Please use a PC Browser to access Register-Tadawul

Get It

A Look at First Advantage (FA) Valuation Following Analyst Upgrades and Raised Earnings Projections

First Advantage Corp. FA | 9.85 | +2.60% |

First Advantage has recently seen its stock price climb as analysts across the board have revised earnings projections higher. This trend points to growing confidence in the firm's near-term outlook and performance.

The recent momentum in First Advantage’s share price stands out, with a 1-month share price return of nearly 10% and analyst upgrades sparking renewed interest. While the stock has faced pressure over the past year, as reflected in its -28% total shareholder return, the market’s tone has shifted more positive in recent weeks as confidence grows around future prospects.

If you're looking for other compelling growth stories that may not be on your radar, now is a great moment to broaden your scope and discover fast growing stocks with high insider ownership

With shares rebounding and analyst targets suggesting notable upside, investors are left to wonder if First Advantage represents an undervalued opportunity right now, or if the market has already accounted for its next phase of growth.

Based on the popular narrative, First Advantage's fair value is set well above the latest closing price, which suggests notable upside if projections are realized. The narrative outlines key catalysts behind this perceived opportunity and sets a high bar for future performance.

Ongoing investments in proprietary AI-enabled technology, automation, and integrated platforms (particularly following the Sterling acquisition) are unlocking operational efficiencies and enabling more high-margin value-added services. This creates potential for margin expansion and higher net earnings.

Want to know what future milestones justify this bullish outlook? The narrative’s case hinges on sharp increases in revenue, profit margins, and a valuation multiple that is rare in this segment of the market. Uncover the projections shaping this verdict—there is more drama in the forecasts than meets the eye.

Result: Fair Value of $17.43 (UNDERVALUED)

However, ongoing macroeconomic headwinds and uncertainty in hiring demand could threaten growth expectations and potentially challenge the current positive narrative for First Advantage.

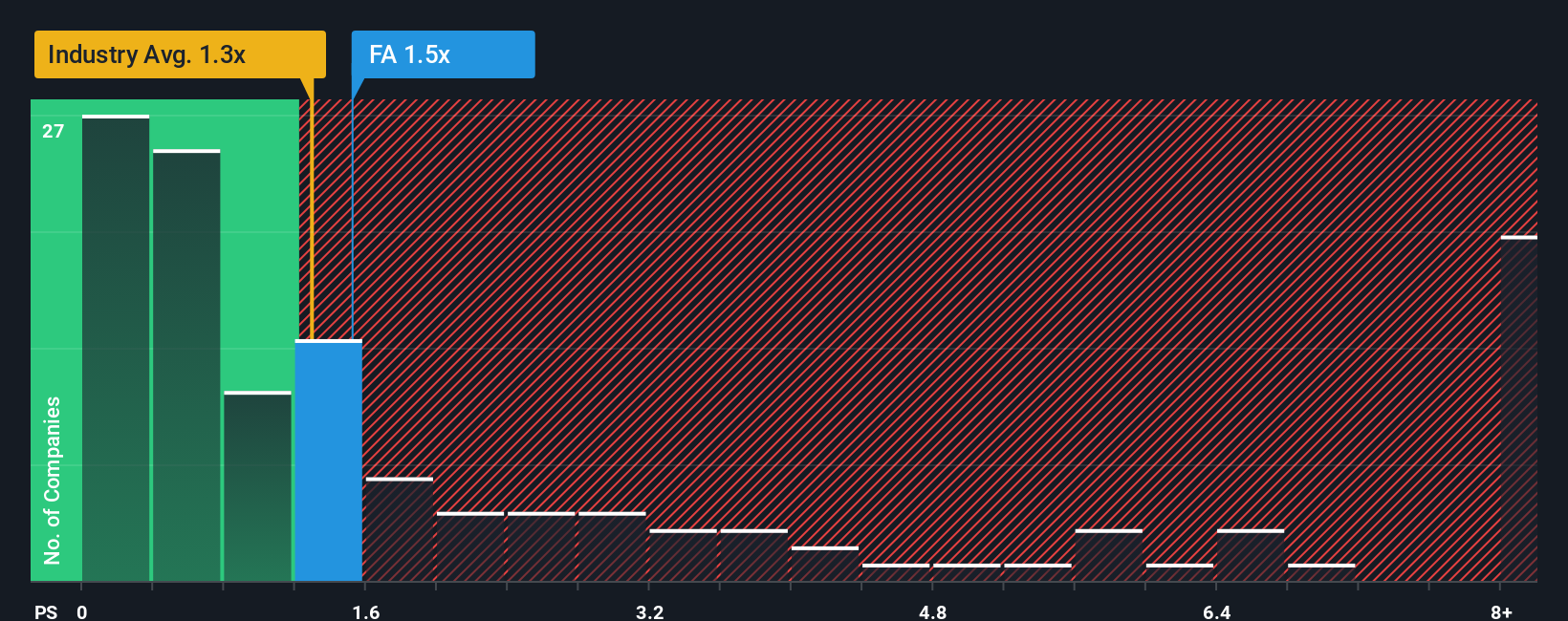

Looking at valuation through the lens of the price-to-sales ratio, First Advantage appears more expensive than industry norms. The company’s ratio of 1.7x sits above both the US Professional Services industry average of 1.3x and the peer average of 1.4x, as well as the fair ratio of 1.6x. This gap could mean investors should weigh whether the rapid rebound is already priced in, or if the market might eventually bring the valuation back in line with its peers.

If you want to take a hands-on approach or see things from a different angle, you can put together your own narrative in just a few minutes. Do it your way

A good starting point is our analysis highlighting 3 key rewards investors are optimistic about regarding First Advantage.

Smart investors do not settle for just one opportunity. Use these targeted stock screeners to unearth investments others are missing and stay ahead of the market shift.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.