Please use a PC Browser to access Register-Tadawul

Get It

Assessing Nicolet Bankshares (NIC) Valuation After Strong Earnings And Higher Investor Optimism

Nicolet Bankshares, Inc. NIC | 161.37 | +1.70% |

Nicolet Bankshares (NIC) is back in focus after reporting fourth quarter and full year 2025 results, showing higher net interest income and net income, alongside a fresh shareholder approval to increase authorized shares.

After these earnings and the shareholder approval to increase authorized shares, Nicolet Bankshares’ share price has climbed to US$145.98, with a 21.16% year to date share price return and a 31.47% total shareholder return over the last year. The three and five year total shareholder returns of 99.38% and 110.85% suggest momentum has been building over a longer horizon.

If the combination of earnings growth, dividends, and capital actions has your attention, it could be a good moment to broaden your search with fast growing stocks with high insider ownership.

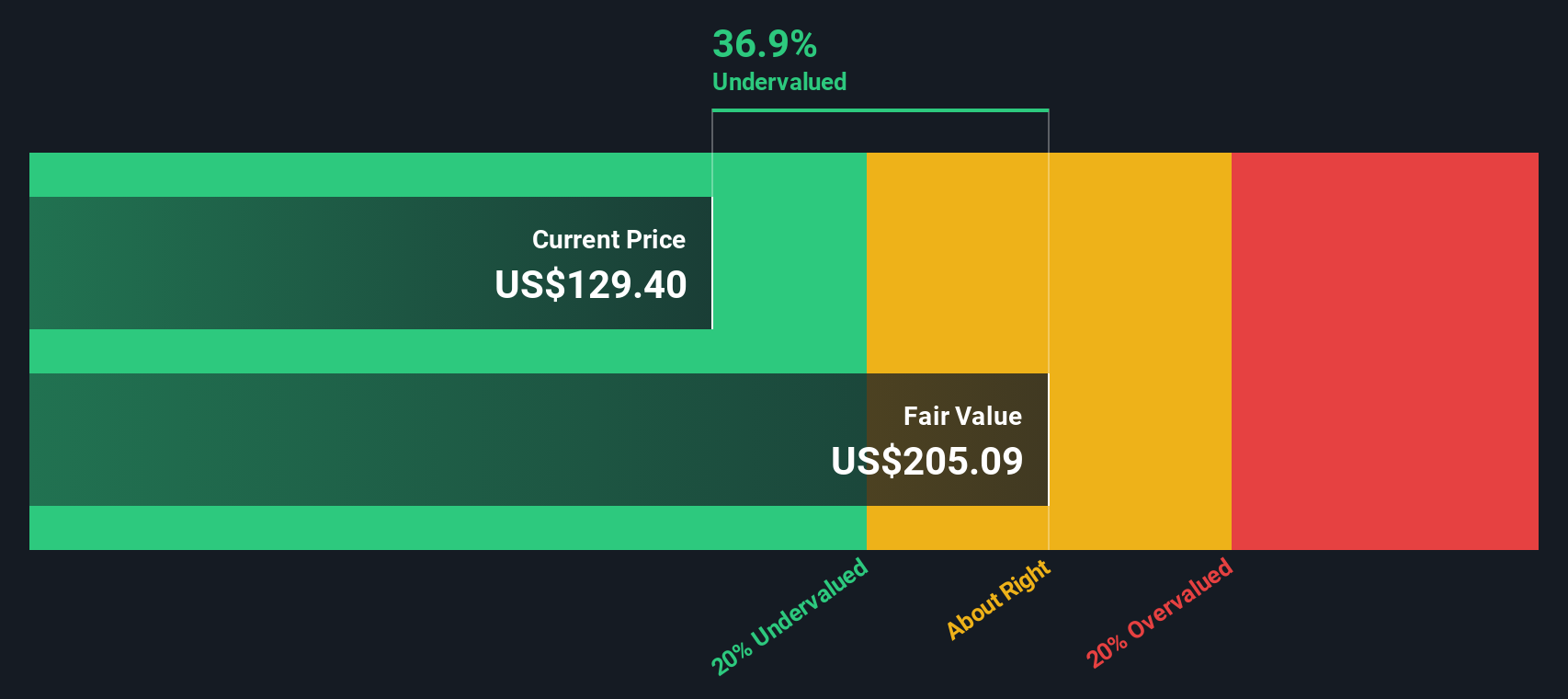

With earnings, dividends and capital moves all in play, the key question now is whether Nicolet Bankshares at US$145.98 and a value score of 4 still trades at a discount, or if the market is already pricing in future growth.

On a P/E of 14.2x at a share price of $145.98, Nicolet Bankshares screens as more expensive than the US Banks industry on this measure, even though other indicators suggest the market may still be assigning it a discount to its estimated fair value.

P/E compares the current share price to earnings per share, so it effectively shows how many dollars investors are paying for each dollar of earnings. For a bank like Nicolet Bankshares, this ratio often reflects what the market thinks about the durability of earnings, growth potential and risk profile.

Here, the picture is mixed. The company is flagged as expensive relative to the broader US Banks industry average P/E of 11.8x. However, it is described as good value against a peer average P/E of 18.4x and an estimated fair P/E of 17.4x. That suggests the current multiple sits between a sector level where investors pay less for bank earnings and a peer group level where the market appears willing to pay more, with the fair ratio implying room for the valuation to move closer to that higher level if conditions support it.

Result: Price-to-Earnings of 14.2x (UNDERVALUED)

However, you still have to weigh risks, such as any shift in credit quality or a weaker return profile, that could challenge the current P/E narrative.

While the 14.2x P/E suggests Nicolet Bankshares is relatively expensive against the US Banks industry but cheaper than peers, our DCF model paints a different picture. With the share price at $145.98 versus an estimated future cash flow value of $192.19, the stock screens as undervalued on this method. This raises the question of which signal may be more informative.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Nicolet Bankshares for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 874 undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

If you see the story differently or prefer to work through the numbers yourself, you can build a fresh view in a few minutes by starting with Do it your way.

A good starting point is our analysis highlighting 3 key rewards investors are optimistic about regarding Nicolet Bankshares.

If Nicolet Bankshares has sharpened your focus, do not stop here, you could miss other opportunities that fit your style just as well.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.