Please use a PC Browser to access Register-Tadawul

Get It

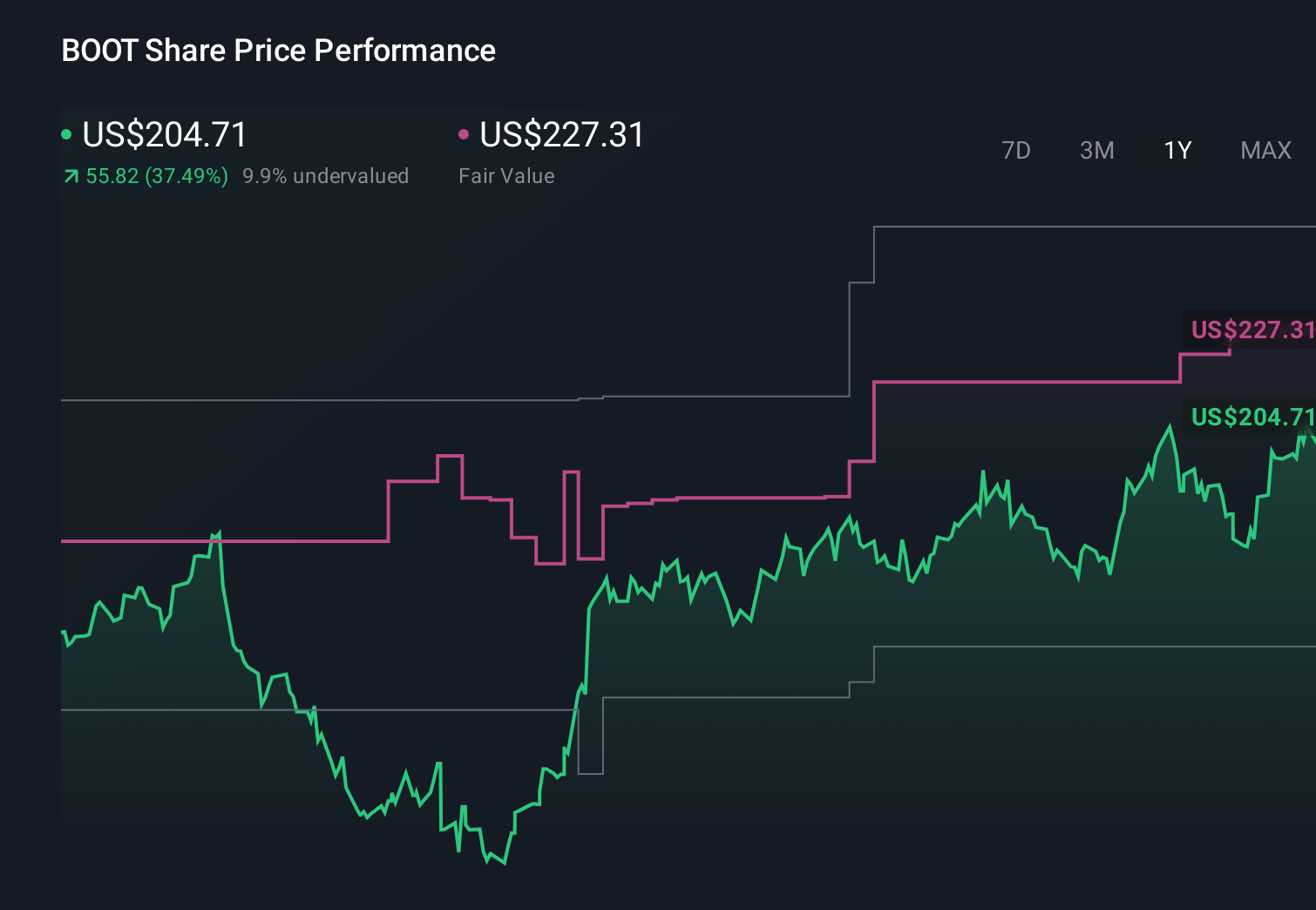

Boot Barn (BOOT) Is Up 10.9% After Raising FY26 Guidance and Accelerating Store Expansion Plans

Boot Barn Holdings, Inc. BOOT | 199.76 | +1.46% |

Capitalize on the AI infrastructure supercycle with our selection of the 33 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

To own Boot Barn today, you have to believe its Western and workwear niche can keep supporting a larger store base, while e-commerce and exclusive brands do more of the heavy lifting on profitability. The latest quarter and upgraded full-year guidance reinforce that story in the near term, with management leaning into 70 new store openings and calling out same-store sales and margin focus as key levers. Short-term, the main catalysts now sit around execution on that expansion plan, maintaining gross margin discipline as volume scales, and how effectively the completed US$37.44 million buyback and any future repurchases support earnings per share. On the risk side, the strong share price run and a price-to-earnings multiple above peers leave less room for disappointment if sales or margins soften.

Boot Barn Holdings' shares are on the way up, but could they be overextended? Uncover how much higher they are than fair value.

Five fair value views from the Simply Wall St Community span roughly US$27.81 to US$278.15 per share, underlining how far apart individual expectations can be. When you set that against Boot Barn’s store expansion push and reliance on same-store sales and margin gains, it becomes clear that different investors are weighing execution risk and growth potential very differently. You are not short of alternative viewpoints to compare with your own assumptions.

Explore 5 other fair value estimates on Boot Barn Holdings - why the stock might be worth less than half the current price!

Disagree with this assessment? Create your own narrative in under 3 minutes - extraordinary investment returns rarely come from following the herd.

The market won't wait. These fast-moving stocks are hot now. Grab the list before they run:

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.