Please use a PC Browser to access Register-Tadawul

Get It

A Look At iRhythm Holdings (IRTC) Valuation After Recent Share Price Volatility

iRhythm Holdings, Inc. IRTC | 117.17 | -0.30% |

iRhythm Holdings (IRTC) has drawn fresh attention after a mixed stretch in its share performance, with a gain of 3.7% over the past day contrasted against negative returns over the past week, month, and past 3 months.

For investors, that combination of short term strength and recent weakness raises questions about how the current US$154.51 share price lines up with the company’s business profile, financial results, and longer term track record.

Zooming out, the recent pullback, including a 30 day share price return of an 11.82% decline and a 90 day share price return of a 16.48% decline, sits alongside a 1 year total shareholder return of 41.95%. This suggests that longer term momentum has been stronger than the latest moves imply.

If iRhythm’s swings have you reassessing your watchlist, it could be a good moment to broaden your research with healthcare peers using our healthcare stocks.

With iRhythm still loss making on US$702.573m of revenue and trading at US$154.51, investors may be considering whether the recent pullback leaves room for upside or if the market is already pricing in its future growth.

Compared with the last close at $154.51, the most followed narrative pegs iRhythm’s fair value at $220.60, implying a sizable valuation gap driven by growth and profitability assumptions.

Investment in the Zio ecosystem, including next generation patches, enhanced form factors, and AI powered analytics (such as the Lucem Health partnership), is improving product differentiation, diagnostic yield, and workflow efficiency. This is likely leading to higher gross margins and operating leverage as software and data become a larger component of the business.

Want to see what kind of revenue ramp and margin lift have to line up to support that price tag? The narrative leans heavily on future profitability, premium earnings multiples, and sustained top line growth assumptions. Curious how those pieces fit together into a $220.60 fair value for a company that is still reporting losses today?

Result: Fair Value of $220.60 (UNDERVALUED)

However, this hinges on execution, and regulatory setbacks or a slower than expected ramp with key channel partners could quickly challenge the US$220.60 fair value narrative.

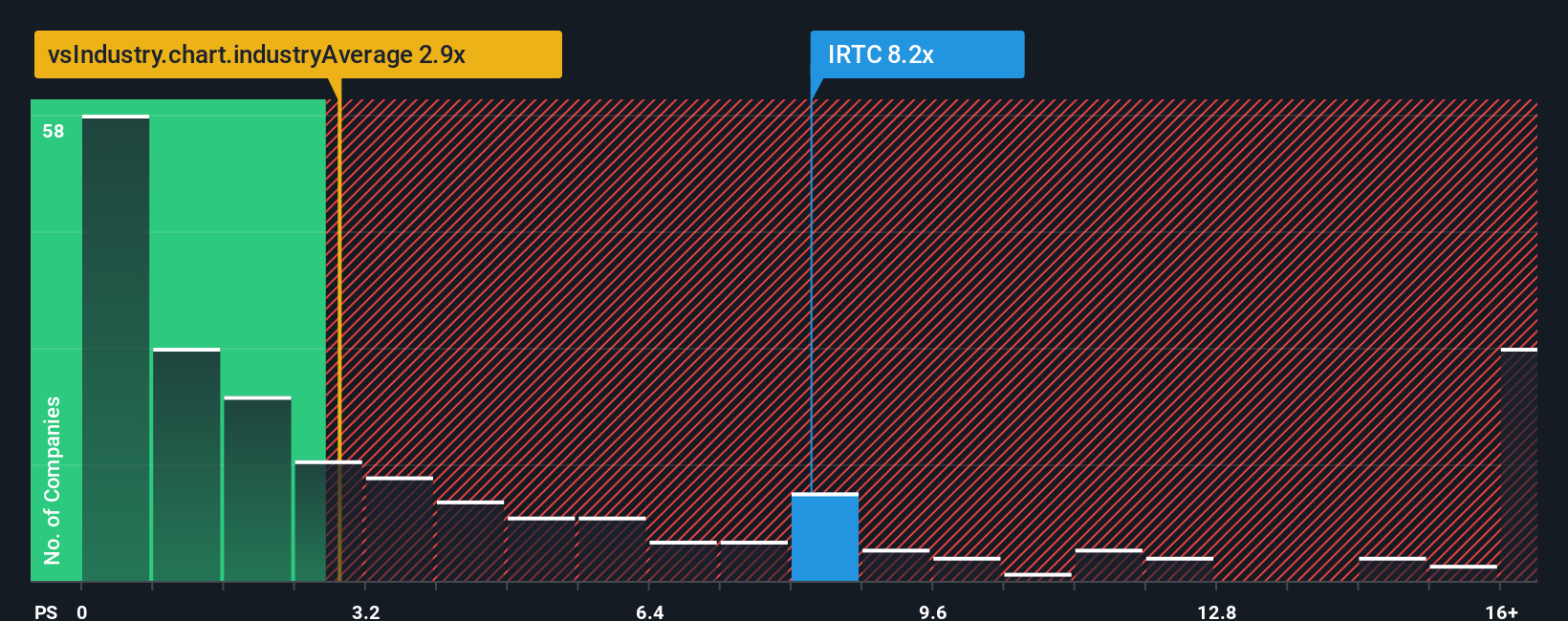

That 30% undervalued narrative leans heavily on future earnings and premium P/E multiples. Our fair ratio work using the P/S metric points the other way, with iRhythm at 7.1x sales versus a 4.5x fair ratio, 5x for peers, and 3.2x for the wider US Medical Equipment group. For you, that gap raises a simple question: is this growth story priced a little too confidently today?

If you think this story misses something, or you would rather test the numbers yourself, you can build a custom view in just a few minutes, starting with Do it your way.

A great starting point for your iRhythm Holdings research is our analysis highlighting 2 key rewards and 1 important warning sign that could impact your investment decision.

If iRhythm has sharpened your focus on valuations and growth stories, do not stop here, fresh ideas often show up where you are not currently looking.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.