Please use a PC Browser to access Register-Tadawul

Get It

Check Point Software (CHKP) Margin Expansion Reinforces Bullish Narratives Despite Earnings Decline Forecast

Check Point Software Technologies Ltd. CHKP | 193.06 | -1.41% |

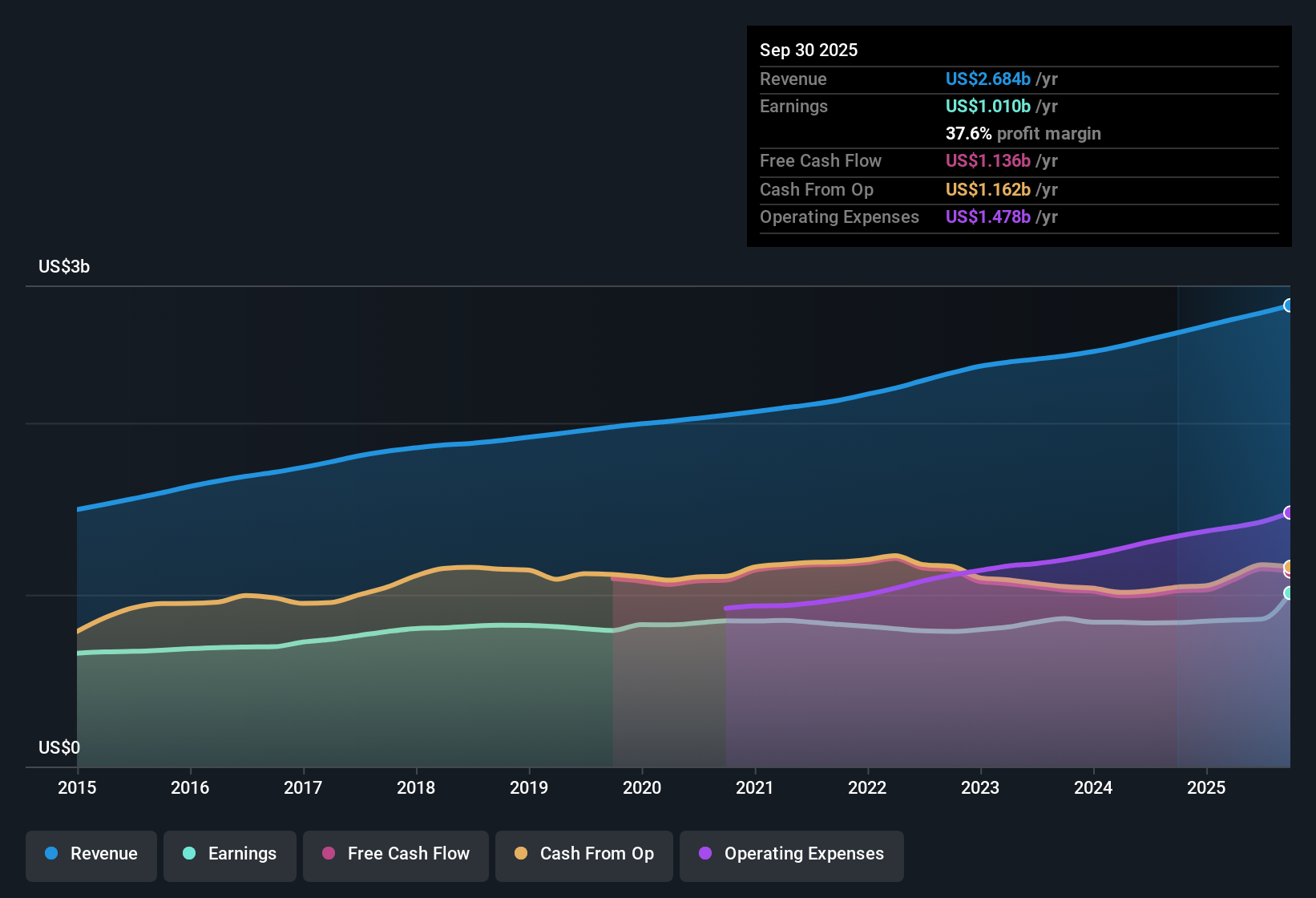

Check Point Software Technologies (CHKP) reported annual earnings growth of 1.5% over the past five years, but recently posted a sharp acceleration with earnings up 20.6% and net profit margins improving to 37.6% from 33.2% last year. However, compared to the broader US software sector, revenue is forecast to rise at a slower pace of 5.8% per year and earnings are expected to decline by 1.5% per year over the next three years. While the company trades at a relatively attractive 21 times Price-to-Earnings ratio compared to industry peers, the share price of $197.28 currently sits above the estimated fair value, creating a mixed picture for investors.

See our full analysis for Check Point Software Technologies.The next section puts these headline numbers up against the most widely discussed investor narratives, highlighting where expectations are confirmed and where the story takes a turn.

Consensus signals provide a balanced perspective on these improvements and the strategic shifts ahead. Read the full Consensus Narrative for a rounded perspective. 📊 Read the full Check Point Software Technologies Consensus Narrative.

To see how these results tie into long-term growth, risks, and valuation, check out the full range of community narratives for Check Point Software Technologies on Simply Wall St. Add the company to your watchlist or portfolio so you'll be alerted when the story evolves.

Curious about a different interpretation of the data? Take just a few minutes to shape your own perspective and share your unique view. Do it your way

A great starting point for your Check Point Software Technologies research is our analysis highlighting 3 key rewards and 1 important warning sign that could impact your investment decision.

Despite recent profit margin gains, Check Point faces slowing long-term revenue and earnings forecasts, which puts its premium valuation at risk compared to faster-growing competitors.

If you want exposure to companies where the numbers are pointing up year after year, use stable growth stocks screener (2122 results) to focus on steady performers with more reliable growth outlooks.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.