Please use a PC Browser to access Register-Tadawul

Get It

CSW Industrials (CSWI) Margin Improvement Tests Bullish Earnings Narratives

CSW Industrials, Inc. CSW | 311.40 | +0.22% |

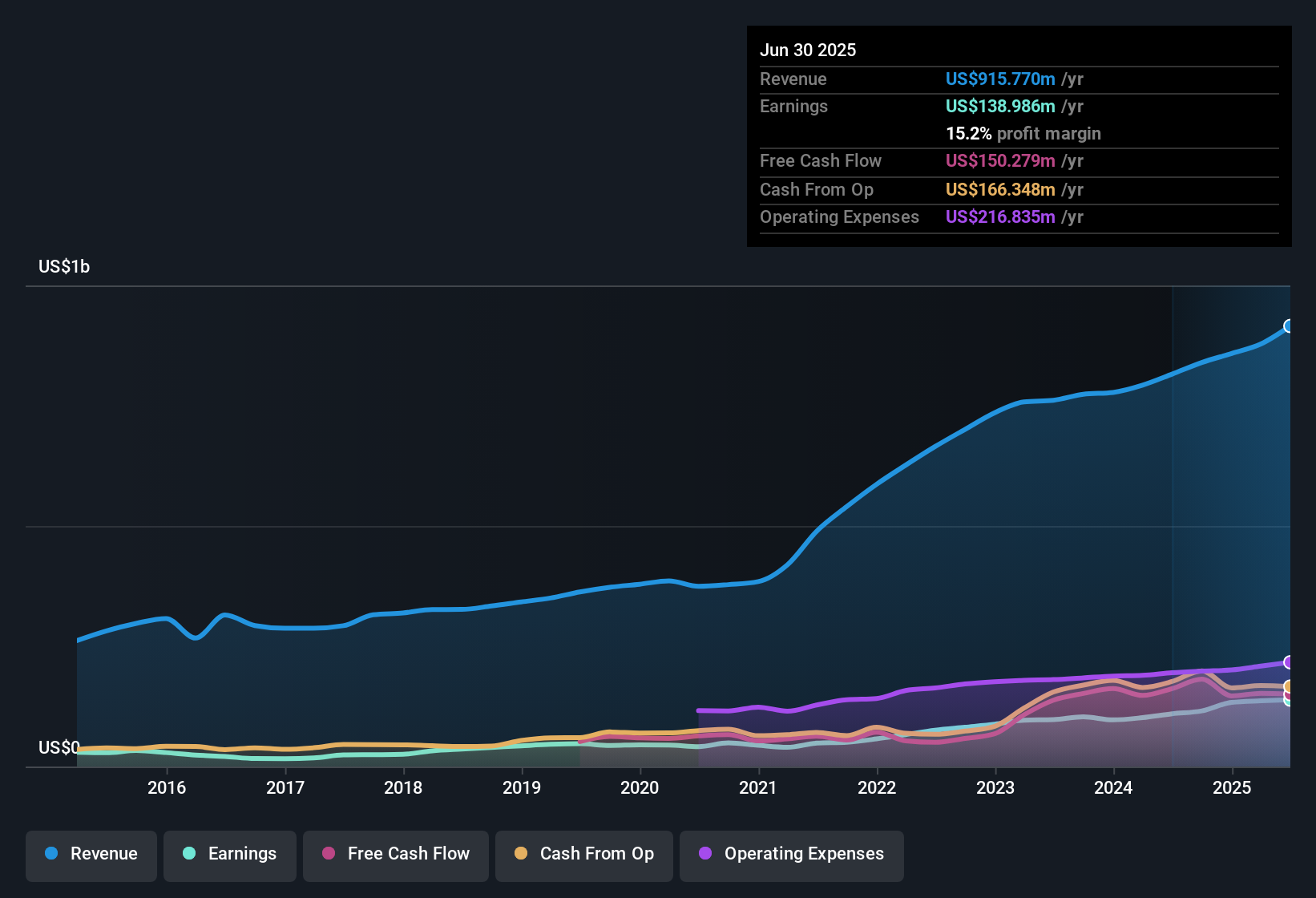

CSW Industrials (CSWI) has put up another solid quarter in Q3 2026, with quarterly context showing revenue moving from US$193.6 million in Q3 2025 to US$276.9 million in Q2 2026. EPS shifted from US$1.60 to US$2.42 over the same period, and trailing twelve month EPS reached US$8.55 on revenue of US$964.8 million. Over the last year, net income for the trailing twelve months rose from US$115.6 million to US$143.6 million as margins widened from 13.8% to 14.9%. This sets the scene for investors to focus on how durable this earnings profile looks as the latest results reset expectations for profitability.

See our full analysis for CSW Industrials.With the headline numbers on the table, the next step is to see how this earnings run rate lines up against the prevailing narratives around CSW Industrials and to examine where the latest margin picture supports or challenges those views.

Don't just look at this quarter; the real story is in the long-term trend. We've done an in-depth analysis on CSW Industrials's growth and its valuation to see if today's price is a bargain. Add the company to your watchlist or portfolio now so you don't miss the next big move.

CSW Industrials’ premium 34.5x P/E against lower industry multiples and a DCF fair value of US$196.61 versus a US$274.36 share price puts the spotlight on valuation risk.

If that kind of pricing makes you cautious, check out these 864 undervalued stocks based on cash flows to focus on companies where current prices look more aligned with underlying cash flow support.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.