Please use a PC Browser to access Register-Tadawul

Get It

A Look At Centessa Pharmaceuticals (CNTA) Valuation After New Analyst Focus On Orexin Pipeline Expansion

Centessa Pharmaceuticals PLC ADR CNTA | 22.20 | -0.89% |

Recent analyst coverage has focused on Centessa Pharmaceuticals (CNTA) after Needham and Oppenheimer highlighted the company’s orexin agonist pipeline and noted a planned clinical expansion, including key ORX-750 and follow-on program trials.

Analyst enthusiasm around the orexin pipeline comes after a mixed short term stretch for the stock, with a 30 day share price return of a 15.43% decline, set against a 1 year total shareholder return of 43.35% and a very large 3 year total shareholder return, which suggests longer term momentum has been strong even as recent moves cool.

If Centessa’s story has you looking at other potential healthcare names, this could be a helpful moment to scan healthcare stocks for more ideas across the sector.

With shares pulling back about 15% over the past month yet still showing a very large 3 year total return and trading below some analysts’ price targets, you have to ask: is this a genuine opportunity, or is the market already pricing in future growth?

On a P/B basis, Centessa Pharmaceuticals looks expensive at 10.9x compared with the US Biotechs industry average of 2.7x, even though the shares closed at $22.42.

P/B compares a company’s market value to the book value of its net assets. This can matter for a clinical stage pharma group where tangible equity and cash resources are key reference points. A higher multiple often reflects strong expectations for future value creation relative to the current balance sheet.

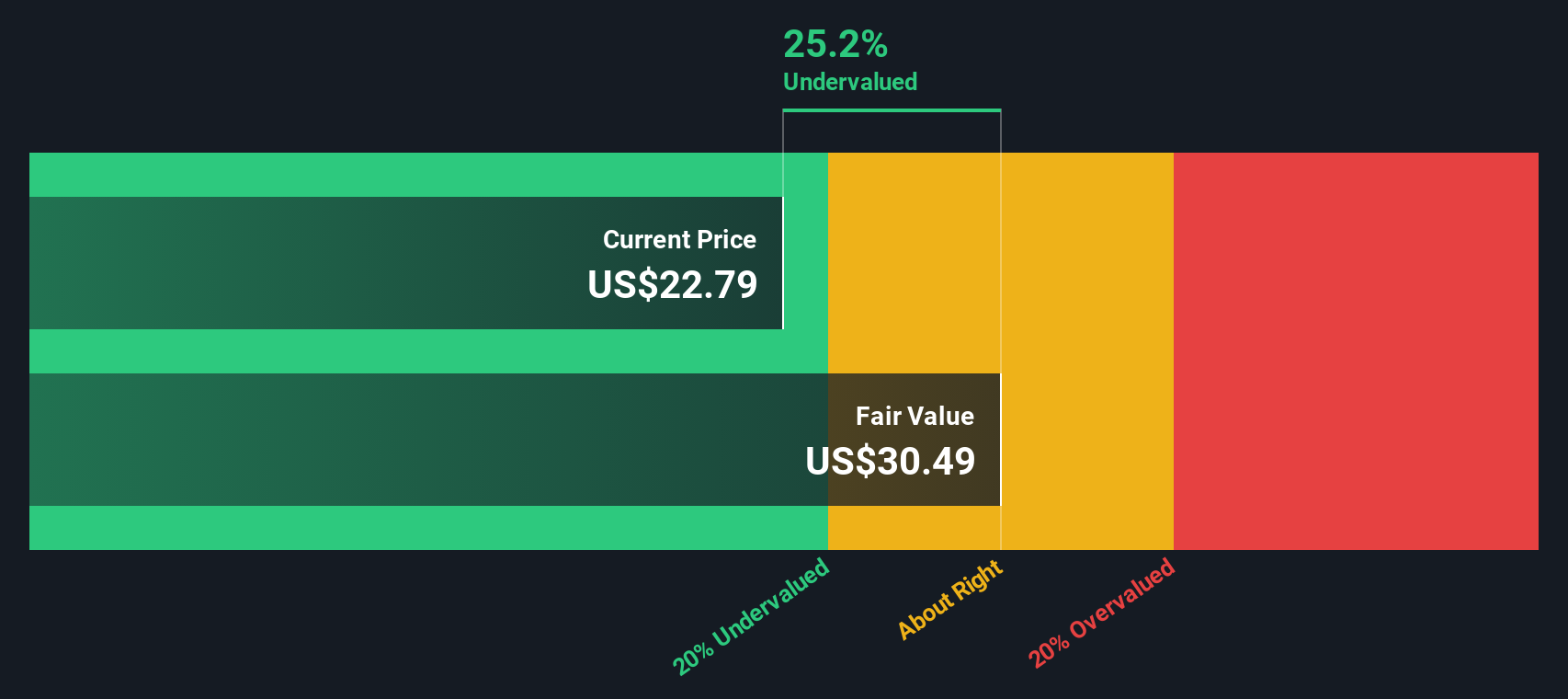

Here, the SWS DCF model points to an estimate of fair value of $205.20 per share. The market is assigning a much lower price and a relatively high P/B versus the broader biotech industry. The DCF result suggests investors are pricing Centessa’s equity more cautiously than that cash flow based estimate, even as the balance sheet multiple sits at the top end of sector levels.

Compared with peers on 2.7x P/B, Centessa’s 10.9x stands out as materially higher. This implies the market is attributing a much richer value to its pipeline and future prospects than to the average biotech name, even if that still falls well short of the SWS DCF fair value figure.

Result: Price to Book of 10.9x (ABOUT RIGHT)

However, you also have to weigh clinical trial uncertainty around ORX750 and related programs, as well as the current net loss of $242.698 million on just $15 million of revenue.

While the 10.9x P/B ratio makes Centessa look expensive next to the US Biotechs average of 2.7x, the SWS DCF model presents a different perspective. At a fair value estimate of US$205.20 per share compared with the current US$22.42 price, the model suggests the stock is heavily undervalued. If both views are based on real data, which one do you think the market may reflect over time?

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Centessa Pharmaceuticals for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 882 undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

If you see the figures differently or prefer to rely on your own work, you can review the data and form your own Centessa view in just a few minutes, then Do it your way.

A great starting point for your Centessa Pharmaceuticals research is our analysis highlighting 2 key rewards and 1 important warning sign that could impact your investment decision.

If Centessa has sharpened your focus, do not stop here. Broaden your watchlist with structured screeners that surface clear themes and specific types of opportunities.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.