Please use a PC Browser to access Register-Tadawul

Get It

Agilent Technologies (A) Valuation Check After New Automation And AI Lab Tools Showcase

Agilent Technologies, Inc. A | 111.63 | 0.00% |

Agilent Technologies (A) is putting automation, imaging, and AI tools front and center at the SLAS2026 conference in Boston, previewing new platforms aimed at workflow efficiency and regulatory compliance in pharma and biotech labs.

Despite the automation and AI product momentum, Agilent’s recent trading has been weaker, with a 30 day share price return of a 12.17% decline and a 1 year total shareholder return of an 11.48% decline, pointing to fading momentum as investors reassess risks and growth expectations.

If this focus on lab automation has your attention, it could be worth widening the lens to other AI infrastructure players by checking out our 33 AI infrastructure stocks as a starting list of potential ideas.

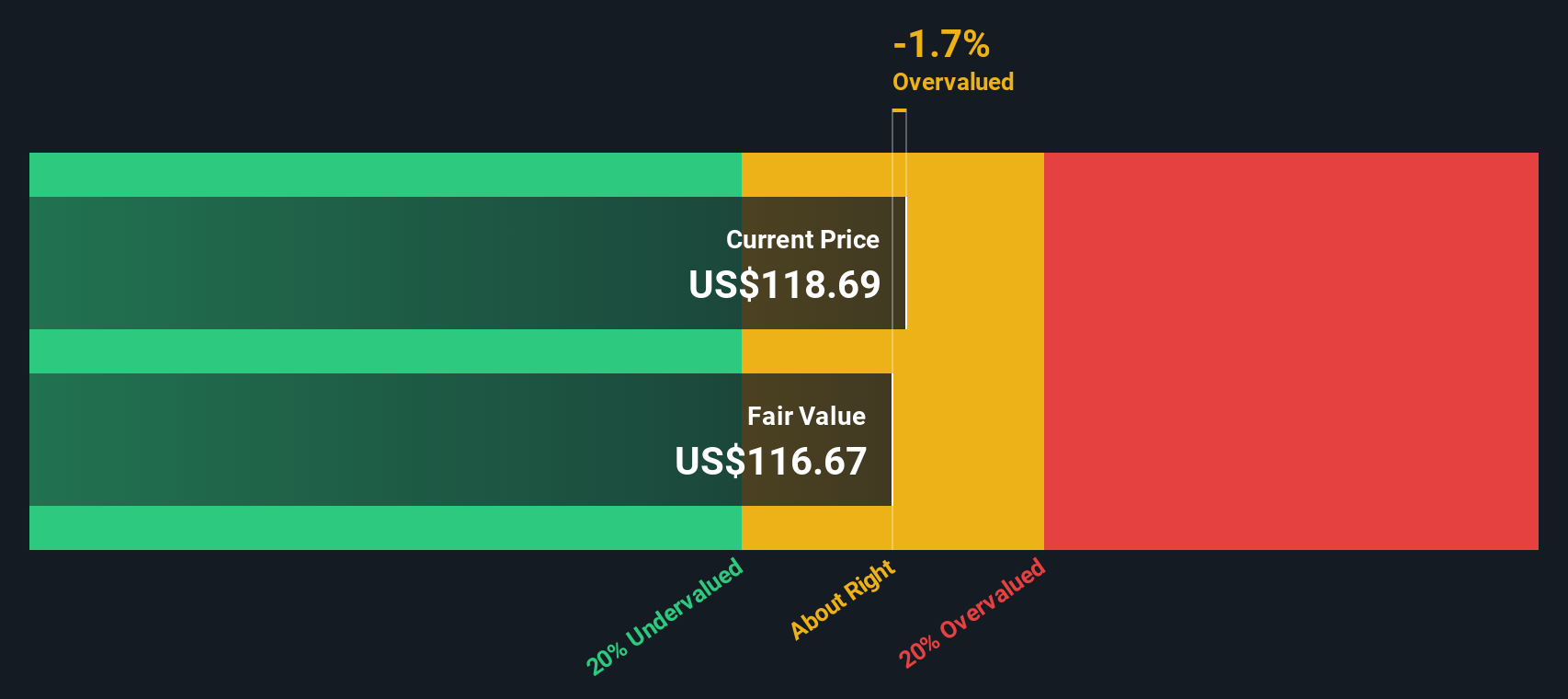

With Agilent’s shares down over the past year despite solid reported revenue and net income growth, the key question now is whether recent weakness has left the stock undervalued or if the market is already assuming significant future growth.

Agilent Technologies most followed valuation narrative sets a fair value of $169.67 per share, above the last close of $129.64, and anchors on measured, recurring growth in life sciences and diagnostics.

Strategic investments in higher margin recurring revenue streams including consumables, software, services, and digital platforms are gaining traction, with CrossLab and services delivering consistent mid single digit growth and high customer satisfaction, indicating further margin expansion and greater earnings stability in future periods. Agilent's Ignite enterprise operating model is already delivering material cost savings (double digit reductions in key categories) and operational efficiencies, while ongoing global supply chain reorganization and targeted pricing actions are expected to fully offset tariff related margin headwinds by FY2026, underpinning future operating margin improvements.

Want to see what kind of revenue profile and margin lift need to line up to support that higher valuation anchor? The narrative leans on recurring sales, rising profitability and a future earnings multiple that assumes investor confidence holds up. Curious which specific growth path and profitability mix are doing the heavy lifting in that fair value model? The full write up lays those assumptions out in detail.

Result: Fair Value of $169.67 (UNDERVALUED)

However, this upside story still hinges on tariffs and supply chain complexity being contained, and on replacement driven instrument demand not cooling faster than analysts expect.

There is a twist when you switch lenses. While the narrative fair value sits at $169.67 per share and frames Agilent as 23.6% undervalued, our DCF model points to a value of $115.94, which would make the current $129.64 price look expensive instead. Which story do you find more convincing?

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Agilent Technologies for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 55 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

If you are not sold on any single take or prefer to stress test the numbers yourself, you can shape a custom view in just a few minutes, starting with Do it your way.

A good starting point is our analysis highlighting 4 key rewards investors are optimistic about regarding Agilent Technologies.

If Agilent has sparked new questions about your portfolio, do not stop here. Use the tools available to keep broadening your opportunity set with discipline.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.