Assessing Liberty Energy (LBRT) Valuation After A Strong Multi‑Period Share Price Run

Liberty Energy, Inc. Class A LBRT | 28.44 28.44 | +2.78% 0.00% Post |

Why Liberty Energy Is On Investors’ Radar

Liberty Energy (LBRT) has caught investor attention after a strong share price move, with returns over the past month and past 3 months outpacing its 1 year and multi year performance.

The recent move to a US$26.09 share price sits on top of a 30 day share price return of 38.19% and a 90 day share price return of 53.38%. Meanwhile, the 1 year total shareholder return of 48.34% and 5 year total shareholder return of 124.50% point to momentum that has been building over time.

If this kind of move in Liberty Energy has your attention, it could be a good moment to broaden your search and check out aerospace and defense stocks as another source of ideas.

With the stock at US$26.09 after strong recent returns and an intrinsic value estimate suggesting a discount, the key question is whether Liberty Energy is still mispriced or whether the market is already factoring in future growth.

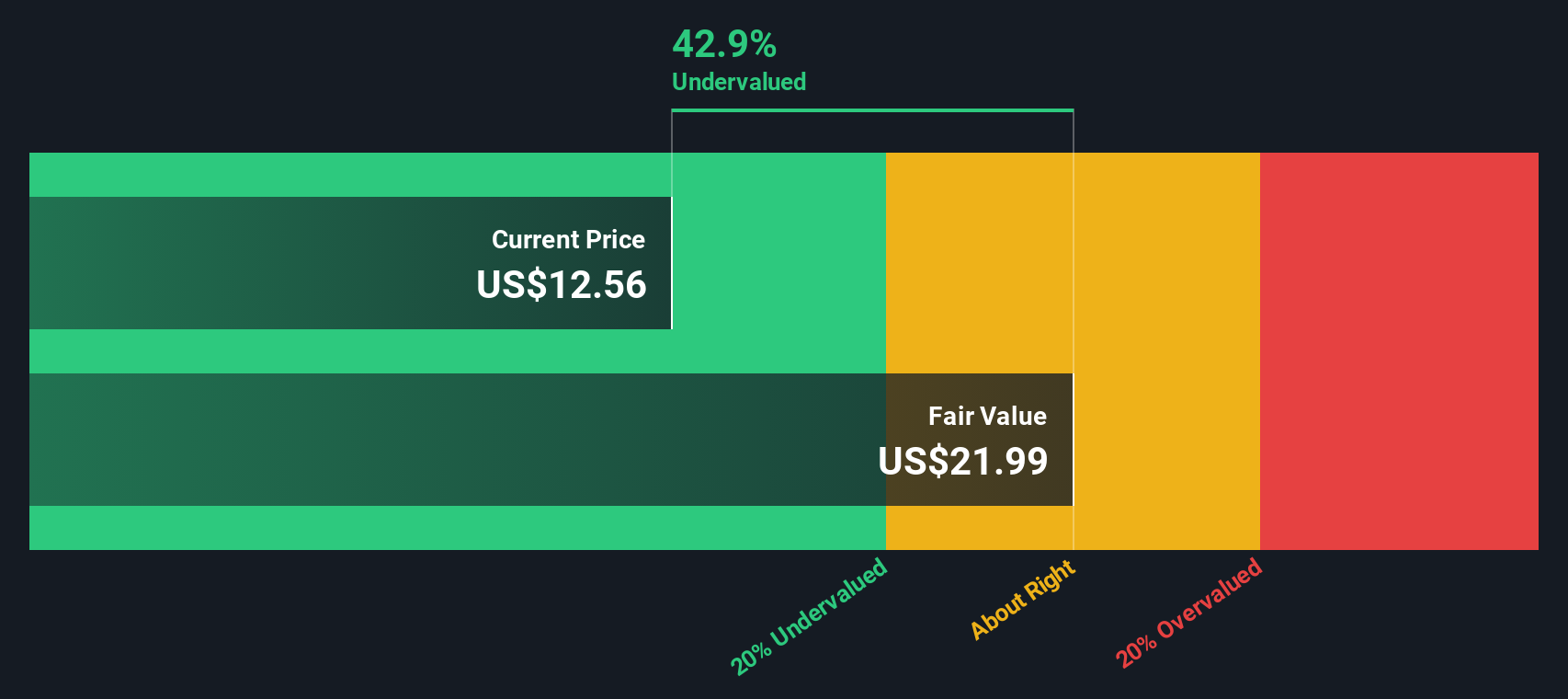

Most Popular Narrative: 29.1% Overvalued

Liberty Energy’s most followed narrative puts fair value at about $20.21, which sits well below the recent $26.09 share price, setting up a clear tension to unpack.

Liberty's leadership in next-generation technology, including its digiPrime/digiFleet natural gas-powered frac solutions and modular, low-emission power generation, is enabling market share gains, operational efficiencies, longer asset life, and stronger pricing with top-tier customers, supporting improved margins and higher free cash flow.

Curious how that operational story leads to a lower fair value than today’s price? The narrative leans on measured revenue growth, slimmer future margins, and a reset earnings multiple. The full set of numbers ties those threads together in a way that may surprise you.

Result: Fair Value of $20.21 (OVERVALUED)

However, there are still clear pressure points, including softer completions activity and service pricing headwinds in 2025 that could weigh on revenue and margins.

Another View: Cash Flows Point The Other Way

The most popular fair value narrative pins Liberty Energy at about $20.21, which sits below the current $26.09 share price. Our DCF model provides an estimated future cash flow value of $144.36 per share.

So which signal do you treat as the anchor for your own work: the earnings based narrative, or the cash flow view?

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Liberty Energy for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 872 undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own Liberty Energy Narrative

If you read this and feel differently, or prefer to weigh the numbers yourself, you can build a fresh view in just a few minutes with Do it your way.

A great starting point for your Liberty Energy research is our analysis highlighting 2 key rewards and 3 important warning signs that could impact your investment decision.

Looking For More Investment Ideas?

If Liberty Energy has sparked your interest, do not stop here. Broaden your watchlist now so you are not relying on a single story or sector.

- Spot potential value by checking out these 872 undervalued stocks based on cash flows that align with cash flow strength and pricing that may not fully reflect it yet.

- Ride long term technology themes by scanning these 24 AI penny stocks at the intersection of artificial intelligence and real business models.

- Add income ideas by reviewing these 13 dividend stocks with yields > 3% that offer yields above 3% alongside underlying business fundamentals.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.