Please use a PC Browser to access Register-Tadawul

Get It

A Look At Seagate Technology Holdings (STX) Valuation After Strong Q2 2026 Earnings And AI Data Center Momentum

Seagate Technology Holdings PLC STX | 383.71 | +2.60% |

Seagate Technology Holdings (STX) is back in focus after a standout fiscal Q2 2026, with higher revenue, wider margins and strong AI driven data center demand, followed by upbeat guidance and broad analyst support.

The latest move has come after a sharp run, with a 41.79% 30 day share price return and a 53.53% 90 day share price return. The 1 year total shareholder return is very large, and recent earnings, guidance, dividend affirmation and the new shelf registration filing are all being weighed into a story of strong recent momentum that investors are now reassessing around a US$407.69 share price.

If Seagate’s AI data center story has your attention, this could be a good moment to see what else is moving in high growth tech and AI stocks.

With Seagate now at an all time high, trading near analyst targets yet still screening at a sizeable intrinsic discount, you have to ask yourself: is there still a buying opportunity here, or is the market already pricing in future growth?

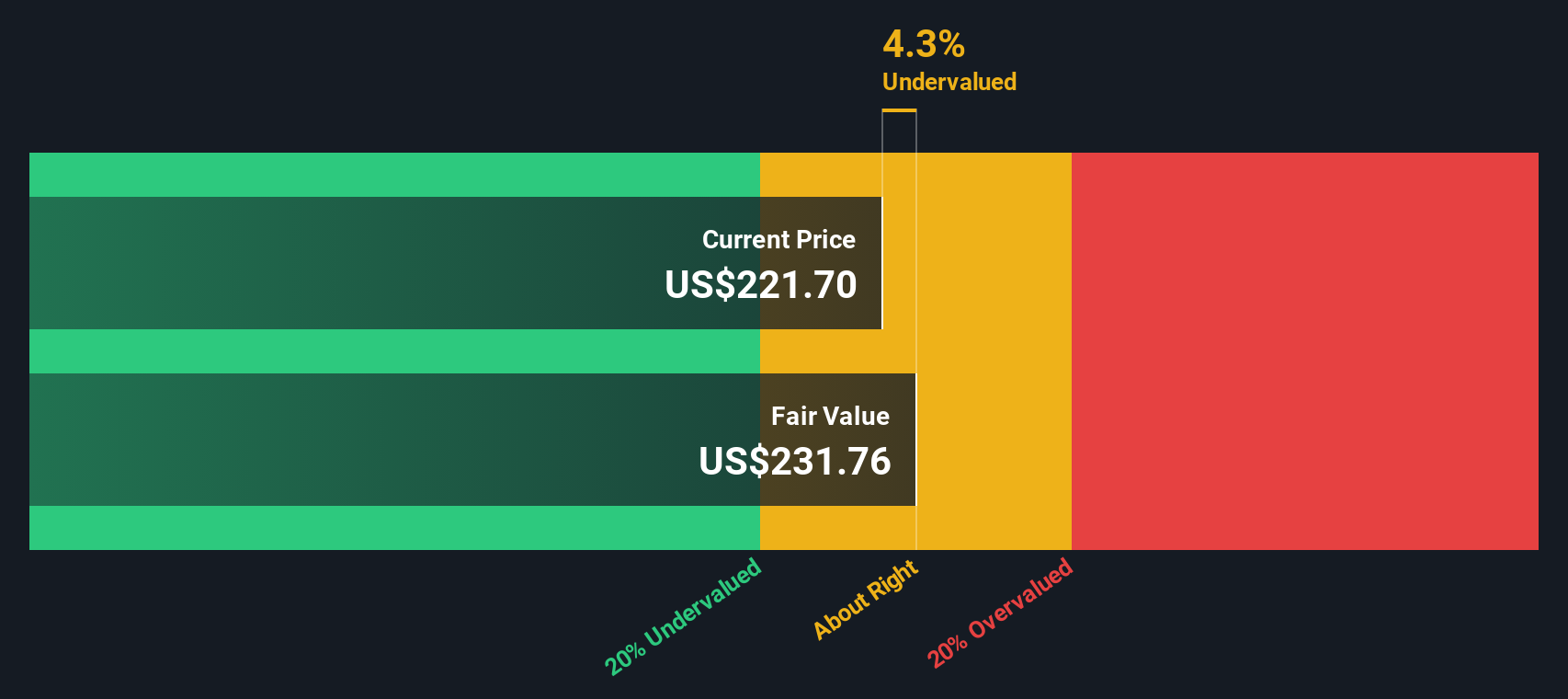

Simply Wall St's most followed narrative puts Seagate’s fair value at about $297 per share compared with the recent $407.69 close, so the story now hinges on how much faith you place in its long run earnings power and AI driven storage demand.

The Fair Value Estimate has risen slightly to approximately $297 per share from about $289, reflecting modestly stronger long term growth and earnings assumptions.

The Future P/E has risen moderately to roughly 23.4x from about 22.7x, indicating a somewhat higher valuation multiple applied to forward earnings expectations.

Curious what earnings trajectory and margin profile are needed to reach that fair value, even with a richer future P/E baked in? The full narrative lays out a detailed path for revenue, profitability and valuation multiples that you might want to weigh against your own expectations.

Result: Fair Value of $297 (OVERVALUED)

However, you still need to keep an eye on potential trade policy shifts and any prolonged supply or operational hiccups that could challenge the current AI driven HDD narrative.

Our DCF model points to a fair value around $625.48 per share, which is well above the current $407.69 price and implies Seagate is trading at a sizeable discount. That sits awkwardly against the narrative fair value of $297, so which set of assumptions feels closer to what you believe?

If you see the numbers differently or want to stress test your own assumptions against the models here, you can use the same data to build a custom view in just a few minutes: Do it your way.

A great starting point for your Seagate Technology Holdings research is our analysis highlighting 3 key rewards and 3 important warning signs that could impact your investment decision.

If you like what you have seen so far on Seagate, now is the moment to scan a wider field of opportunities before the next move passes you by.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.