Please use a PC Browser to access Register-Tadawul

Get It

A Look At Nutanix (NTNX) Valuation After Dual Analyst Downgrades On Growth Concerns

Nutanix, Inc. Class A NTNX | 39.13 39.13 | +2.33% 0.00% Pre |

Barclays and Morgan Stanley both downgraded Nutanix (NTNX), pointing to slowing growth, limited momentum, and weaker visibility into revenue, a combination that has sharpened investor attention on the stock’s recent pullback.

The recent analyst downgrades arrived after a sharp swing in sentiment, with Nutanix’s share price at US$39.33 and a 30 day share price return of a 22.27% decline, adding to a 1 year total shareholder return loss of 42.81%. However, the 3 year and 5 year total shareholder returns of 34.51% and 17.12% respectively point to a longer term record that looks very different from the current pullback.

If this volatility has you comparing options in cloud and AI infrastructure, it could be a good moment to broaden your watchlist with high growth tech and AI stocks.

With Nutanix trading at US$39.33 and sitting at a 47% intrinsic discount alongside a 68% discount to analyst targets, the key question is whether this sell off is creating an opportunity or if the market is already pricing in future growth.

The most followed Nutanix narrative pegs fair value at about $67.85, well above the last close of $39.33, framing the recent slide in a very different light.

Ongoing enterprise digital transformation and demand for scalable solutions, as evidenced by large multi-year deals, major wins like Finanz Informatik, and increasing contributions from Global 2000 customers, provide a robust pipeline for future "land and expand" motions, improving both revenue visibility and opportunities for net new ARR expansion.

Curious what kind of revenue trajectory and margin profile sits behind that valuation gap prediction, and how long term profit expectations feed into the $60s fair value band?

Result: Fair Value of $67.85 (UNDERVALUED)

However, this hinges on Nutanix keeping growth on track. Slower workload shifts to its platform or tighter pricing competition could quickly challenge that $60s fair value view.

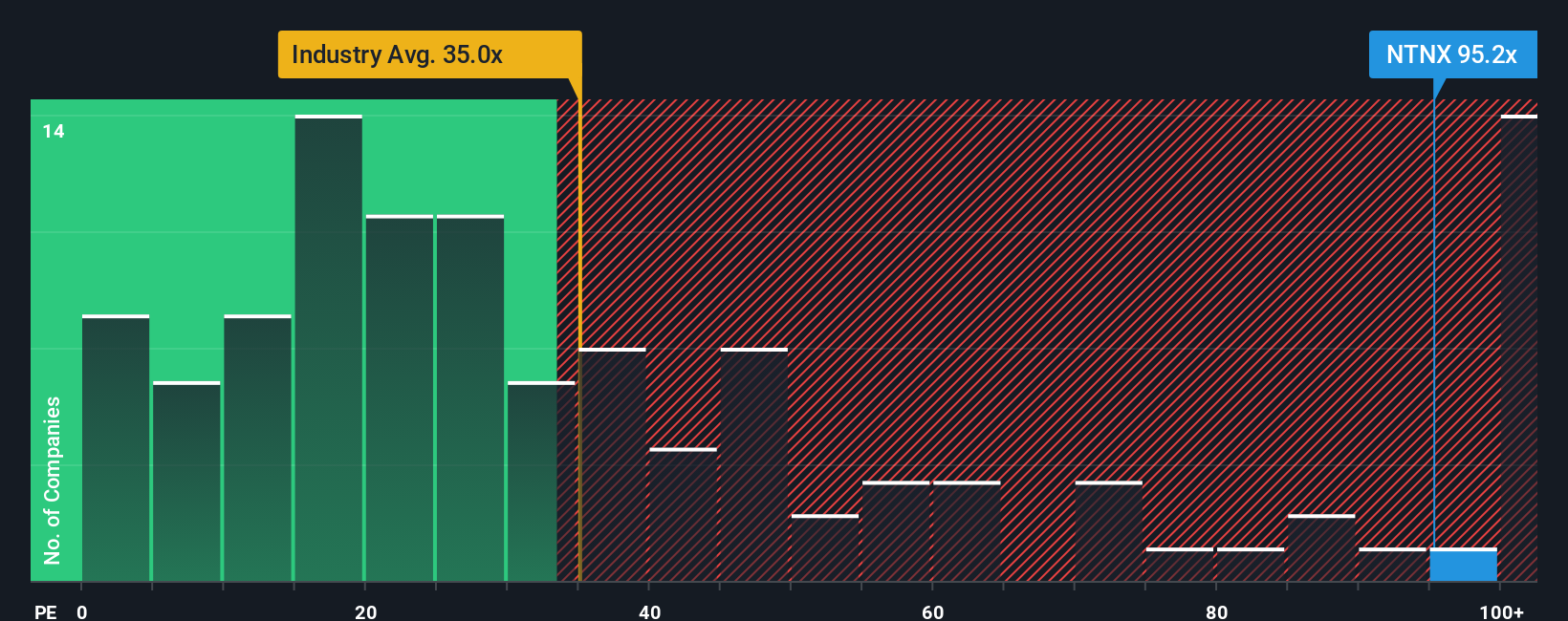

Those fair value estimates around $67.85 sit alongside a very different message from Nutanix’s current P/E of 48.2x. That is higher than the US Software industry at 28.2x and above its 42.3x fair ratio, so the multiple suggests less margin for error than the discount implies. Which signal matters more to you?

If you see the story differently or simply want to test your own assumptions against the same inputs, you can build a custom thesis in minutes with Do it your way.

A great starting point for your Nutanix research is our analysis highlighting 3 key rewards and 2 important warning signs that could impact your investment decision.

If Nutanix has sharpened your thinking, do not stop there. Use the Simply Wall St screener to quickly spot other opportunities that fit your style.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.