Please use a PC Browser to access Register-Tadawul

Get It

Does Clorox’s ERP Transition Set the Stage for Long-Term Efficiency Gains for CLX Investors?

Clorox Company CLX | 126.81 | -0.28% |

These 13 companies survived and thrived after COVID and have the right ingredients to survive Trump's tariffs. Discover why before your portfolio feels the trade war pinch.

To be a Clorox shareholder, you need confidence in the company’s ability to drive long-term efficiency gains and margin expansion as it navigates category headwinds and shifting consumer preferences. The latest earnings did not materially change the near-term catalyst of ERP-driven operational improvements, though persistent sales declines and uncertain demand remain the foremost risks weighing on the outlook.

Of the recent announcements, management’s reaffirmed guidance for fiscal 2026 stands out, with net sales projected to decline 6% to 10% despite the successful ERP rollout. This signals that, while ERP benefits are beginning to surface, top-line growth challenges and the pace of category recovery are still key issues for the business.

Yet, investors should be aware that despite visible ERP progress, Clorox’s exposure to ongoing price competition and sluggish consumer categories means ...

Clorox is projected to reach $7.0 billion in revenue and $881.8 million in earnings by 2028. This outlook assumes a 0.4% annual decline in revenue and a $71.8 million increase in earnings from the current $810.0 million.

Uncover how Clorox's forecasts yield a $124.76 fair value, a 20% upside to its current price.

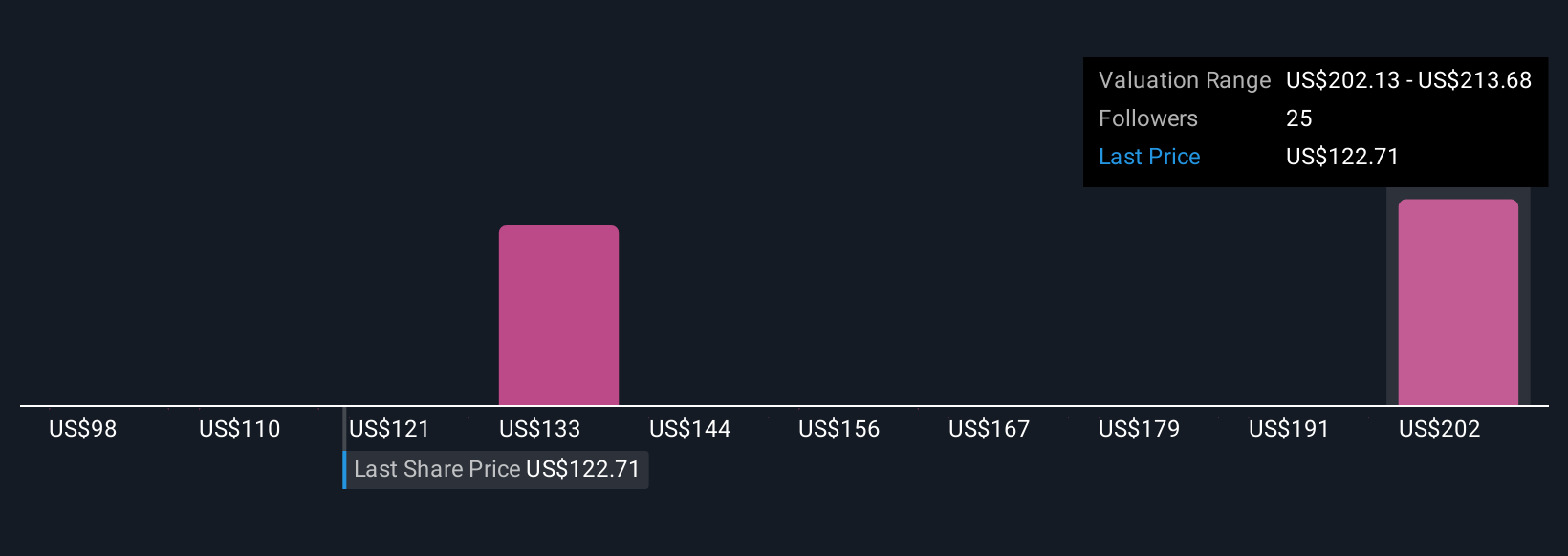

Six Simply Wall St Community members’ fair value estimates for Clorox range widely between US$98.22 and US$213.56. While some see ERP-led efficiency as a catalyst for future margin improvement, persistent sales pressures invite a closer look at how expectations can sharply diverge across the market.

Explore 6 other fair value estimates on Clorox - why the stock might be worth over 2x more than the current price!

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

The market won't wait. These fast-moving stocks are hot now. Grab the list before they run:

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.