ZYN’s FDA Modified-Risk Label Could Be A Game Changer For Philip Morris International (PM)

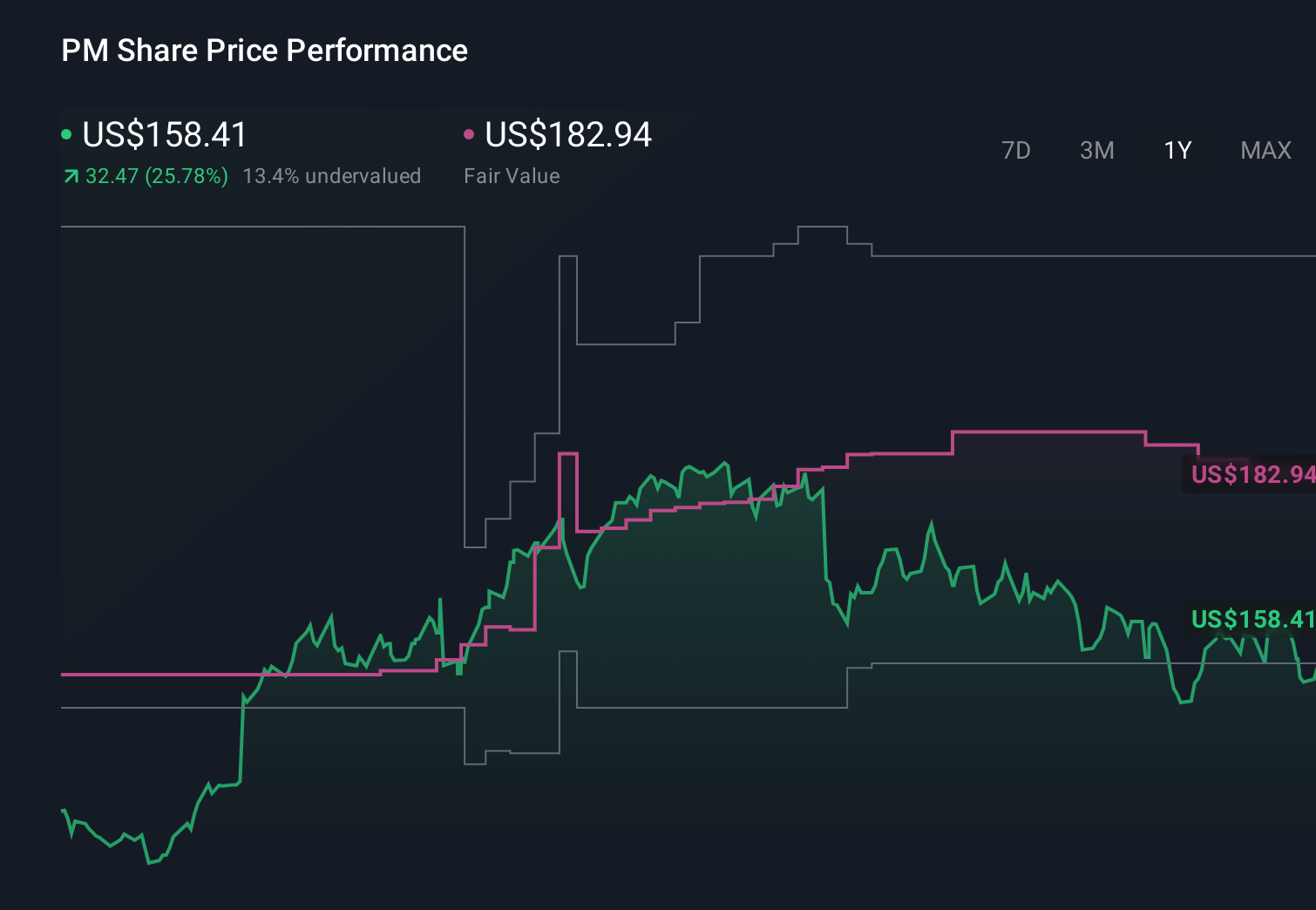

Philip Morris International Inc. PM | 0.00 |

- Philip Morris International Inc. recently announced that the U.S. Food and Drug Administration granted Modified Risk Tobacco Product orders for 20 ZYN nicotine pouch variants, authorizing marketing claims that switching from cigarettes to ZYN lowers the risk of several serious smoking-related diseases.

- This makes ZYN the first nicotine pouch range in the U.S. with MRTP status, potentially strengthening Philip Morris International’s position in smoke-free products as regulators differentiate between combustible and non-combustible nicotine.

- We’ll now examine how ZYN’s newly granted MRTP status could influence Philip Morris International’s smoke-free growth narrative and risk profile.

Uncover the next big thing with 20 elite penny stocks that balance risk and reward.

Philip Morris International Investment Narrative Recap

To own Philip Morris International, you need to believe its shift toward smoke free products can offset pressure on traditional cigarettes and regulatory risks. The FDA’s modified risk orders for ZYN reinforce that smoke free narrative in the U.S., but they do not remove key uncertainties around regulation, illicit trade and the pace of reduced risk product adoption, which still look like the most important near term catalyst and the biggest risk.

The recent US$1.0 billion prepayment on PMI’s term loan sits alongside the ZYN decision as part of a broader effort to support balance sheet resilience while investing in smoke free products. While the debt move does not directly affect the ZYN catalyst, it shapes how PMI manages high debt levels, interest costs and financial flexibility if smoke free growth, including ZYN and IQOS, does not progress as expected.

Yet behind the promise of ZYN’s MRTP status, investors still need to weigh the growing regulatory and tax risks that could materially affect...

Philip Morris International's narrative projects $49.6 billion revenue and $15.3 billion earnings by 2029. This requires 6.1% yearly revenue growth and about a $4.2 billion earnings increase from $11.1 billion today.

Uncover how Philip Morris International's forecasts yield a $193.14 fair value, a 3% upside to its current price.

Exploring Other Perspectives

Some of the most optimistic analysts already expected PMI to reach about US$54.0 billion in revenue and US$16.2 billion in earnings by 2029, so this new ZYN milestone could either support that bullish view on smoke free growth or expose how much it depends on assumptions about future regulation and consumer adoption that not every investor will share.

Explore 8 other fair value estimates on Philip Morris International - why the stock might be worth 14% less than the current price!

The Verdict Is Yours

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your Philip Morris International research is our analysis highlighting 3 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Philip Morris International research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Philip Morris International's overall financial health at a glance.

Want Some Alternatives?

Our top stock finds are flying under the radar-for now. Get in early:

- This technology could replace computers: discover 26 stocks that are working to make quantum computing a reality.

- We've uncovered the 9 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

- Find 45 companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.