Please use a PC Browser to access Register-Tadawul

Get It

3 Growth Companies With Insider Ownership Up To 27%

AppLovin APP | 462.14 | -3.19% |

As the U.S. stock market reaches new heights, with the S&P 500 closing at a record high following robust economic growth, investors are increasingly focused on identifying promising opportunities in this buoyant environment. In such conditions, stocks of growth companies with significant insider ownership can be particularly appealing, as they often indicate strong confidence from those most familiar with the company's potential and strategic direction.

| Name | Insider Ownership | Earnings Growth |

| Super Micro Computer (SMCI) | 13.9% | 50.7% |

| StubHub Holdings (STUB) | 14.1% | 74% |

| SES AI (SES) | 12% | 68.9% |

| Niu Technologies (NIU) | 37.2% | 93.7% |

| Credo Technology Group Holding (CRDO) | 10.1% | 30.7% |

| Corcept Therapeutics (CORT) | 11.4% | 52.7% |

| Cloudflare (NET) | 10.2% | 43.5% |

| Atour Lifestyle Holdings (ATAT) | 18% | 24.4% |

| Astera Labs (ALAB) | 11.7% | 29.0% |

| AppLovin (APP) | 27.4% | 27.1% |

Let's uncover some gems from our specialized screener.

Simply Wall St Growth Rating: ★★★★★★

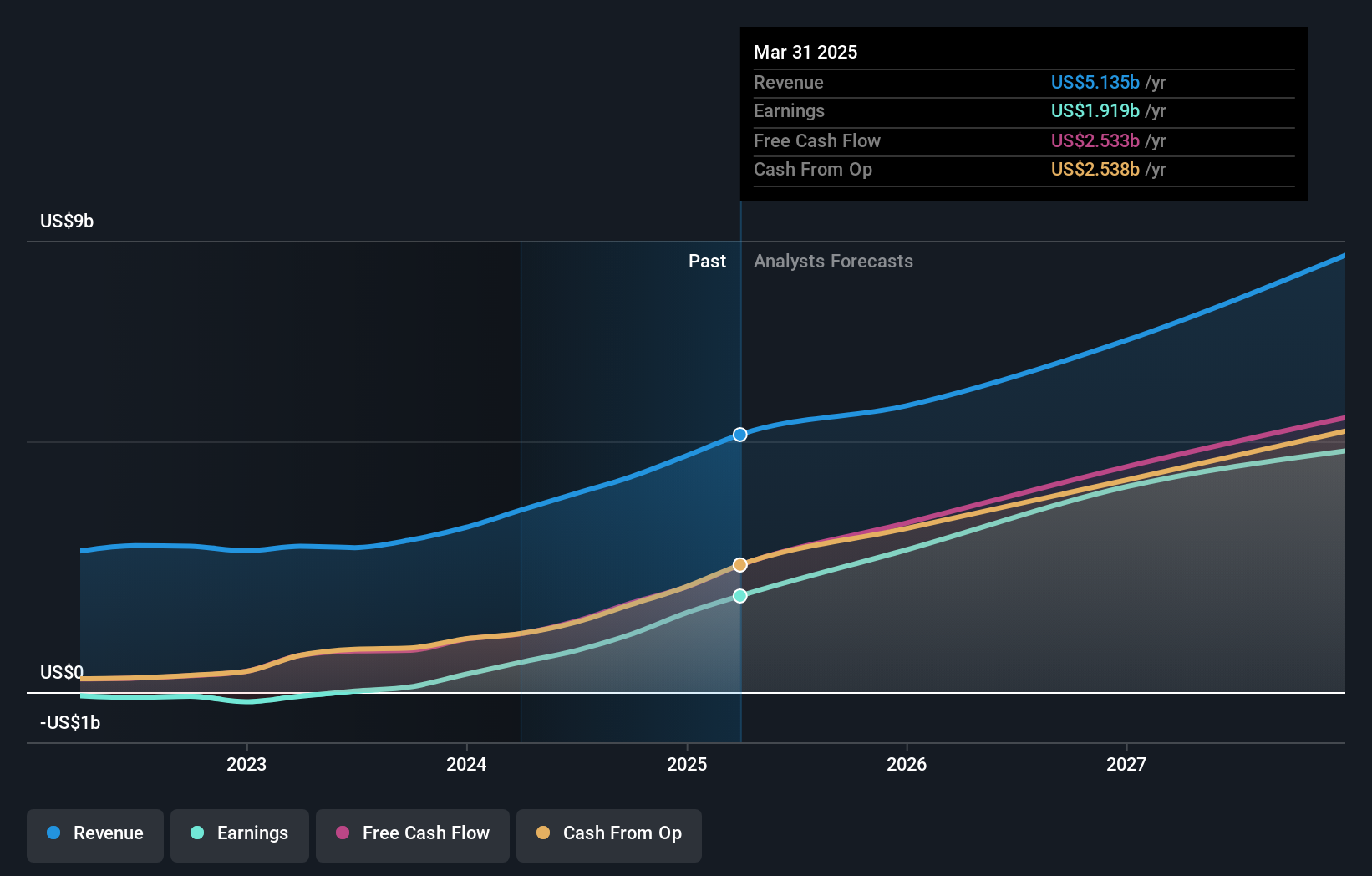

Overview: AppLovin Corporation develops a software-based platform aimed at improving marketing and monetization for advertisers both in the United States and internationally, with a market cap of approximately $246.18 billion.

Operations: The company's revenue is primarily derived from its advertising segment, which generated $4.82 billion.

Insider Ownership: 27.4%

AppLovin demonstrates strong growth potential with earnings forecasted to increase 27.1% annually, outpacing the US market's 16.2%. Revenue is expected to grow at 20.5% per year, surpassing market averages. Despite high debt levels, the company reported significant Q3 sales of US$1.41 billion and net income of US$835.55 million, reflecting robust performance compared to last year. Insider activity shows more buying than selling recently, though no substantial purchases occurred in the past three months.

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Chime Financial, Inc. is a financial technology company that offers digital consumer banking and payment solutions, with a market cap of approximately $9.94 billion.

Operations: Chime Financial generates $2.07 billion in revenue from its business services segment, focusing on digital banking and payment solutions.

Insider Ownership: 10.3%

Chime Financial is poised for growth, with revenue expected to grow 17.9% annually, surpassing the US market average. Recent executive promotions aim to enhance strategic initiatives and customer experience. Despite a net loss of US$54.72 million in Q3 2025, Chime raised its earnings guidance for the year, projecting revenue between $2.16 billion and $2.17 billion—an increase of nearly 30%. Its addition to the S&P Global BMI Index underscores its expanding market presence.

Simply Wall St Growth Rating: ★★★★★☆

Overview: Sable Offshore Corp. is an independent oil and gas company operating in the United States with a market cap of $1.10 billion.

Operations: Sable Offshore Corp.'s revenue segments are not specified in the provided information.

Insider Ownership: 15.1%

Sable Offshore is forecasted to grow its revenue significantly faster than the US market, with an expected annual increase of 82%. Despite a substantial net loss in recent quarters, the company aims to become profitable within three years. Recent management changes and strategic financing moves, including a $250 million private placement and shelf registration closure of $254.55 million, indicate efforts to strengthen its financial position amidst ongoing legal challenges with the California Coastal Commission.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.The analysis only considers stock directly held by insiders. It does not include indirectly owned stock through other vehicles such as corporate and/or trust entities. All forecast revenue and earnings growth rates quoted are in terms of annualised (per annum) growth rates over 1-3 years.