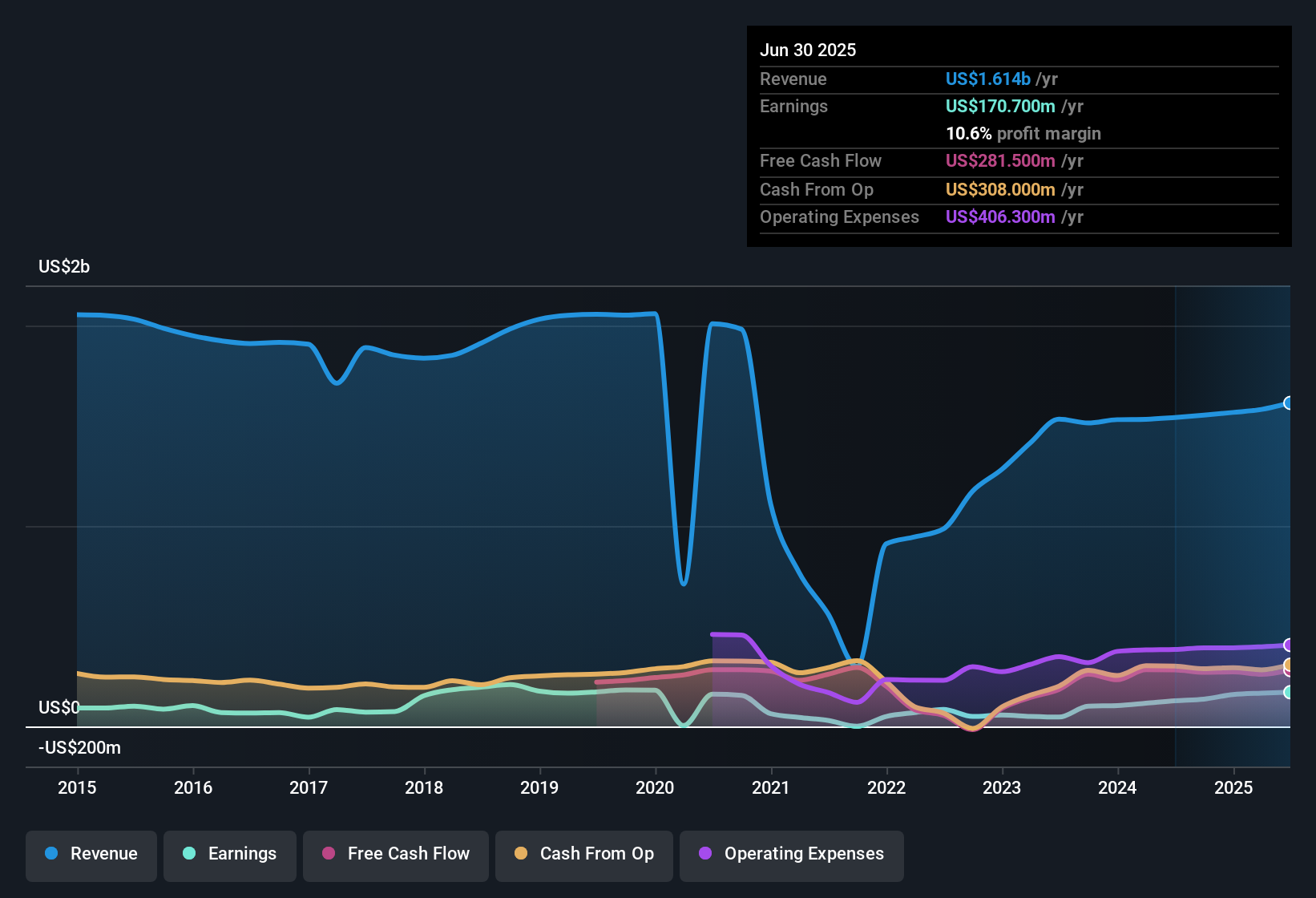

Zurn Elkay Water Solutions (ZWS) has wrapped up FY 2025 with fourth quarter revenue of US$407.2 million and basic EPS of US$0.25, while trailing twelve month revenue sits at US$1.70 billion with EPS of US$1.14. This gives investors a clear read on both the latest quarter and the full year run rate. The company has seen quarterly revenue move from US$370.7 million and EPS of US$0.21 in Q4 2024 to a range between US$388.8 million and US$455.4 million and EPS between US$0.24 and US$0.35 through 2025. This sets the backdrop for a year where higher earnings growth forecasts and an 11.3% trailing net margin put profitability in sharp focus.

See our full analysis for Zurn Elkay Water Solutions.With the headline numbers on the table, the next step is to see how this earnings profile lines up with the widely followed narratives around Zurn Elkay Water Solutions, and where the latest margin performance supports or challenges those views.

11.3% net margin puts profitability in focus

- On a trailing twelve month basis, Zurn Elkay earned US$192.4 million of net income on US$1.70b of revenue, which works out to an 11.3% net margin compared with 10.1% a year earlier.

- A more bullish view here is backed by trailing EPS of US$1.14 and that 11.3% margin, alongside a 21.1% earnings increase over the last year. At the same time, earnings growth forecasts of about 12.9% a year are lower than the 34.6% five year pace, which may lead optimistic investors to focus more on the current margin level than on repeating past growth rates.

Earnings growing faster than revenue

- Forecasts in the data show earnings expected to grow about 12.9% per year while revenue is expected to grow about 5.2% per year. Over the last year, earnings rose 21.1% against a smaller move in trailing revenue from US$1.57b to US$1.70b.

- Supporters of a bullish angle often like this kind of gap between revenue and earnings growth, because

- the trailing net income increase from US$158.9 million to US$192.4 million on a smaller change in revenue suggests more profit per dollar of sales in the period, and

- the 34.6% five year annualized earnings growth sits well above both the latest 21.1% yearly gain and the 12.9% forecast, which can make the current earnings profile look more conservative than the longer term track record.

Premium P/E and DCF gap to US$47.93

- Zurn Elkay trades on a trailing P/E of 44.4x, above the US Building industry average of 22.7x but below a peer average of 59.1x. The supplied DCF fair value of US$47.93 sits below the current share price of US$51.11.

- For a more cautious or bearish angle, critics point out that

- paying 44.4x trailing earnings already embeds strong expectations on top of the recent 21.1% earnings growth, and

- the gap between the US$51.11 share price and the US$47.93 DCF fair value in the data gives a concrete figure skeptics can reference when they argue that valuation is running ahead of those 5.2% revenue and 12.9% earnings growth forecasts.

Next Steps

Don't just look at this quarter; the real story is in the long-term trend. We've done an in-depth analysis on Zurn Elkay Water Solutions's growth and its valuation to see if today's price is a bargain. Add the company to your watchlist or portfolio now so you don't miss the next big move.

See What Else Is Out There

With a trailing P/E of 44.4x above the industry average and a DCF fair value of US$47.93 below the US$51.11 share price, valuation looks demanding.

If that rich pricing makes you cautious, it is a good time to run your eye over 54 high quality undervalued stocks that could offer more modest valuations and a wider margin of safety.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.