Please use a PC Browser to access Register-Tadawul

Get It

A Look At Invitation Homes (INVH) Valuation After Trump Administration Curbs Institutional Single Family Home Purchases

Invitation Homes, Inc. INVH | 24.39 | -2.44% |

The Trump administration’s sudden move to block large institutional investors from buying additional single-family homes has put Invitation Homes (INVH) directly in focus, as markets reassess its growth options and long term business model.

At a share price of US$27.02, Invitation Homes has seen a 6.41% decline in its 90 day share price return and an 8.01% drop in its 1 year total shareholder return, suggesting momentum has recently weakened as investors react to new regulatory headline risk, the ResiBuilt acquisition and upcoming earnings.

If the policy shock around institutional homeownership has you rethinking where growth could come from next, it might be worth widening your search to fast growing stocks with high insider ownership.

With Invitation Homes trading at US$27.02 and screens flagging an intrinsic discount of around 39%, the key question is simple: are you looking at a mispriced REIT here, or is the market already factoring in all the future growth?

With Invitation Homes at $27.02 against a most followed fair value of about $33.80, the narrative suggests a sizeable gap for investors to think about.

The company's concentrated investments and expansion in high-growth Sun Belt and suburban markets align with population migration trends, creating opportunities for above-average rental rate increases and boosted property appreciation, directly supporting both revenue and asset value growth.

Curious what kind of revenue climb, margin path, and future earnings multiple are baked into that fair value line? The full narrative explains the specific growth mix, the implied profitability shift, and the valuation bridge that connects today’s price to that higher figure.

Result: Fair Value of $33.80 (UNDERVALUED)

However, that upside story runs into real questions around tighter rules on institutional homeownership and rising property tax and insurance costs in key markets, which could pressure returns.

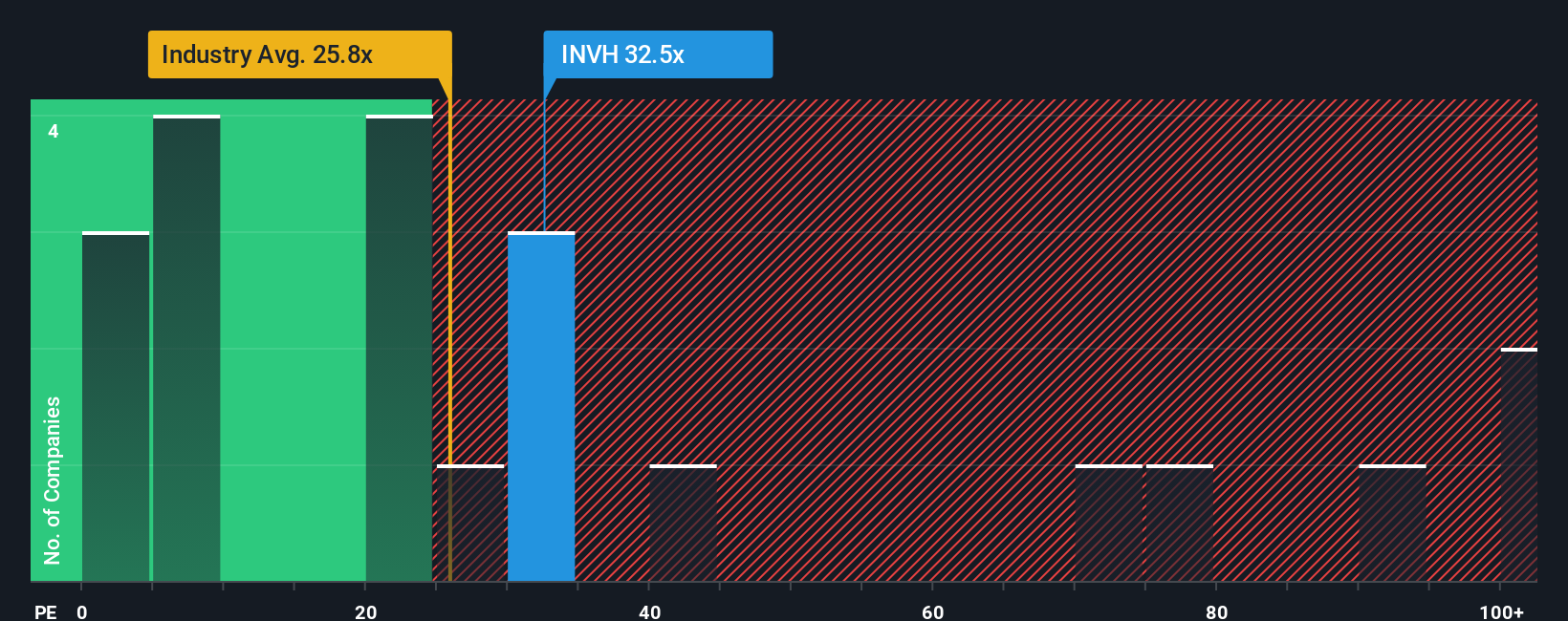

While our DCF model points to value, the market is less generous when you look at P/E. Invitation Homes trades at about 28.3x earnings, compared with 26.7x for peers and 25.4x for the North American Residential REITs group, yet its fair ratio is 29.4x. That gap is small enough that any earnings wobble or sentiment shift could matter a lot more than a neat theoretical discount. Which signal do you trust more right now?

If you see the numbers differently or want to stress test your own assumptions, you can build a custom thesis in just a few minutes with Do it your way.

A great starting point for your Invitation Homes research is our analysis highlighting 3 key rewards and 3 important warning signs that could impact your investment decision.

If you stop with one stock, you risk missing better fits for your goals, so keep testing ideas until the numbers and story really line up for you.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.