Please use a PC Browser to access Register-Tadawul

Get It

CrowdStrike (CRWD) Is Up 8.8% After Surge in Contract Renewals Driven by AI and Platform Integration

CrowdStrike CRWD | 504.78 | -2.49% |

These 15 companies survived and thrived after COVID and have the right ingredients to survive Trump's tariffs. Discover why before your portfolio feels the trade war pinch.

To own CrowdStrike, you need to believe its innovation-led platform strategy and expanding AI capabilities can propel sustained customer and revenue growth in the competitive cybersecurity market. While recent news around contract renewals and partner ecosystem enhancements reinforces the momentum behind key customer and product catalysts, it does not materially alter the biggest short-term risk, whether new product launches and acquisitions will consistently deliver anticipated growth and margin benefits, or introduce execution volatility.

Among recent developments, the launch of Falcon Data Protection stands out for its relevance as enterprises grapple with AI-driven threat sophistication. This product directly addresses rising compliance, cloud security, and data protection demands, which is at the heart of CrowdStrike’s effort to deepen customer lock-in and support contract value expansion, aligning closely with the catalysts supporting its growth outlook.

Yet, it’s worth noting that if CrowdStrike fails to maintain high customer retention or struggles with Falcon Flex execution, investors should be aware that ...

CrowdStrike Holdings' outlook projects $7.9 billion in revenue and $691.1 million in earnings by 2028. This is based on analysts forecasting a 22.1% annual revenue growth rate and an $988.1 million increase in earnings from the current level of -$297.0 million.

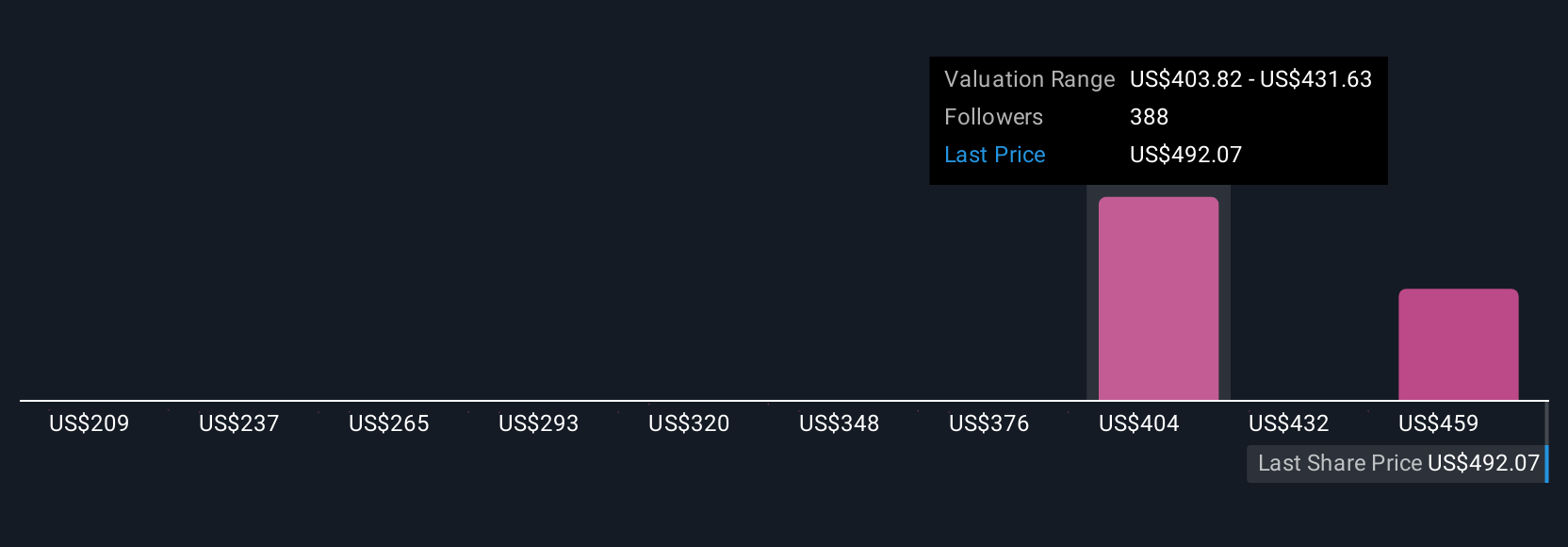

Uncover how CrowdStrike Holdings' forecasts yield a $498.91 fair value, a 5% downside to its current price.

Simply Wall St Community members provided 29 fair value estimates for CrowdStrike, spanning US$277 to US$600, highlighting wide-ranging views. In light of ongoing platform innovation, readers should explore several alternative viewpoints on growth prospects and potential risks.

Explore 29 other fair value estimates on CrowdStrike Holdings - why the stock might be worth 47% less than the current price!

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

Markets shift fast. These stocks won't stay hidden for long. Get the list while it matters:

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.