Please use a PC Browser to access Register-Tadawul

Get It

A Look At Molson Coors (TAP) Valuation After Weaker Q3 Sales And Earnings Results

Molson Coors Beverage Company Class B TAP | 48.99 | +1.98% |

Molson Coors Beverage (TAP) recently reported quarterly results with a 2.3% decline in net sales and a 7.2% drop in adjusted EPS versus last year, missing analyst expectations and drawing a cautious reaction.

Despite the weaker quarterly report, the recent price action has been firm, with a 1 month share price return of 10.53% and a 3 month share price return of 17.10%. The 5 year total shareholder return of 40.28% contrasts with a 1 year total shareholder return of negative 3.65%, suggesting momentum has picked up lately after a softer patch.

If this earnings update has you reassessing your watchlist, it could be a good moment to broaden your search with our screener of 23 top founder-led companies.

With Molson Coors posting weaker Q3 numbers but carrying a value score of 5 and an indicated intrinsic discount of 67%, you have to ask: is this a genuine mispricing or has the market already accounted for its future?

Molson Coors Beverage's most followed narrative puts fair value at about $51.10, slightly below the last close at $54.38, which sets up an interesting tension between model and market.

Molson Coors' expansion into above premium and non beer beverage categories (e.g., Fever Tree mixers, seltzers, flavored malt beverages) positions it to capitalize on shifting consumer preferences for higher quality, better for you, and non alcoholic options, which should drive higher margin revenue growth in future periods.

Growth and premiumization in international segments, especially ongoing success of Madri and Peroni in EMEA/APAC and distribution runway for Banquet in the US, indicate strong potential for margin expansion and top line growth as global urbanization and rising disposable incomes support higher long term beverage consumption.

Curious how a flat revenue path still supports that fair value, a higher future P/E and a profit step up by 2028? The full narrative lays out the cash flow curve, the margin tweaks and the share count assumptions that hold this valuation together.

Result: Fair Value of $51.10 (OVERVALUED)

However, there are clear pressure points too, including weaker U.S. beer volumes and volatile aluminum costs. These factors could squeeze margins and challenge the fair value story.

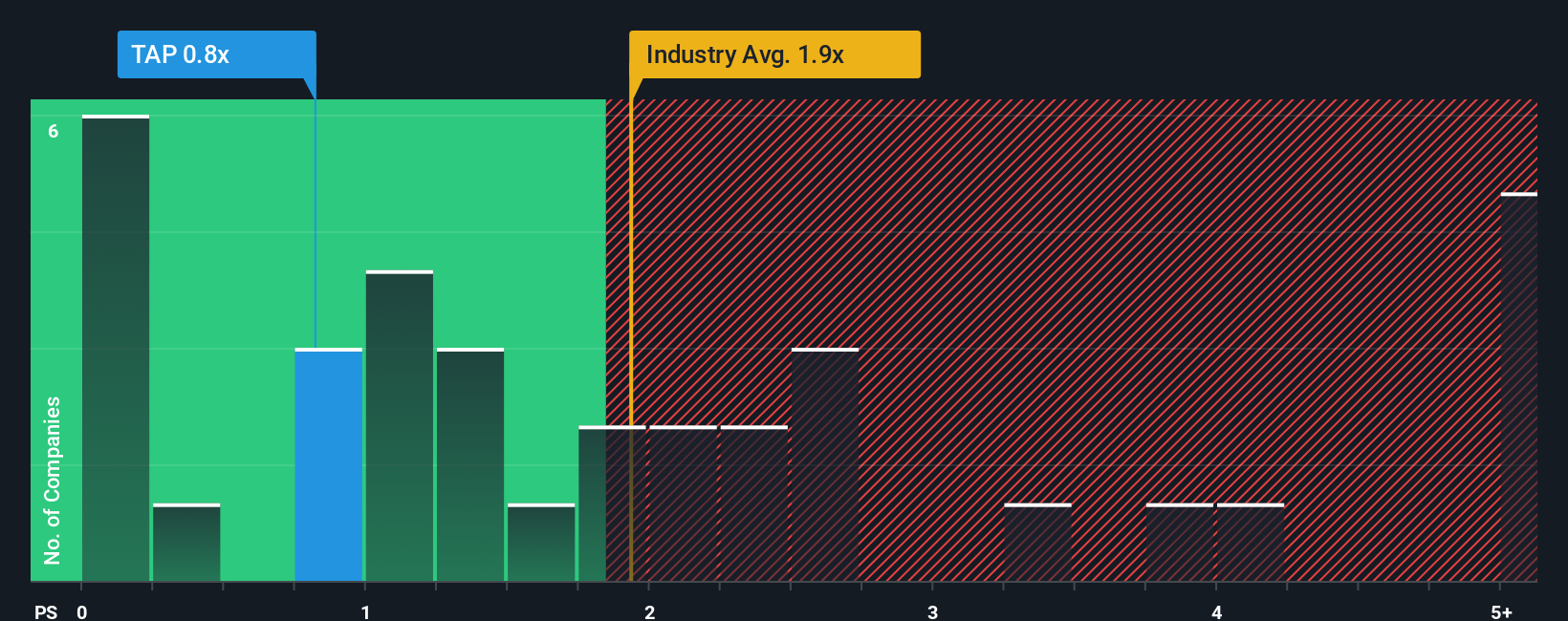

While the most popular narrative puts fair value around $51.10 and tags Molson Coors as 6.4% overvalued, the current P/S of 1x looks modest next to the US Beverage industry at 2.1x and a fair ratio of 1.3x. If the market edges closer to that fair ratio, does today’s discount reflect risk or opportunity?

If you see the numbers differently or prefer to test your own assumptions, you can shape a complete view in just a few minutes: Do it your way.

A great starting point for your Molson Coors Beverage research is our analysis highlighting 3 key rewards and 2 important warning signs that could impact your investment decision.

If Molson Coors is on your radar, do not stop there. Widen your search now or you risk missing opportunities sitting in plain sight.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.