Please use a PC Browser to access Register-Tadawul

Get It

Does Accenture's AI Partnerships Signal a New Value Opportunity After 28.9% Share Price Drop?

Accenture Plc Class A ACN | 199.99 | -1.75% |

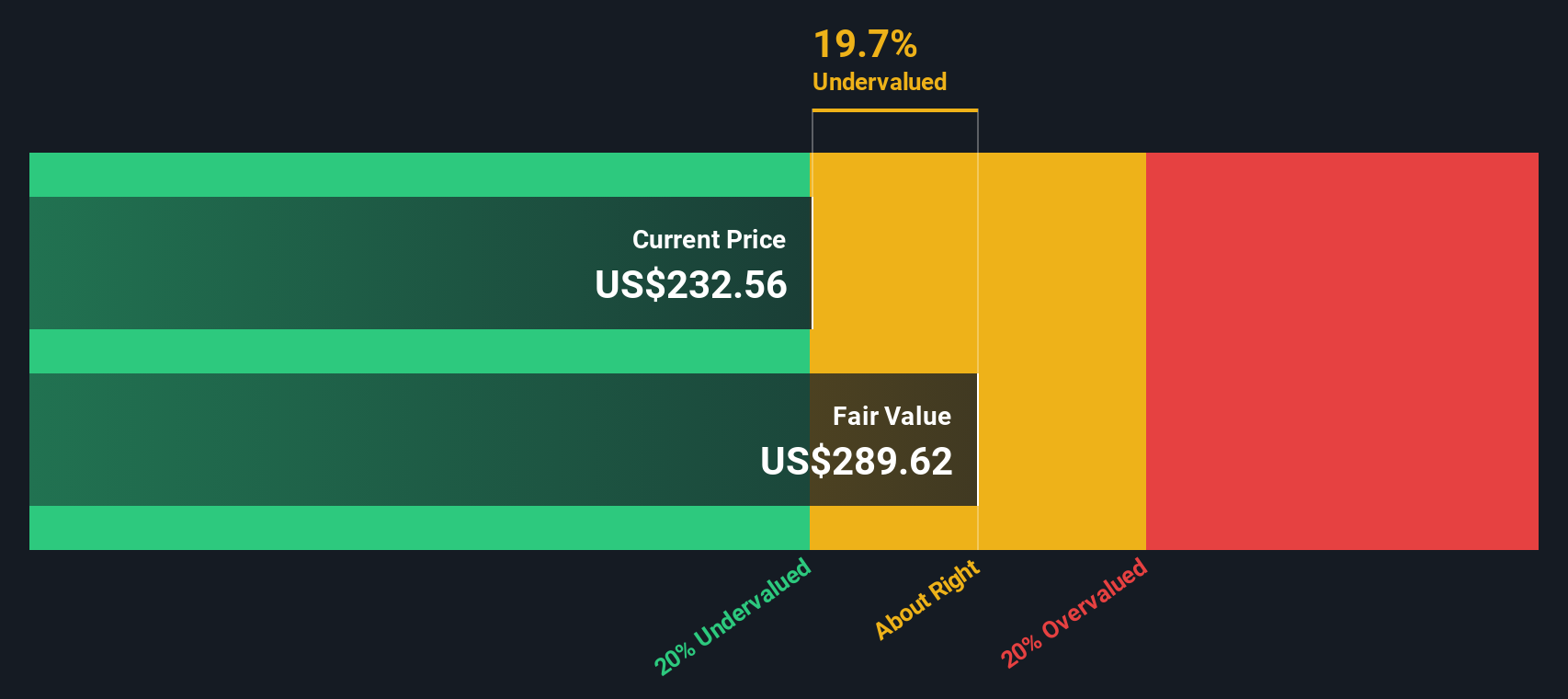

The Discounted Cash Flow (DCF) model estimates a company's true value by projecting its future free cash flows and discounting them back to today's dollar value. This process helps investors gauge what the business is genuinely worth, aside from current market noise.

Accenture currently generates $10.9 billion in free cash flow. Analyst projections, which cover the next five years, suggest steady growth in these cash flows, with subsequent years extrapolated by Simply Wall St. By 2029, Accenture’s free cash flow is forecasted to reach around $12.4 billion. Ten-year projections indicate continued modest increases, with a forecast of about $14.8 billion in 2035.

Using these forward-looking cash flows in the DCF model puts Accenture’s intrinsic value at $275.58 per share. This figure is 10.1% above the recent share price, suggesting the stock is currently undervalued according to the DCF approach.

