Please use a PC Browser to access Register-Tadawul

Get It

A Look At Robert Half (RHI) Valuation After Q4 Beat And Emerging Recovery Signals

Robert Half Inc. RHI | 23.18 | +1.87% |

Robert Half (RHI) has just reported Q4 2025 results, with revenue and earnings topping Wall Street forecasts even though both metrics were below the levels reported in the prior year.

The earnings beat and management’s talk of an inflection point have been followed by a sharp shift in sentiment, with a 30 day share price return of 26.59% and a 1 year total shareholder return of 43.27% decline. Short term momentum is picking up while longer term holders are still well under water.

If these Q4 moves have you rethinking where you find potential opportunities, it could be worth scanning fast growing stocks with high insider ownership as a starting point for fresh ideas.

So with Robert Half trading at US$34.61 after a 26% 30 day surge, a 34% estimated intrinsic discount and a price now above the average analyst target, are investors still getting a bargain, or is a recovery already priced in?

At a last close of $34.61 versus a most followed fair value estimate of about $30.67, the narrative suggests the recent rebound has moved ahead of that fair value anchor while still hinging on a recovery in earnings quality and capital returns.

The analysts have a consensus price target of $43.667 for Robert Half based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $55.0 and the most bearish reporting a price target of just $33.0.

Want to see what sits behind that spread in outcomes? Revenue rebuilding, margin repair, and a future earnings multiple all pull in different directions. The full narrative lays out how those moving parts combine into one fair value line.

Result: Fair Value of $30.67 (OVERVALUED)

However, persistent revenue declines and rising SG&A as a share of sales could keep margins under pressure and challenge the earnings recovery that underpins this fair value story.

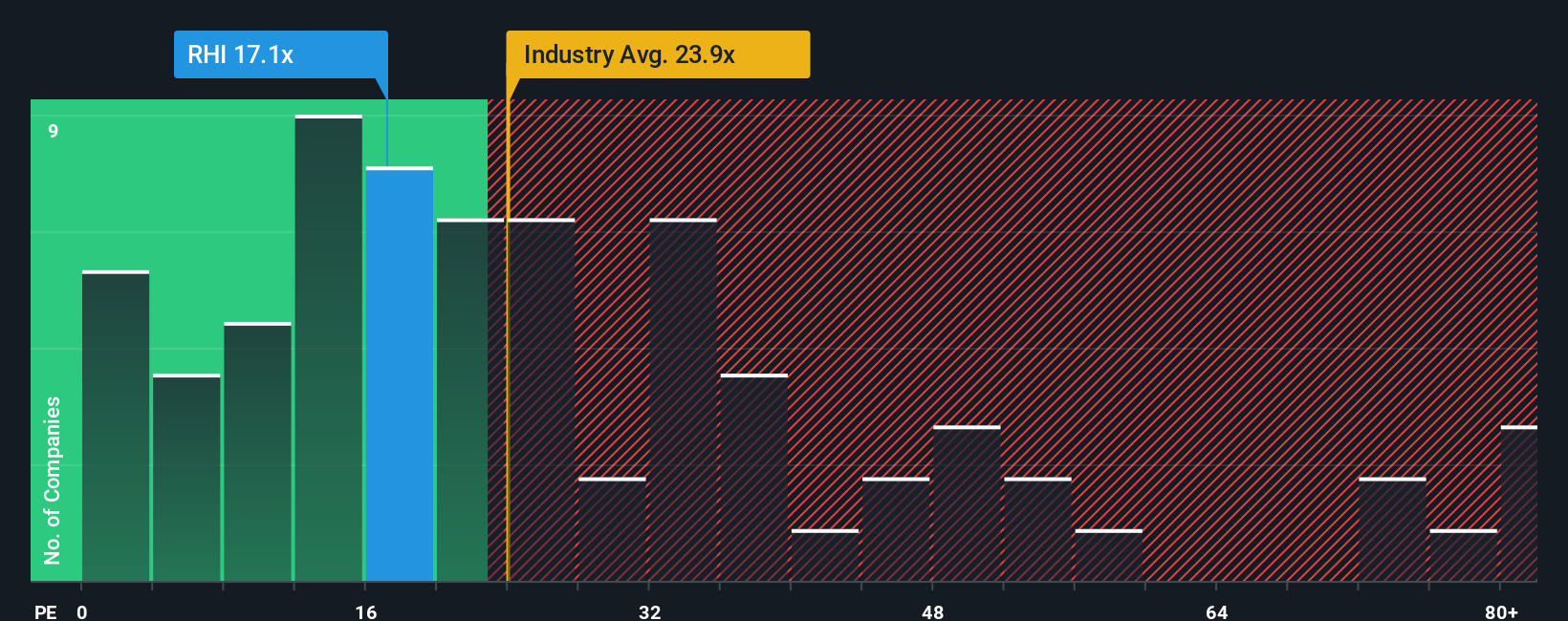

Our DCF-based fair value of $52.83 suggests Robert Half is undervalued at $34.61, even though the narrative fair value of $30.67 points to a 12.9% premium. On a P/E of 26x, it also screens as cheaper than its 29.4x fair ratio and below peers at 35.4x, but slightly richer than the 23.3x industry average. So, which reference point do you trust most when you think about risk versus upside?

If you see the numbers differently or prefer to test your own assumptions, you can build a complete Robert Half view in minutes using Do it your way.

A great starting point for your Robert Half research is our analysis highlighting 2 key rewards and 2 important warning signs that could impact your investment decision.

If Robert Half has you thinking differently about valuation and risk, do not stop here. Broaden your watchlist now so fresh opportunities do not pass you by.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.