Please use a PC Browser to access Register-Tadawul

Get It

AbbVie (ABBV) Boosts Dividend After Net Income Slips—What Does This Reveal About Its Capital Priorities?

AbbVie, Inc. ABBV | 208.34 208.30 | -5.20% -0.02% Post |

These 13 companies survived and thrived after COVID and have the right ingredients to survive Trump's tariffs. Discover why before your portfolio feels the trade war pinch.

To be a shareholder in AbbVie right now, you’d need to be confident in the company’s ability to drive growth through its immunology and neuroscience franchises, balancing expansion with disciplined capital returns even as earnings face temporary headwinds. The recent Q3 news of higher sales but a sharp fall in net income, triggered by a non-cash impairment, does not materially change the immediate catalyst: maintaining strong revenue growth from new therapies while offsetting Humira’s ongoing decline. The most pressing risk remains heightened pricing pressure and patent expirations for key products, which could impact future profitability.

The announced increase in AbbVie’s quarterly dividend, up 5.5% to US$1.73 per share starting in February 2026, is particularly relevant in this context. While the boost reinforces the commitment to rewarding shareholders, it also draws attention to the challenge of sustaining robust cash flows as patent cliffs and competitive pressures loom. For investors, it underscores how closely cash return policies are intertwined with the company’s long-term growth trajectory and risk management, especially as pipeline and portfolio diversification become more critical.

Yet, in contrast to the rising dividend, there’s emerging pressure from pricing reforms and regulatory shifts that all investors should be aware of...

AbbVie's narrative projects $73.0 billion revenue and $20.8 billion earnings by 2028. This requires 7.7% yearly revenue growth and a $17.1 billion increase in earnings from $3.7 billion today.

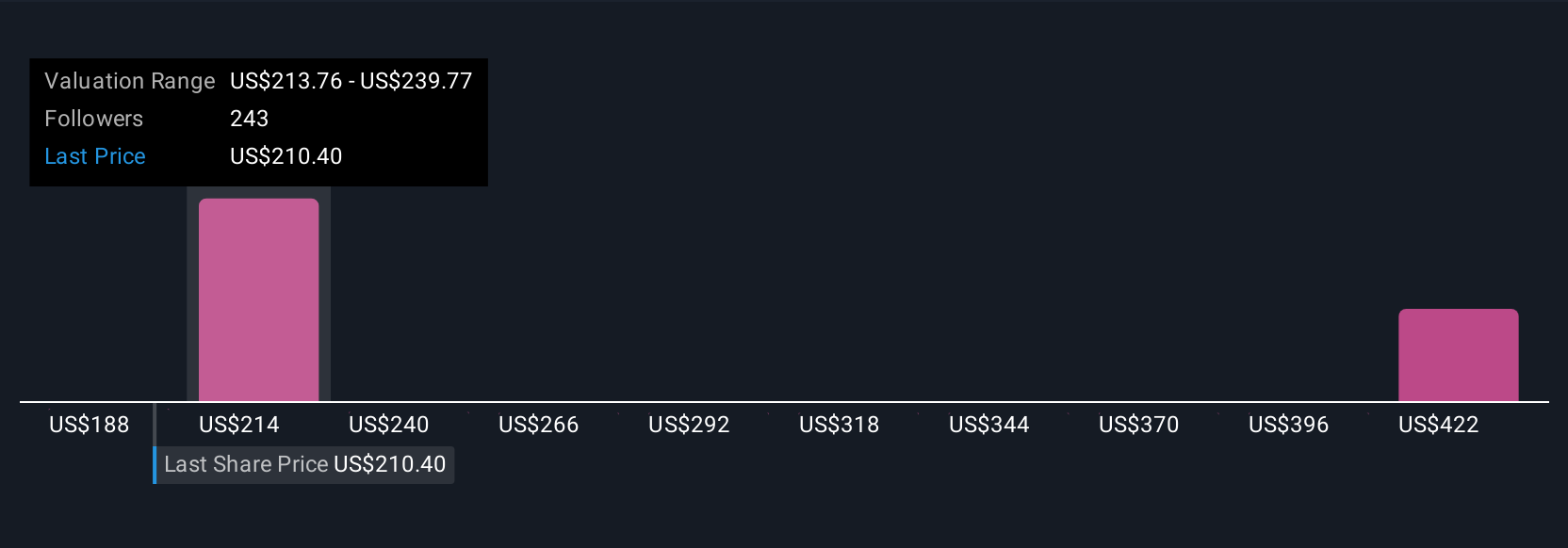

Uncover how AbbVie's forecasts yield a $241.29 fair value, a 4% upside to its current price.

Fair value estimates from four Simply Wall St Community members range from US$232 to US$435, reflecting wide views on future growth and risk. Your outlook on AbbVie may also hinge on competition and potential revenue erosion as major product exclusivities expire, suggesting it is valuable to compare different perspectives before making up your mind.

Explore 4 other fair value estimates on AbbVie - why the stock might be worth as much as 87% more than the current price!

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

Our top stock finds are flying under the radar-for now. Get in early:

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.