In-Depth Equity Analysis: Uber Technologies, Inc. (UBER)

UBER: Undervalued Giant - Time for A Reversal in Bearish Sentiment

Company Overview:

UBER Technologies, Inc. is a global leader in mobility technology, leveraging its vast transportation network to create a comprehensive platform ecosystem. The company's core competencies span across three major segments:

- Mobility (ride-hailing)

- Delivery (food and groceries)

- Freight (logistics services)

With operations in over 70 countries, UBER has transformed from a simple ride-hailing service into a diversified technology platform, establishing strong network effects across its multiple business lines.

Growth Journey:

- Founded as a ride-sharing service, UBER began its international expansion in 2014

- Enhanced its technological capabilities through strategic acquisitions, including autonomous driving companies

- Launched Uber Eats in 2015, marking its entry into the food delivery market

- Since 2017, implemented strategic market focus:

Direct operations in core markets (North America, Latin America, and Europe)

Partnership/investment approach in other regions

Investment Thesis:

1. The global mobility market presents a favorable competitive landscape, with UBER commanding a dominant position of over 60% market share. While competitors exist, they face significant limitations:

- Lyft relies heavily on price competition in the U.S. market, raising concerns about long-term sustainability

- DiDi and other players remain focused on specific regional markets, lacking global scale

Recent financial performance validates UBER's competitive advantages:

- Consistent commission rates

- Stable profit margins

- High barriers to entry for new competitors

UBER's strong market position and operational metrics demonstrate its sustainable competitive moat, setting it apart from competitors who struggle to balance growth with profitability.

2. UBER's delivery business, now representing over 30% of total revenue, demonstrates powerful synergies with its mobility operations. The fundamental business model is similar - while ride-hailing connects drivers with passengers, delivery simply adds restaurants as an additional layer to this network.

This structural similarity enables significant operational advantages:

- Direct application of existing operational models from mobility to delivery

- Shared driver and customer base reduces market expansion costs

- Common technology platform serving both businesses

The dual-service model creates strong benefits for all participants. Drivers can increase their potential earnings by accepting both ride-hailing and delivery orders, enhancing their platform loyalty. Similarly, customers who use UBER for food delivery are more likely to use its ride-hailing service, creating a self-reinforcing ecosystem that strengthens user retention and platform stickiness.

This integrated approach has proven highly effective in:

- Reducing customer acquisition costs

- Increasing platform engagement

- Building sustainable competitive advantages

- Maximizing resource utilization

3. The market's previous concerns about UBER's valuation centered on autonomous driving disrupting its core business. However, this perspective overlooks two critical factors:

First, the timeline for commercial autonomous driving deployment:

- Market expectations appear overly optimistic

- Mass commercialization of autonomous taxis faces significant technological and regulatory hurdles

- The path to widespread adoption remains uncertain

Second, the business model dynamics:

- Autonomous vehicle companies (tech startups and EV giants) are unlikely to operate large-scale taxi fleets

- Fleet ownership requires significant capital investment and high fixed costs

- This asset-heavy model contradicts these companies' core competencies

UBER's competitive advantages remain strong:

- Massive user base

- Sophisticated dispatch and operations expertise

- Established market presence

The emerging business model appears to be collaborative rather than competitive, as evidenced by UBER's partnership with Waymo, allowing customers to book autonomous Waymo vehicles through UBER's platform. This suggests UBER is well-positioned to integrate autonomous vehicles into its existing ecosystem rather than being disrupted by them.

4. Following the significant stock price correction, UBER's current valuation appears attractive:

Key valuation metrics:

- P/E (TTM): approximately 32x

- P/S ratio: around 3.3x, near historical median

These valuations are particularly noteworthy considering:

- UBER only achieved profitability in 2023

- Current P/S ratio aligns with historical averages

At these levels, UBER presents an attractive value proposition, offering a compelling entry point for investors considering the company's market leadership, improving profitability, and strong competitive position.

Fundamental Analysis:

UBER's business is built on three core segments: Mobility, Delivery, and Freight. As of 2023, the platform has achieved remarkable scale with 150 million monthly active users and over 7.4 million active drivers and couriers.

