Please use a PC Browser to access Register-Tadawul

Get It

A Closer Look at nLIGHT (LASR) Valuation After Recent 14% Share Price Surge

NLIGHT, INC. LASR | 66.49 66.49 | +4.23% 0.00% Post |

nLIGHT's latest surge builds on a stunning run this year. A 1-day share price return of nearly 15% has pushed its year-to-date gain to an eye-catching 228%. With a 1-year total shareholder return topping 200% and momentum still strong, the stock’s recent moves suggest investors are increasingly optimistic about its prospects, possibly spotting growth potential that the market once overlooked.

If nLIGHT’s rapid gains have you thinking bigger, this could be the perfect moment to discover See the full list for free.

After such a dramatic rally and with shares now trading just below analyst targets, the big question is whether nLIGHT is still an underappreciated bargain or if markets have already priced in all the future growth.

With nLIGHT shares closing at $34.16 and the narrative fair value at $35.58, the stock is seen as modestly undervalued by those tracking company fundamentals. This perspective is built on a foundation of growing revenues, strong sector demand, and progress in operational execution.

The rapid growth and expanding pipeline in aerospace and defense, particularly around high-power laser solutions (e.g., HELSI-2 program, DE M-SHORAD, Golden Dome initiative, and increased directed energy orders internationally), positions nLIGHT to benefit from rising global defense spending and modernization, supporting strong multi-year revenue growth.

Want to know what powers this sky-high narrative? Analysts are betting on a mix of ambitious revenue growth, higher margins, and valuation multiples typically reserved for sector standouts. Eager to discover if these bullish assumptions hold the secret to nLIGHT’s projected upside? The financial logic behind the price target might surprise you.

Result: Fair Value of $35.58 (UNDERVALUED)

However, potential weakness in commercial sales or delays in key defense programs could quickly undermine nLIGHT’s bullish outlook and challenge the case for continued upside.

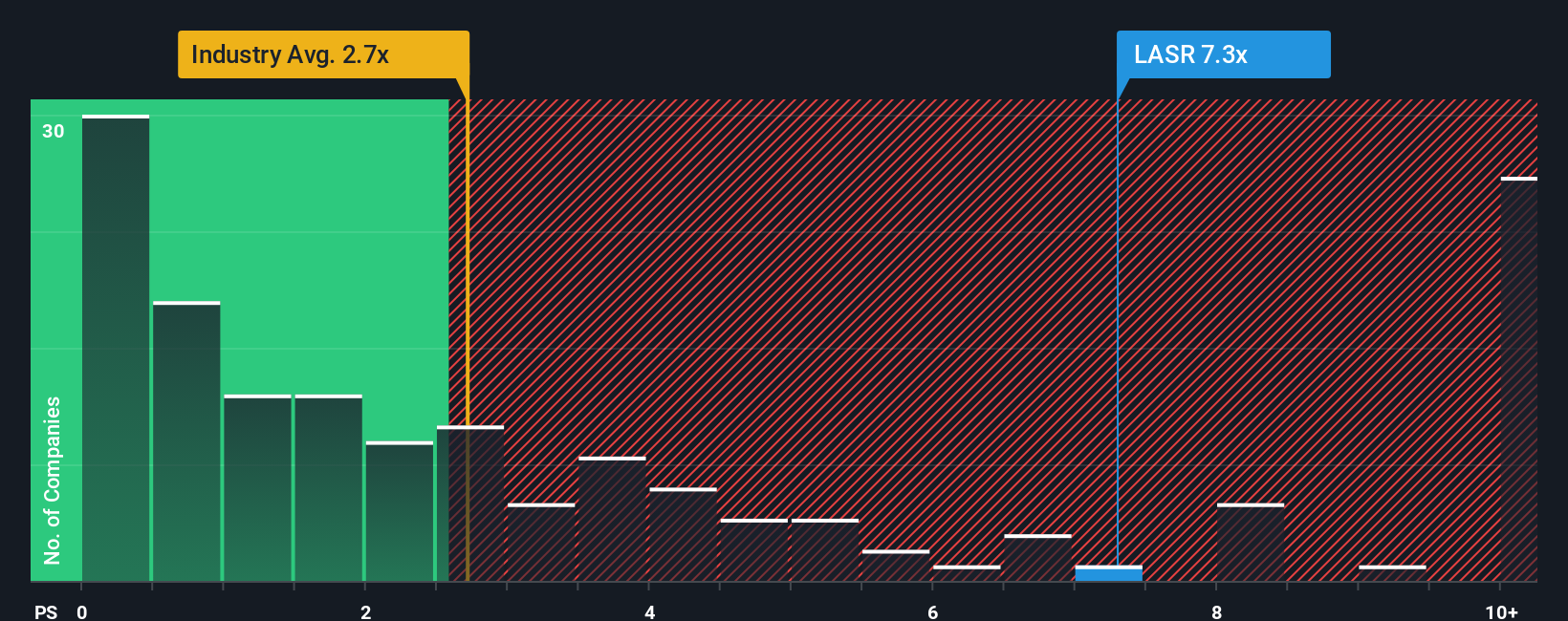

While the fair value model paints nLIGHT as modestly undervalued, traditional market pricing tells a different story. The company’s price-to-sales ratio is 7.5x, which is significantly higher than both its industry peers at 2.6x and an estimated fair ratio of 1.5x. This steep gap signals that investors are paying a hefty premium, introducing greater valuation risk if growth expectations slip.

If this analysis doesn't match your perspective or you’d rather see the story your way, dive into the numbers and shape your own insights in under three minutes, then Do it your way

A great starting point for your nLIGHT research is our analysis highlighting 1 key reward and 3 important warning signs that could impact your investment decision.

Make your next smart move by searching handpicked opportunities using the Simply Wall Street Screener. Don’t let standout stocks and market trends pass you by. See what else is available right now.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.