Please use a PC Browser to access Register-Tadawul

Get It

Can Analyst Support for Valero’s (VLO) Refining Business Shift the Long-Term Transition Narrative?

Valero Energy Corporation VLO | 202.68 | +4.40% |

Trump has pledged to "unleash" American oil and gas and these 22 US stocks have developments that are poised to benefit.

To own shares of Valero Energy today, one mainly has to believe in the company's continued resilience in its core refining business amid ongoing industry headwinds, especially as it balances traditional fuels with the gradual move toward renewables. Piper Sandler’s reaffirmed confidence, reflected in a raised price target, underscores near-term optimism about Valero’s refining operations; however, it does not materially alter the current short-term catalyst or the primary risk, which centers on ongoing challenges in renewable diesel margins due to regulatory uncertainty.

Among recent developments, Valero’s decision to maintain its quarterly cash dividend at US$1.13 per share stands out, especially given the analyst attention on financial strength and shareholder returns. This move reinforces the ongoing catalyst for investors: stable and shareholder-friendly capital allocation, even as other segments of the business remain under pressure.

Yet, on the other hand, investors should not overlook the impact that more stringent regulatory measures could have on…

Valero Energy's outlook anticipates $116.7 billion in revenue and $3.9 billion in earnings by 2028. This reflects a 0.2% annual revenue decline and a $3.14 billion increase in earnings from the current $760 million.

Uncover how Valero Energy's forecasts yield a $155.67 fair value, a 17% upside to its current price.

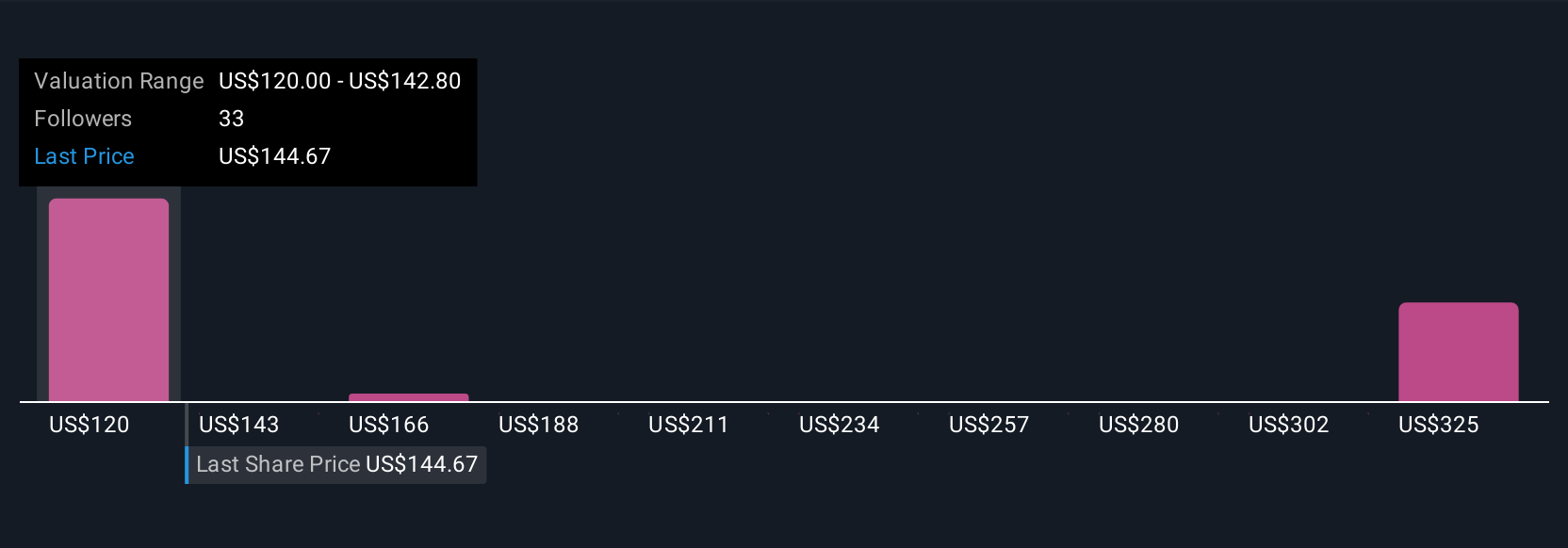

Five members of the Simply Wall St Community estimate Valero’s fair value from US$115.01 up to US$305.39 per share. While many see financial resilience as a key strength, close attention is warranted on policy risks that could impact renewable diesel profitability.

Explore 5 other fair value estimates on Valero Energy - why the stock might be worth over 2x more than the current price!

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

The market won't wait. These fast-moving stocks are hot now. Grab the list before they run:

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.