Please use a PC Browser to access Register-Tadawul

Get It

Assessing Ubiquiti (UI) Valuation After Debt Repayment And Renewed Shareholder Returns

UBIQUITI INC UI | 774.25 774.25 | -3.02% 0.00% Pre |

Ubiquiti (UI) is back in focus after a strong 2025, when the company repaid substantial debt, reinstated its share repurchase program, and lifted its dividend. These moves have sharpened attention on shareholder outcomes.

The recent 3.4% 1 month share price return to US$580.38 comes after a much weaker 90 day share price return of a 23.1% decline. However, longer term total shareholder returns of 61.1% over 1 year and 146.8% over 5 years suggest the recent momentum looks more like a pause than a reset in how the market views Ubiquiti’s growth prospects and risk profile.

If Ubiquiti’s move has caught your attention, it can be helpful to compare it with other networking and connectivity names in tech, including high growth tech and AI stocks.

With Ubiquiti trading near its US$587.50 analyst target and recent returns already strong, the key question now is simple: is the current price still attractive, or is the market already pricing in the next phase of growth?

At a last close of US$580.38, Ubiquiti trades on a P/E of 44.3x, which screens as expensive relative to both its peers and an estimated fair level.

The P/E ratio compares the current share price with earnings per share, so a higher figure usually means the market is putting a richer price on each dollar of profit. For a networking hardware and software name like Ubiquiti, investors often look at P/E to gauge how much future earnings growth they are implicitly paying for.

Here, several checks point in the same direction. Ubiquiti is described as expensive versus its fair P/E of 37x, and also expensive compared with the peer average of 31.9x. That suggests the current price builds in a stronger earnings outlook than what those benchmarks imply, and the gap to the fair ratio highlights a level the market could move toward if sentiment or growth expectations cool.

Against the broader US Communications industry, Ubiquiti again sits at the high end, with its 44.3x P/E above the sector average of 37.6x. That is a clear premium, and it reinforces the idea that investors are already paying up compared with similar companies on earnings terms.

Result: Price-to-Earnings of 44.3x (OVERVALUED)

However, the rich 44.3x P/E and Ubiquiti’s tight focus on networking gear and software mean any slowdown in demand or earnings could quickly hit sentiment.

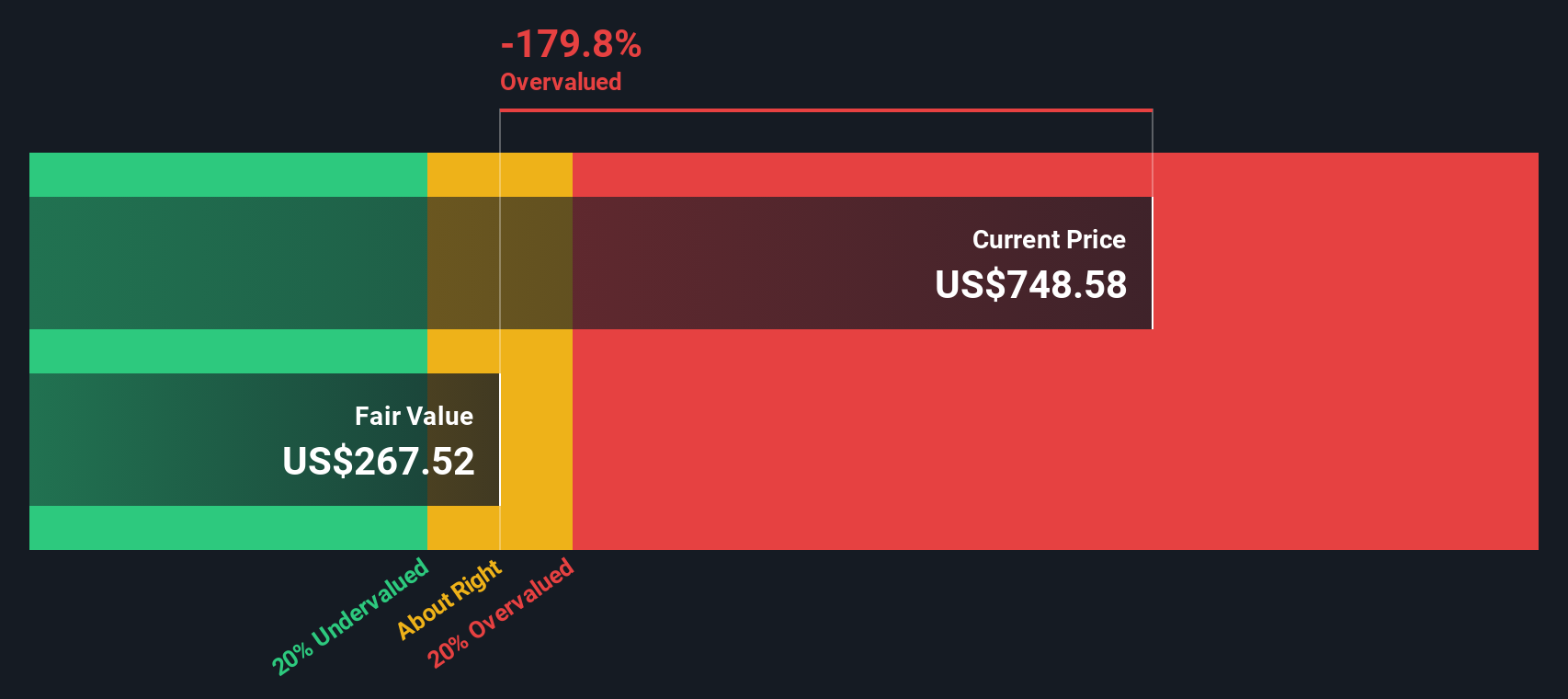

While the 44.3x P/E suggests a rich price, the SWS DCF model points in the same direction rather than softening that picture. At US$580.38, Ubiquiti trades well above our DCF fair value estimate of US$141.88, which frames the shares as overvalued on this cash flow view.

In practical terms, that gap means you are paying a price that our DCF model does not support based on its cash flow assumptions. The question is whether you believe Ubiquiti’s future cash generation can outpace those inputs enough to close that gap, or if the current enthusiasm is running ahead of fundamentals.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Ubiquiti for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 880 undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

If you look at the numbers and reach a different conclusion, or simply prefer to rely on your own work, you can build a complete view in just a few minutes by starting with Do it your way.

A great starting point for your Ubiquiti research is our analysis highlighting 2 key rewards and 1 important warning sign that could impact your investment decision.

If Ubiquiti is on your radar, it is worth broadening your watchlist with a few focused stock ideas that could suit very different approaches.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.