Please use a PC Browser to access Register-Tadawul

Get It

Assessing Comfort Systems USA (FIX) Valuation After Revenue Beat And Growing AI Infrastructure Demand

Comfort Systems USA, Inc. FIX | 1365.34 | -0.61% |

Recent commentary from Jim Cramer and Voya Investment Management has put Comfort Systems USA (FIX) in focus after the company reported quarterly revenue above expectations, tied to demand from data centers, AI infrastructure, and recurring service work.

At a share price of $1,142.10, Comfort Systems USA has paired a 13.8% 30 day share price return with a very large 5 year total shareholder return. This hints that enthusiasm around data center and AI infrastructure work is feeding into expectations rather than fading.

If this kind of AI infrastructure story has your attention, it could be a good moment to see what else is moving in related areas through high growth tech and AI stocks.

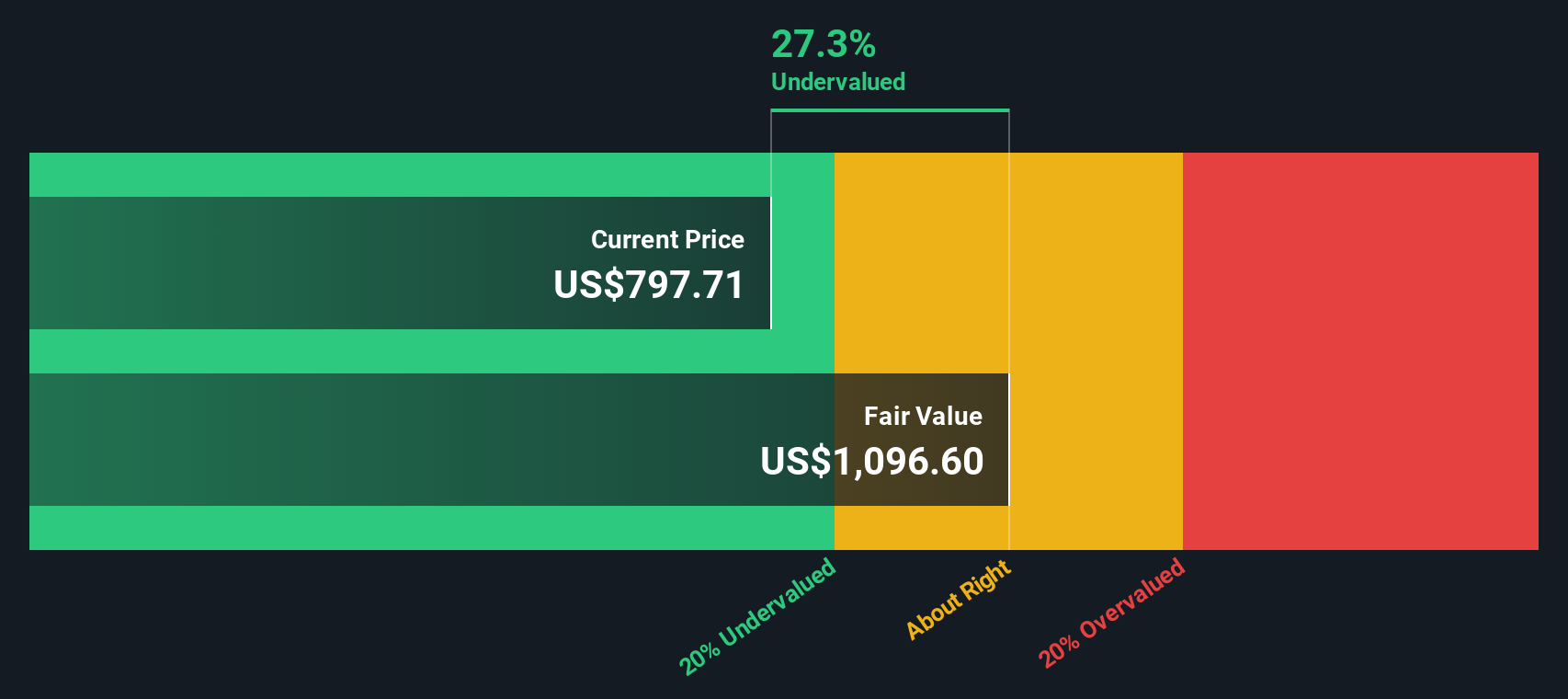

With the stock at $1,142.10 after a strong 1 year and 5 year run, the key question now is whether Comfort Systems USA is still trading below its intrinsic value or if the market is already pricing in expectations for the company’s future.

The most followed narrative places Comfort Systems USA’s fair value at $1,150, which sits slightly above the last close of $1,142.10, and leans on long run cash flow potential rather than short term momentum.

Ongoing modular construction expansion, with modular revenue now 18% of total and more capacity coming online, is capitalizing on industry movement toward integrated and efficient building solutions supporting higher revenue growth and gross margin expansion.

Want to see what sits behind that $1,150 fair value call? The narrative leans heavily on sustained revenue expansion and thicker margins, all filtered through a single discount rate and a future earnings profile that looks very different to today.

Result: Fair Value of $1,150 (UNDERVALUED)

However, this hinges on tech heavy project demand staying firm, and on Comfort Systems USA managing labor and cost pressures that could squeeze margins and backlog quality.

While our DCF model suggests Comfort Systems USA is undervalued, the current P/E of 48x is higher than both the US Construction industry at 34.8x and the company’s own fair ratio of 45.4x. This points to some valuation risk if sentiment cools.

If you see the numbers differently, or just want to stress test these assumptions with your own inputs, you can create a custom Comfort Systems USA view in a few minutes using Do it your way.

A great starting point for your Comfort Systems USA research is our analysis highlighting 3 key rewards and 1 important warning sign that could impact your investment decision.

If Comfort Systems USA has sharpened your thinking, do not stop here. Use the Simply Wall St Screener to surface more focused, data driven ideas in minutes.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.