Zymeworks (ZYME) Stock Could Be 42.3% Undervalued After Cryo EM Breakthrough

Zymeworks Inc. ZYME | 0.00 |

Why Zymeworks’ Cryo‑EM Breakthrough Matters for the Stock

Zymeworks (ZYME) just reported a collaboration with Gandeeva Therapeutics that used high resolution cryo electron microscopy to map a small antigen bound to a Zymeworks antibody, sharpening insight into antibody epitope binding.

For you as a shareholder or potential investor, the key point is that this work goes beyond a headline partnership announcement and delivers specific structural data, including a 2.6 Å view of nine amino acids that form the antibody binding epitope. That level of detail can influence how efficiently Zymeworks prioritizes antibody candidates and refines biologics in its pipeline.

The cryo EM progress and recent ZW191 data arrive after a mixed stretch for Zymeworks’ share price, which is down 13.07% year to date but sits on a very strong 1 year total shareholder return of 85.42% and a 3 year total shareholder return of 185.33%. This suggests past momentum has been strong even as shorter term share price returns have cooled.

If Zymeworks’ antibody and ADC work has your attention, it could be a good moment to see what else is emerging in healthcare AI by scanning 40 healthcare AI stocks

With Zymeworks trading at $23.14 and sitting at a large discount to a $39.23 analyst price target, the key question is simple: are you looking at an overlooked entry point or a stock already pricing in future growth?

Most Popular Narrative: 42.3% Undervalued

The most followed narrative on Zymeworks compares a fair value of $40.08 to the last close at $23.14, framing the stock as materially discounted based on long term cash flow assumptions.

The analysts have a consensus price target of $40.08 for Zymeworks based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $58.0, and the most bearish reporting a price target of just $31.0.

Want to see why this narrative points to such a large gap between price and fair value? The core story links rapid revenue expansion, margin reset and a future earnings multiple that is rarely seen in early stage biotechs. Curious which assumptions have the biggest impact on that valuation path and how sensitive the outcome is to them? The full narrative lays out those numbers step by step.

Result: Fair Value of $40.08 (UNDERVALUED)

However, Zymeworks’ story still hinges on partner execution around milestones and royalties, as well as on early stage assets clearing clinical and regulatory hurdles without major setbacks.

Another View on Zymeworks’ Valuation

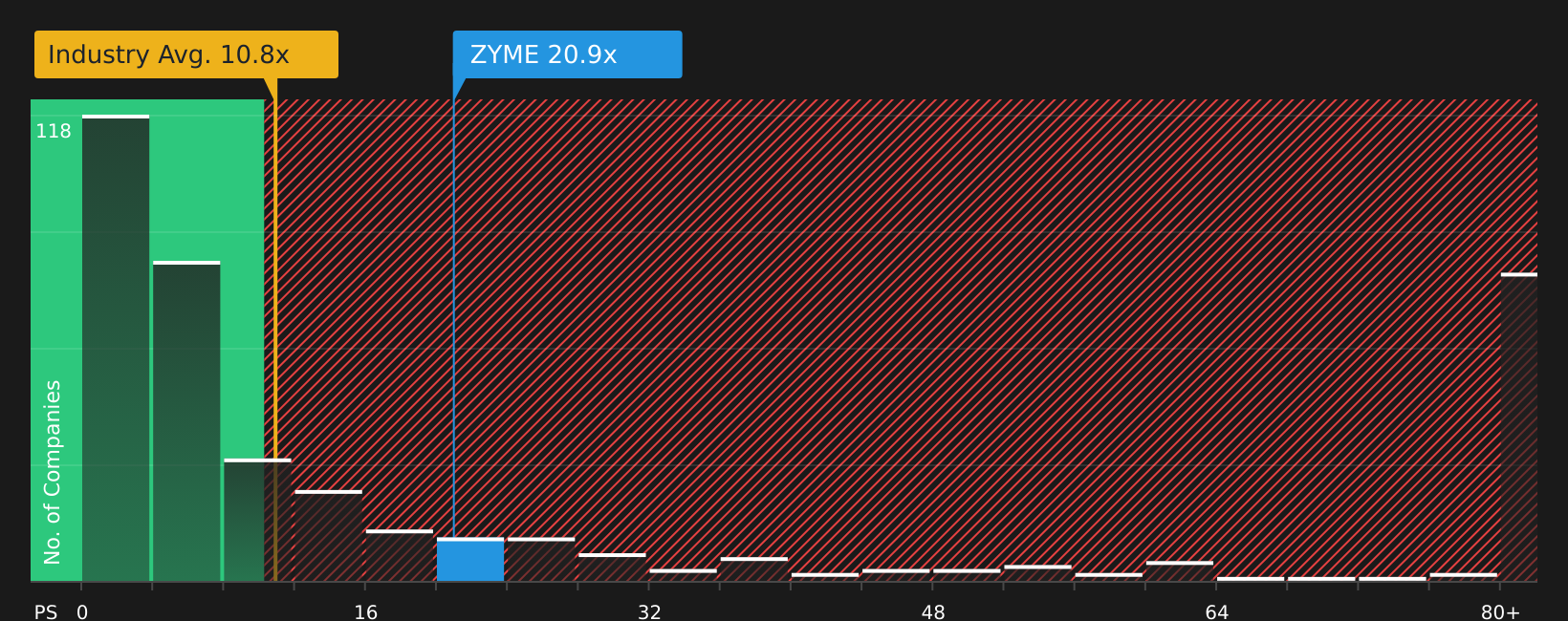

The first narrative leans heavily on analyst targets and long term earnings assumptions to argue Zymeworks is undervalued. Yet its current P/S of 20.8x is almost double the US Biotechs industry average of 10.8x and far above a fair ratio of 0.9x, which points to meaningful valuation risk if sentiment cools.

For a closer look at what this gap could mean for you as an investor, and how the numbers stack up in context, See what the numbers say about this price — find out in our valuation breakdown.

Next Steps

If the mix of optimism and caution around Zymeworks has you thinking, take a moment to review the data yourself and move quickly to refine your stance as you weigh the company’s 3 key rewards.

Looking for more investment ideas beyond Zymeworks?

If Zymeworks has sharpened your focus on stock selection, now is the time to widen your watchlist and spot other opportunities before the crowd catches on.

- Target strong long term value potential by scanning companies that screen as high quality and attractively priced through the 45 high quality undervalued stocks.

- Prioritize resilience by reviewing companies with healthier finances and sturdier fundamentals using the solid balance sheet and fundamentals stocks screener (48 results).

- Unearth overlooked opportunities by checking the screener containing 19 high quality undiscovered gems that may not yet be on most investors' radar.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.