Please use a PC Browser to access Register-Tadawul

Get It

Did Weak Earnings and a Pause in Buybacks Shift Madison Square Garden Sports' (MSGS) Investment Narrative?

Madison Square Garden Co. Class A MSGS | 316.49 | +0.90% |

AI is about to change healthcare. These 32 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

To be a shareholder in Madison Square Garden Sports, you need to believe in the long-term appeal and monetization potential of flagship franchises like the Knicks and Rangers, especially as national media rights fees ramp up in the coming years. The recent decline in sales and widening net loss reported this quarter do not appear to materially alter the biggest short term catalyst, anticipated growth in national media rights revenue, but they do reinforce the main risk: heavy dependence on local team performance and related revenue streams. Among recent updates, the lack of share buybacks in the latest quarter stands out, especially given the company’s history of significant repurchases. This inactivity may signal a more cautious approach during periods of weaker earnings, which could affect capital returns to shareholders if top-line performance continues to lag, especially as the company looks to offset pressure from declining local media revenue. However, what investors should really keep in mind is that, unlike the expected national media boost, local media rights fees...

Madison Square Garden Sports is expected to deliver $1.1 billion in revenue and $102.9 million in earnings by 2028. This forecast requires 1.6% annual revenue growth and a $125.4 million increase in earnings from their current earnings of -$22.5 million.

Uncover how Madison Square Garden Sports' forecasts yield a $265.00 fair value, a 21% upside to its current price.

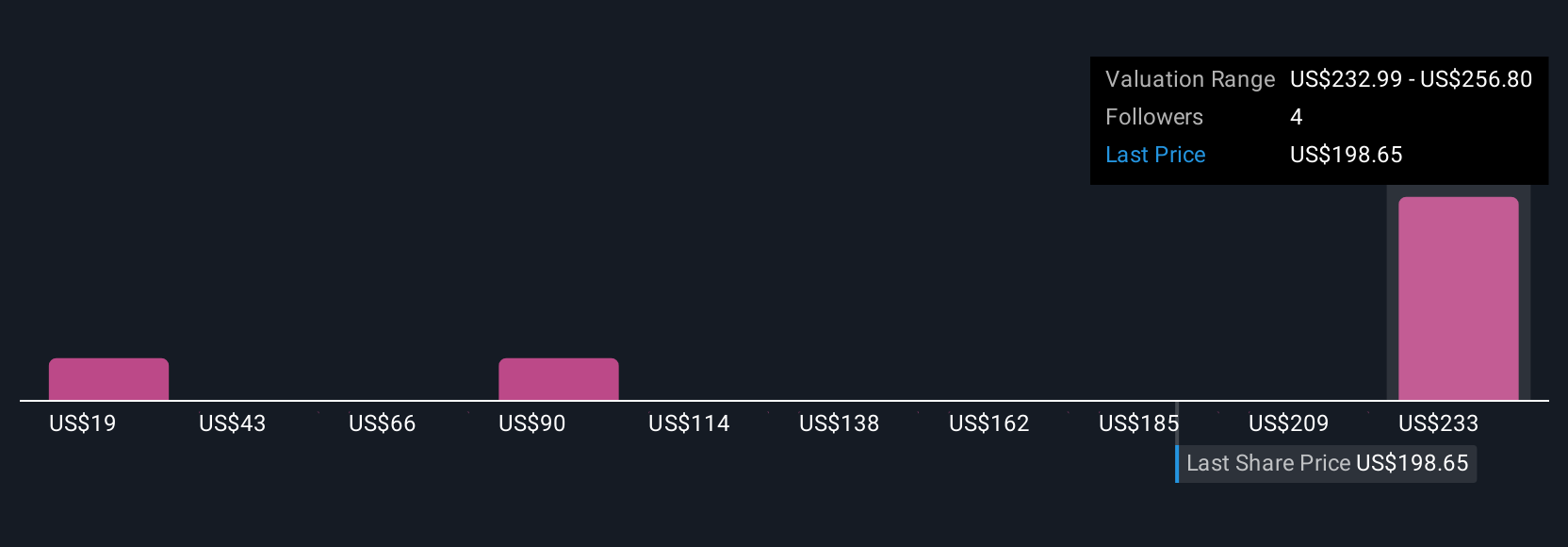

Three private investors in the Simply Wall St Community provided fair value estimates ranging from US$18.37 to US$265, reflecting widely different opinions on the stock. While some see upside, the risk of structural declines in core local media revenue may weigh on performance, making it vital to compare these diverse perspectives.

Explore 3 other fair value estimates on Madison Square Garden Sports - why the stock might be worth less than half the current price!

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

Right now could be the best entry point. These picks are fresh from our daily scans. Don't delay:

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.