Please use a PC Browser to access Register-Tadawul

Get It

Assessing Take-Two Interactive Software (TTWO) Valuation After Recent Share Price Pullback

Take-Two Interactive Software, Inc. TTWO | 244.34 244.34 | -0.47% 0.00% Pre |

Take-Two Interactive Software (TTWO) shares have nudged lower over the past month, with investors parsing the recent performance. While no major event has rocked the headlines, some are taking a closer look at how the stock’s valuation compares.

After jumping earlier this year, Take-Two’s momentum has faded a bit, with the share price pulling back over the past month. Even so, investors who stuck with the company have enjoyed a 32% total shareholder return over the past year and an impressive 138% total return over three years. This suggests long-term potential remains strong despite short-term volatility.

If you’re interested in finding other compelling opportunities in the sector, check out fast growing stocks with high insider ownership.

With Take-Two’s recent pullback and robust long-term returns, the key question now is whether the current share price undervalues the company’s future prospects or if the market has already factored in all of its potential growth.

Take-Two Interactive Software’s most followed valuation narrative puts fair value at $274.49, notably higher than the recent close of $235.03. This implies meaningful room for upside if projections play out. The calculations reflect both optimism for future growth and specific expectations for margin and revenue expansion.

Strategic investments in technology, AI, and content pipeline efficiency, along with a strong release slate featuring multiple high-profile launches (including Borderlands 4, NBA 2K26, and Mafia: The Old Country), support management's outlook for record net bookings and enhanced profitability in the coming years.

Curious what kind of game-changers support this valuation? Dive in for the growth targets, bold margin projections, and the blockbuster launch pipeline that analysts are banking on. There’s one profit forecast in particular raising eyebrows. See how it could set a new standard for the industry.

Result: Fair Value of $274.49 (UNDERVALUED)

However, uncertainty remains, as heavy dependence on blockbuster franchises and rising development costs could hinder Take-Two’s ability to meet bullish growth targets.

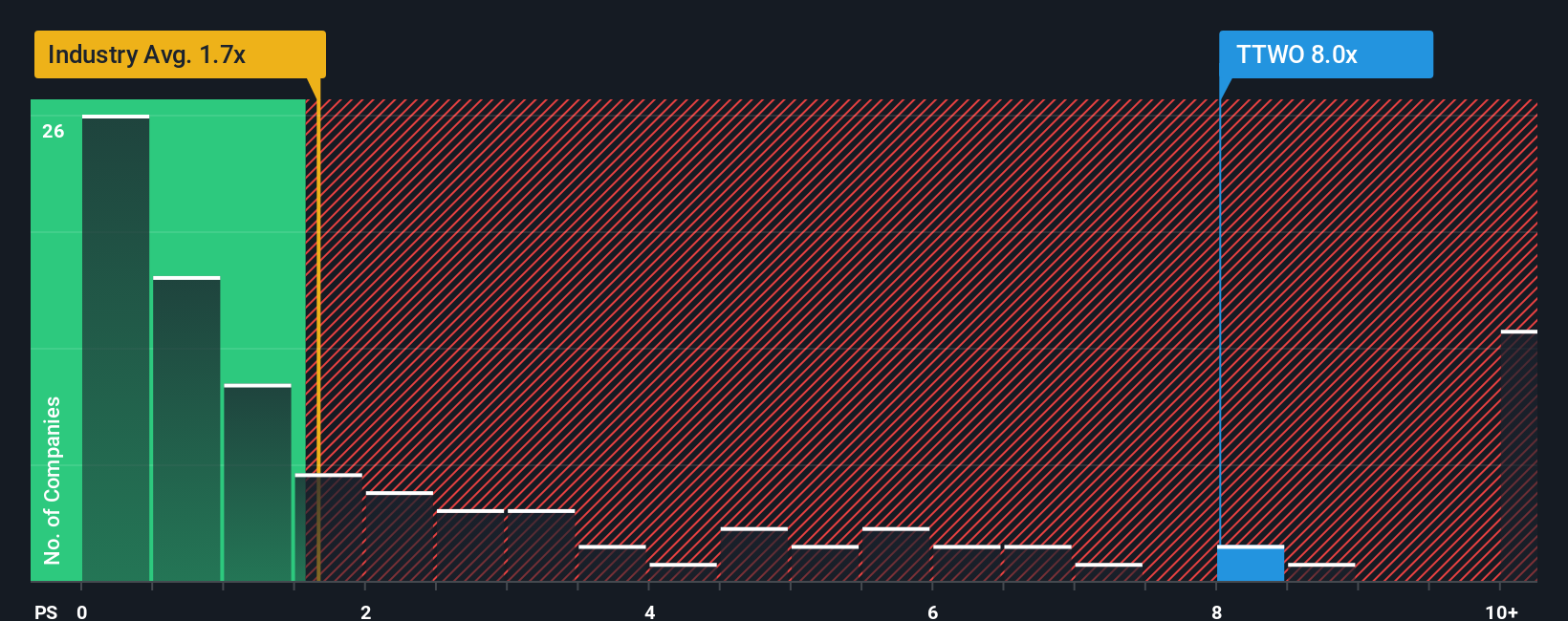

While the consensus view sees Take-Two as undervalued based on analyst forecasts, the market’s current price-to-sales ratio tells a different story. Take-Two trades at about 7x sales, which is much steeper than the peer average of 6.3x, the industry’s 1.5x, and even well above its fair ratio of 4.9x.

This gap suggests investors are paying a premium for future potential, not proven profits, raising questions about valuation risk. Will the company’s results catch up to this higher bar, or could expectations reset?

Feel free to dive into the numbers and shape your own perspective. Building a custom narrative for Take-Two is quick and straightforward. Do it your way

A good starting point is our analysis highlighting 1 key reward investors are optimistic about regarding Take-Two Interactive Software.

Smart investors never settle for just one play. Unlock fresh strategies by acting now on opportunities that others might overlook. The next breakout stock could be a click away.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.