Please use a PC Browser to access Register-Tadawul

Get It

A Look At Wynn Resorts (WYNN) Valuation After Mixed Recent Share Performance

Wynn Resorts, Limited WYNN | 103.33 104.00 | +1.03% +0.65% Pre |

Wynn Resorts (WYNN) has drawn investor attention after a period of mixed share performance, with the stock showing negative returns over the past week, month, and past 3 months, but a positive 1 year total return.

The company reports revenue of US$7.1b and net income of US$504.3m, with both revenue and net income growth reported on an annual basis. Its value score of 4 and current price of US$107.45 give investors a starting point for assessing how the market is currently pricing the business.

At around US$107.45, Wynn Resorts has seen its short term share price under pressure, with weaker recent share price returns contrasting with a stronger 1 year total shareholder return. This suggests earlier optimism has cooled in recent months as investors reassess growth and risk.

If Wynn has you thinking about opportunities in travel and leisure, it can be useful to compare it with other consumer focused names and broaden your search through fast growing stocks with high insider ownership.

So with Wynn Resorts trading around US$107.45 and sitting at a sizeable discount to some analyst targets and intrinsic estimates, is the recent pullback setting up an undervalued entry point or is the market already pricing in future growth?

Compared with the last close at $107.45, the most followed narrative points to a fair value near $144.89, framing Wynn Resorts as trading at a sizeable discount.

The imminent launch of Wynn Al Marjan Island, with first-mover advantage and limited near-term competition in a potentially multi-billion-dollar new market, is a major forward catalyst that is currently underappreciated by investors and could drive a meaningful step-change in both consolidated revenue and EBITDAR.

Want to see what kind of revenue, margin uplift, and future earnings multiple are baked into that valuation gap? The full narrative lays out the numbers and the logic behind them.

At the core of this fair value is a glide path for Wynn Resorts that assumes measured revenue expansion, improving profitability, and a future P/E that remains above the wider US hospitality group. It also builds in a specific discount rate to bring those projected cash flows back to today, which is why the gap between $107.45 and about $144.89 stands out for followers of this narrative.

Result: Fair Value of $144.89 (UNDERVALUED)

However, the story can change quickly if Macau faces fresh regulatory pressure or if rising operating and project costs squeeze the earnings power that underpins that valuation gap.

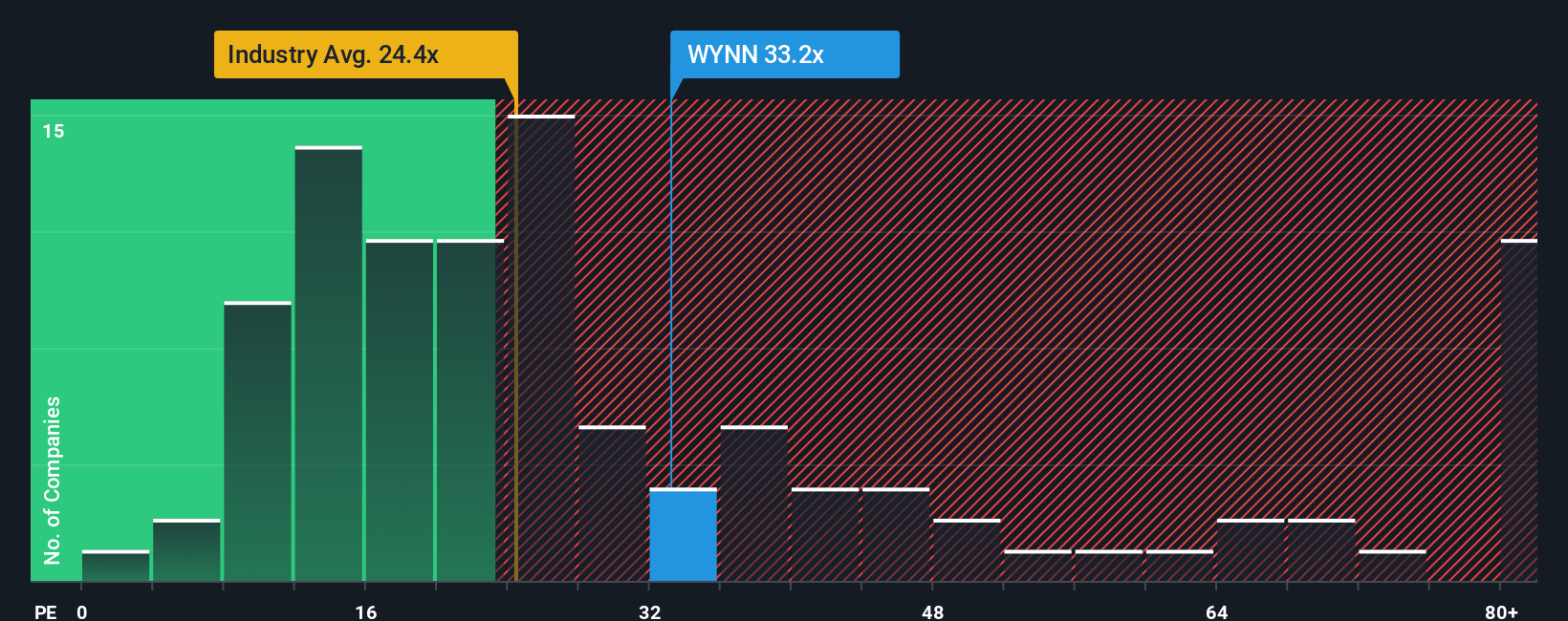

Analysts and the narrative both point to upside for Wynn Resorts from its current price of $107.45, but the earnings multiple sends a different signal. The stock trades on a P/E of 21.9x, slightly higher than the US Hospitality average of 21.2x and above its own fair ratio of 21.2x, which suggests less room for error if earnings fall short.

With peers on 55.6x, you could argue Wynn looks restrained or that the peer group is simply priced for a lot more growth. Which reference point do you lean on when you weigh risk against potential reward?

If you see the numbers differently or simply prefer to stress test the assumptions yourself, you can spin up a fresh view in just a few minutes with Do it your way.

A great starting point for your Wynn Resorts research is our analysis highlighting 3 key rewards and 3 important warning signs that could impact your investment decision.

If Wynn has sparked your interest, do not stop here. Broaden your watchlist with fresh ideas that fit different themes and potential return profiles.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.