Result: UNDERVALUED

Our Discounted Cash Flow (DCF) analysis suggests Accenture is undervalued by 10.1%. Track this in your watchlist or portfolio, or discover 932 more undervalued stocks based on cash flows.

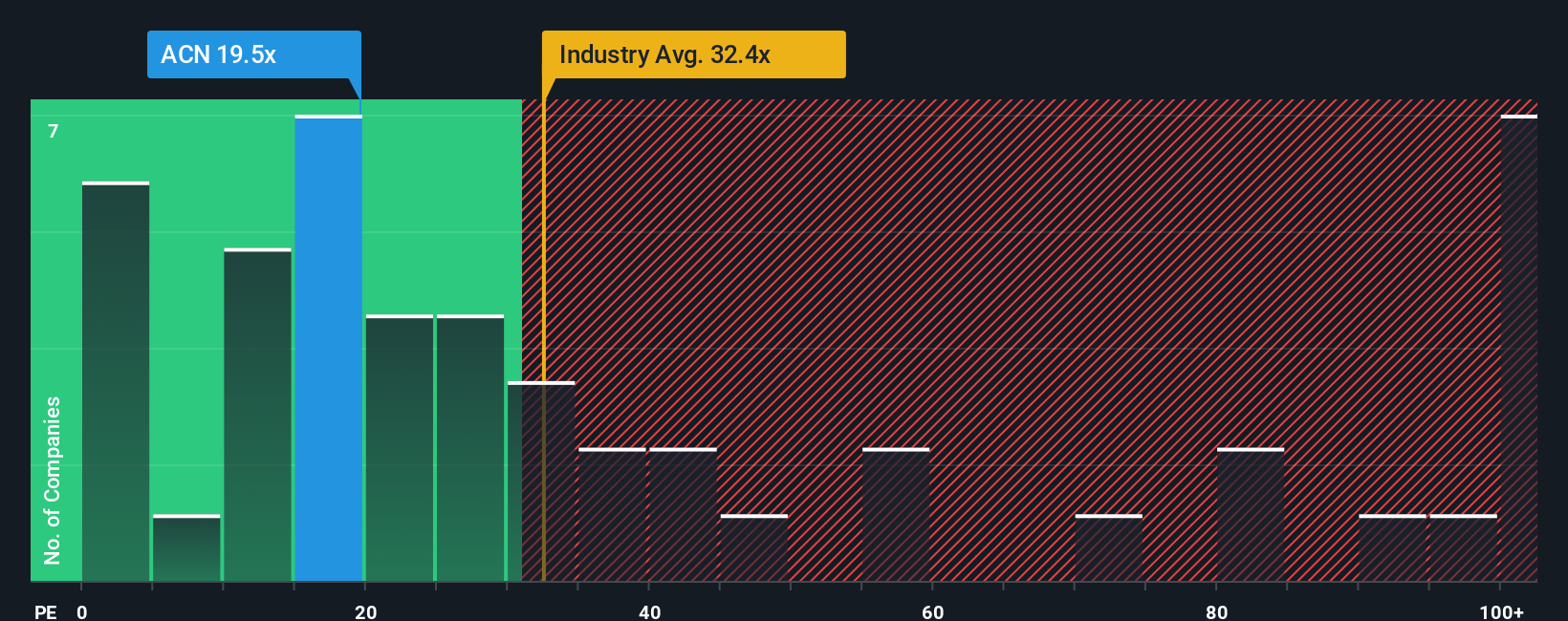

The Price-to-Earnings (PE) ratio is widely used to value profitable companies like Accenture because it quickly shows how much investors are willing to pay for current earnings. For established businesses with stable profits, PE ratios offer a straightforward snapshot of market sentiment about the company’s earnings power.

What counts as a “fair” PE ratio often depends on a company’s expected growth, profitability, and the perceived risks it faces. Higher growth and lower risk tend to justify higher PE ratios; lower growth or additional uncertainties might warrant a lower ratio.

Accenture currently trades at a PE ratio of 20x. This is below the IT industry’s average PE of 27.8x and also lower than the average of its peers, which sits at 25x. Instead of just comparing PE ratios in isolation, Simply Wall St uses a proprietary “Fair Ratio” that analyzes variables such as Accenture’s earnings growth, profit margins, industry, market capitalization, and risk levels. For Accenture, the Fair Ratio is calculated at 38.2x, significantly higher than its current 20x multiple.