Revenue Distribution:

Mobility business:

The Mobility business, which focuses on ride-hailing services, demonstrates UBER's market dominance. The company has established a strong first-mover advantage from its early market entry, resulting in a global market share that now exceeds 60%. For markets where UBER doesn't operate directly, the company employs a strategic approach of securing market exposure through partnerships and equity investments. A prime example of this strategy is UBER's 2016 decision to exit the Chinese market by selling its operations to DiDi and becoming a DiDi shareholder, effectively maintaining a stake in the Chinese market while avoiding direct competition.

In the mobility segment, UBER generates revenue primarily through commission fees from rides. While the take rate (commission percentage) was significantly affected during the pandemic period, it has since recovered and stabilized at approximately 30%. The major cost components for this segment include driver incentives, insurance coverage, and other driver-related expenses. The business has now achieved a stable operational state with predictable performance metrics.

Delivery Business:

The delivery segment represents approximately 30% of UBER's total revenue. The business model, similar to mobility, is commission-based, but targets restaurants and merchants instead of drivers. The current commission rate stands at around 20%. The relatively lower market share of approximately 20% globally, despite having presence in multiple markets worldwide, may be attributed to UBER's later entry into the delivery business compared to its mobility operations.

The delivery market presents unique challenges as each country and region has its own localized competitors. A prime example is DoorDash in the United States, which leveraged its first-mover advantage to capture over 60% market share. UBER's growth strategy in this segment focuses on two key aspects: leveraging synergies with its mobility business to expand its user base, and utilizing its proven operational expertise to enhance customer satisfaction.

Freight Business:

The freight segment currently represents a relatively small portion of UBER's revenue, accounting for approximately 10%. The business model follows a similar pattern to other segments, connecting shippers with carriers, and generating revenue through commission fees of around 20% of the total freight charges.

Although the current revenue contribution is modest, this segment holds significant potential as UBER's third growth trajectory. If UBER can successfully apply its expertise and operational experience from mobility and delivery businesses to the freight segment and successfully expand into global markets, it could become a substantial growth driver for the company.

Risk Factors:

1.Global macroeconomic risks: If the global economy performs below expectations, consumer spending might be negatively impacted, potentially affecting UBER's revenue. A significant economic downturn could reduce consumers' willingness to spend on ride-hailing and delivery services.

2.Regulatory risks: Changes in policies and regulations could require UBER to increase expenditure on driver-related costs, particularly in areas such as insurance coverage and benefits for platform-registered drivers.

3.Market competition risks: Although UBER has established itself as a leader in both mobility and delivery sectors, intense market competition persists. This competitive pressure could potentially lead to revenue decline if UBER fails to maintain its market position.

4.Autonomous vehicle technology risks: The rapid advancement of autonomous driving technology poses both an opportunity and a threat. If UBER fails to keep pace with this technological evolution, it risks falling behind in the mobility sector, particularly as self-driving technology continues to develop faster than expected.

Research Report Appendix

Company Concept:

UBER Technologies, Inc. is a global leader in mobility technology, leveraging its vast transportation network to create a comprehensive platform ecosystem. The company's core competencies span across three major segments: Mobility (ride-hailing), Delivery (food and groceries) and Freight (logistics services)

