Please use a PC Browser to access Register-Tadawul

Get It

City Holding (CHCO) Valuation Check After Recent Share Moves And DCF Versus P/E Signals

City Holding Company CHCO | 124.96 | +0.22% |

City Holding (CHCO) is back on investor radars after recent share moves, with the stock last closing at $123.28. You might be weighing how its recent returns and fundamentals line up today.

The recent share price has held close to $123.28, with a 1 year to date share price return of 2.83% and a 1 year total shareholder return of 5.89%. The 5 year total shareholder return of 99.05% points to momentum that has built over time rather than short term swings.

If City Holding has you looking more closely at regional banks, it can also be useful to compare them with broader financial names and broaden your search with fast growing stocks with high insider ownership.

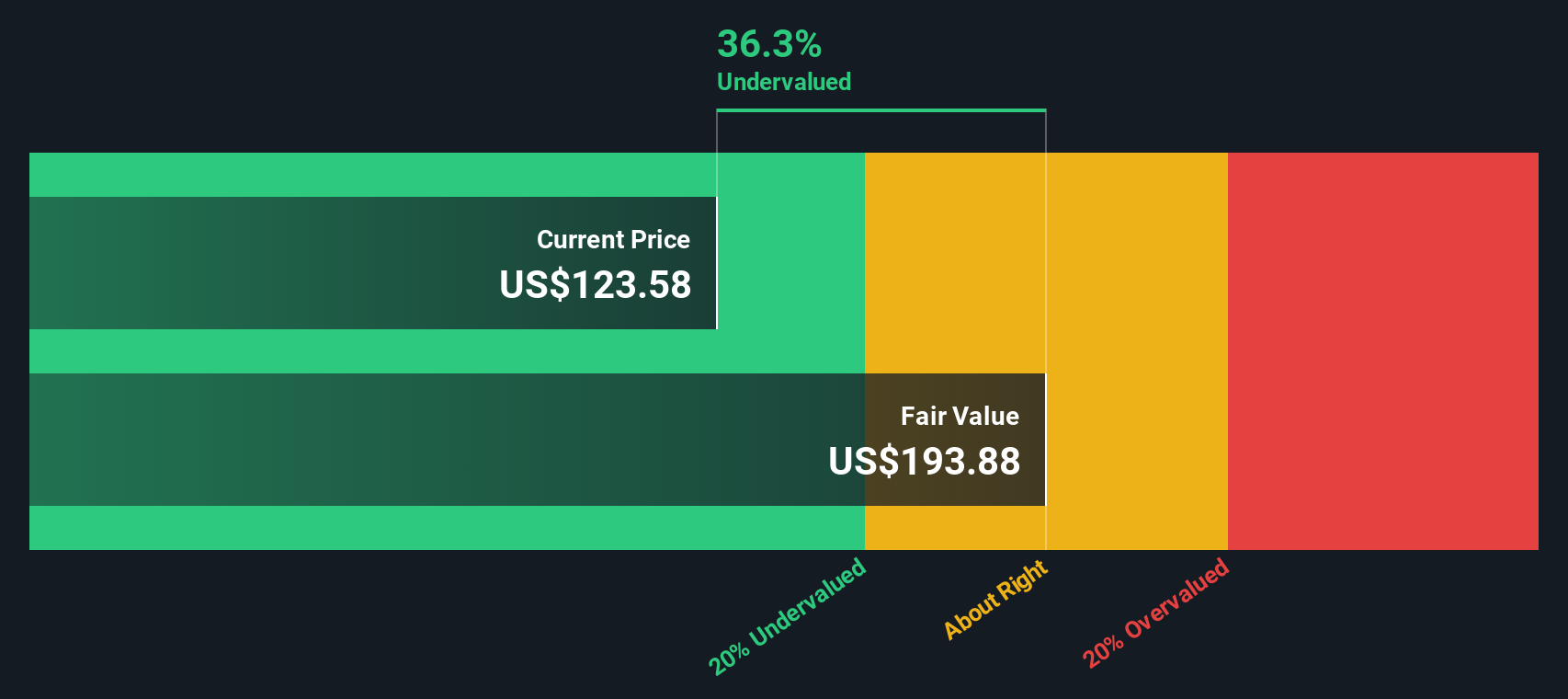

So with solid long term total returns, a recent share price around $123.28, and an indicated intrinsic discount of about 38%, is City Holding quietly undervalued, or is the market already baking in its future growth?

City Holding trades on a P/E of 14x, while our DCF work suggests a fair value of about US$198.83 per share versus the last close of US$123.28.

The P/E multiple tells you how much investors are currently paying for each dollar of earnings. This is a common yardstick for banks where profits and returns on equity are closely watched. For City Holding, the current 14x P/E sits above the estimated fair P/E of 9.9x in the SWS framework, which indicates that the market is assigning a richer tag to its earnings than that fair ratio implies.

Relative to other US banks, City Holding screens as expensive on this measure, with its 14x P/E higher than both the industry average of 11.9x and the peer average of 12.1x. Against the fair ratio benchmark of 9.9x, the gap is even wider. This is a level the market could move toward if sentiment or expectations reset closer to that fair multiple.

Result: Price-to-Earnings of 14x (OVERVALUED)

However, there are pressure points to keep in mind, including flat net income growth and the risk that a richer P/E multiple compresses if sentiment cools.

While the 14x P/E suggests City Holding trades at a premium to banks, our DCF model indicates something different. On that measure, the shares sit about 38% below an estimated fair value of US$198.83, which presents the current price as potentially cheap rather than stretched. So which lens matters more for you?

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out City Holding for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 873 undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

If you interpret the numbers differently or prefer to test your own assumptions, you can build a custom view in just a few minutes by starting with Do it your way.

A great starting point for your City Holding research is our analysis highlighting 3 key rewards and 2 important warning signs that could impact your investment decision.

If City Holding has sparked your interest, consider widening your watchlist with a few focused stock sets that match different goals and themes.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.