This Fair Ratio approach offers a more complete view by factoring in not just how Accenture compares to similar companies, but also how its unique qualities and market position affect its fair value. This broader context suggests that Accenture’s shares may actually be undervalued at their current price.

Result: UNDERVALUED

PE ratios tell one story, but what if the real opportunity lies elsewhere? Discover 1441 companies where insiders are betting big on explosive growth.

Earlier we mentioned that there is an even better way to understand valuation, so let us introduce you to Narratives. A Narrative is simply a story that represents your viewpoint about a company’s future, brought to life with real financial forecasts, including your assumptions about fair value, future revenue, earnings, and margins.

Narratives connect what you believe about a company to how it could perform, helping you turn your research and perspective into a data-driven outlook. On Simply Wall St’s Community page, millions of investors use Narratives as an accessible tool to transform opinions into actionable investing ideas.

With Narratives, you can instantly see how your story lines up against the current share price. If your fair value is higher than today’s price, it might be a buy; if lower, it might be time to wait or sell. Plus, whenever news breaks or earnings are updated, your Narrative and its valuation adjust automatically, ensuring your decisions reflect the latest facts.

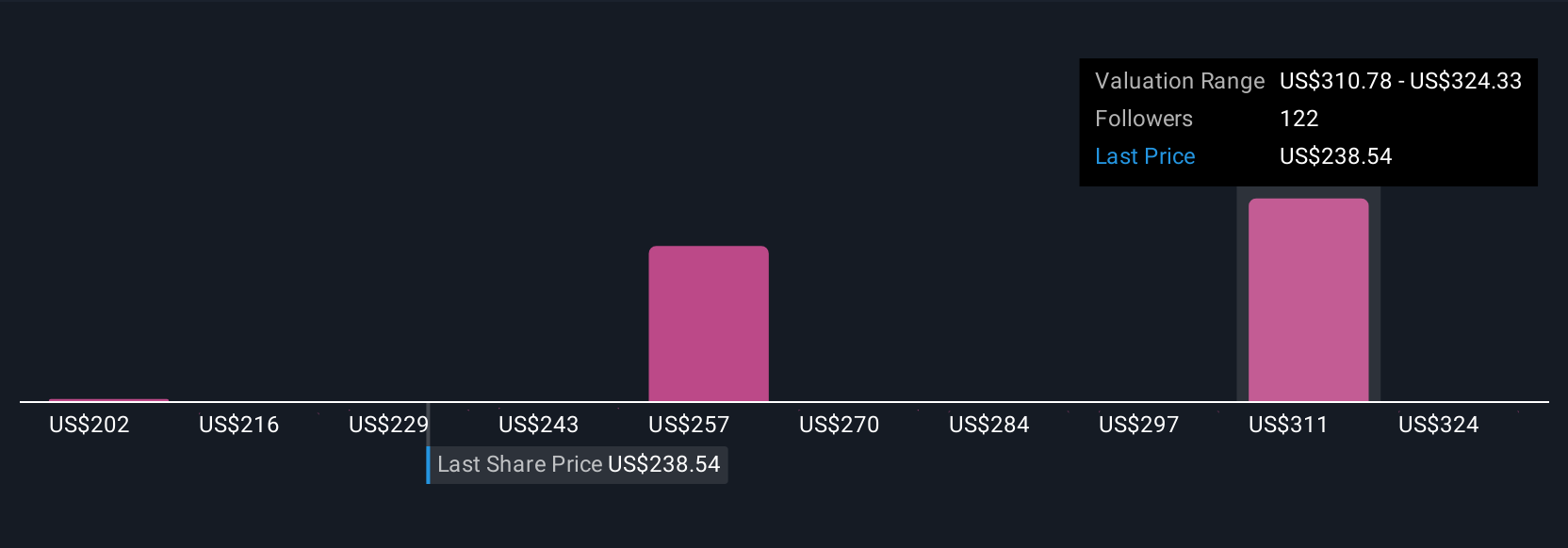

For example, recent Accenture Narratives reveal differences in investor outlooks. A cautious view values shares at $202 based on margin pressures, while an optimistic perspective sees fair value at $372 citing AI-driven revenue growth. This highlights how the right Narrative can guide your next move.

For Accenture, here are previews of two leading Accenture Narratives:

Fair Value: $277.60

Current valuation: 10.7% undervalued

Revenue Growth Forecast: 5.7%

Fair Value: $202.38

Current valuation: 22.5% overvalued

Revenue Growth Forecast: 5.4%

Do you think there's more to the story for Accenture? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.