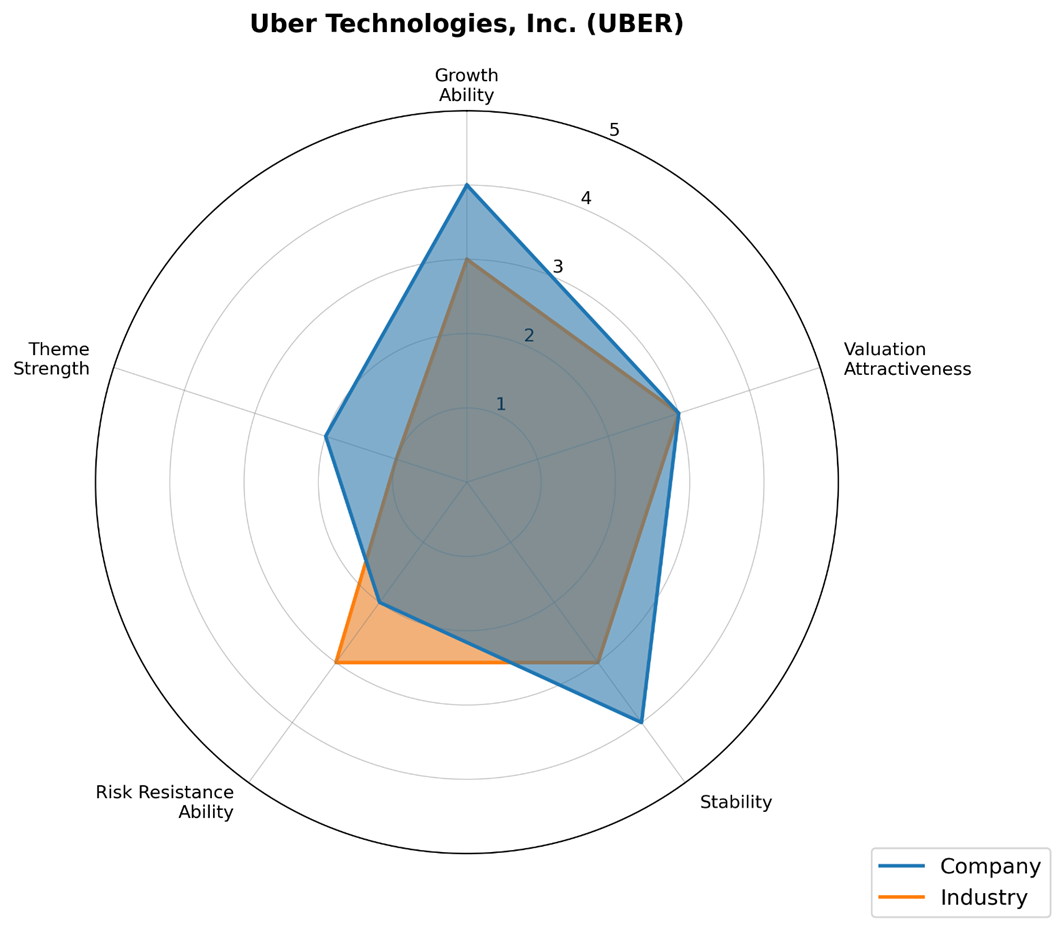

Dimension | UBER | Industry |

Growth | 4 | 3 |

Valuation Attractiveness | 3 | 3 |

Stability | 4 | 3 |

Risk Resistance | 2 | 3 |

Theme Strength | 2 | 1 |

Overall Score | 15 | 13 |

Model Explanation:

The model primarily evaluates companies and industries across five dimensions: growth ability, valuation attractiveness, stability, risk resistance ability, and theme strength. Each dimension is scored from 1-5, with 1 being the lowest and 5 the highest. Overall, higher scores indicate stronger fundamentals. For each dimension, a multi-factor model will be constructed based on industry and historical data of selected stocks, and a quantitative model will be used to automatically score each dimension.

Here are the dimensions explained:

- Growth Ability: Measures future performance potential; higher growth rates yield higher scores.

- Valuation Attractiveness: Assesses stock valuation; lower valuations earn higher scores.

- Stability: Evaluates the consistency of profit generation; greater stability means higher scores.

- Risk Resistance: Gauges the capacity to endure macroeconomic changes; better risk resistance leads to higher scores.

- Theme Strength: Rates market favor for the stock in the short term; increased favor results in higher scores.

Disclaimer:

The Information presented above is for information purposes only, which shall not be intended as and does not constitute an offer to sell or solicitation for an offer to buy any securities or financial instrument or any advice or recommendation with respect to such securities or other financial instruments or investments. When making a decision about your investments, you should seek the advice of a professional financial adviser and carefully consider whether such investments are suitable for you in light of your own experience, financial position and investment objectives. The firm and its analysts do not have any material interest or conflict of interest with any stocks mentioned in this report.

IN NO EVENT SHALL SAHM CAPITAL FINANCIAL COMPANY BE LIABLE FOR ANY DAMAGES, LOSSES OR LIABILITIES INCLUDING WITHOUT LIMITATION, DIRECT OR INDIRECT, SPECIAL, INCIDENTAL, CONSEQUENTIAL DAMAGES, LOSSES OR LIABILITIES, IN CONNECTION WITH YOUR RELIANCE ON OR USE OR INABILITY TO USE THE INFORMATION PRESENTED ABOVE, EVEN IF YOU ADVISE US OF THE POSSIBILITY OF SUCH DAMAGES, LOSSES OR EXPENSES.