Please use a PC Browser to access Register-Tadawul

Get It

Does Warrior Met Coal's (HCC) Credit Expansion Reflect a New Commitment to Long-Term Production Growth?

Warrior Met Coal, Inc. HCC | 83.55 | +0.05% |

Trump has pledged to "unleash" American oil and gas and these 22 US stocks have developments that are poised to benefit.

To be a shareholder of Warrior Met Coal today, you need to believe in the company's ability to deliver higher volumes and margin improvement from the Blue Creek project, while managing volatile coal prices and shifting Asian demand. The recent expansion and extension of its credit facility directly supports Blue Creek’s ramp to full production, which is the key short-term catalyst; however, this move also heightens exposure to operational and placement risks if market conditions remain weak.

The most relevant recent announcement is Warrior Met Coal's increase in production and sales guidance for 2025, which aligns with Blue Creek's anticipated longwall startup. While the expanded credit facility bolsters financial flexibility for this major growth initiative, investor focus remains fixed on whether expanded output can translate into margin recovery amid challenging price fundamentals.

By contrast, investors should also be aware that growing dependence on Asian demand introduces new risks that...

Warrior Met Coal's outlook anticipates $2.0 billion in revenue and $636.5 million in earnings by 2028. This is based on analysts' expectations of 18.8% annual revenue growth and a $596 million increase in earnings from the current $40.3 million.

Uncover how Warrior Met Coal's forecasts yield a $65.67 fair value, a 4% upside to its current price.

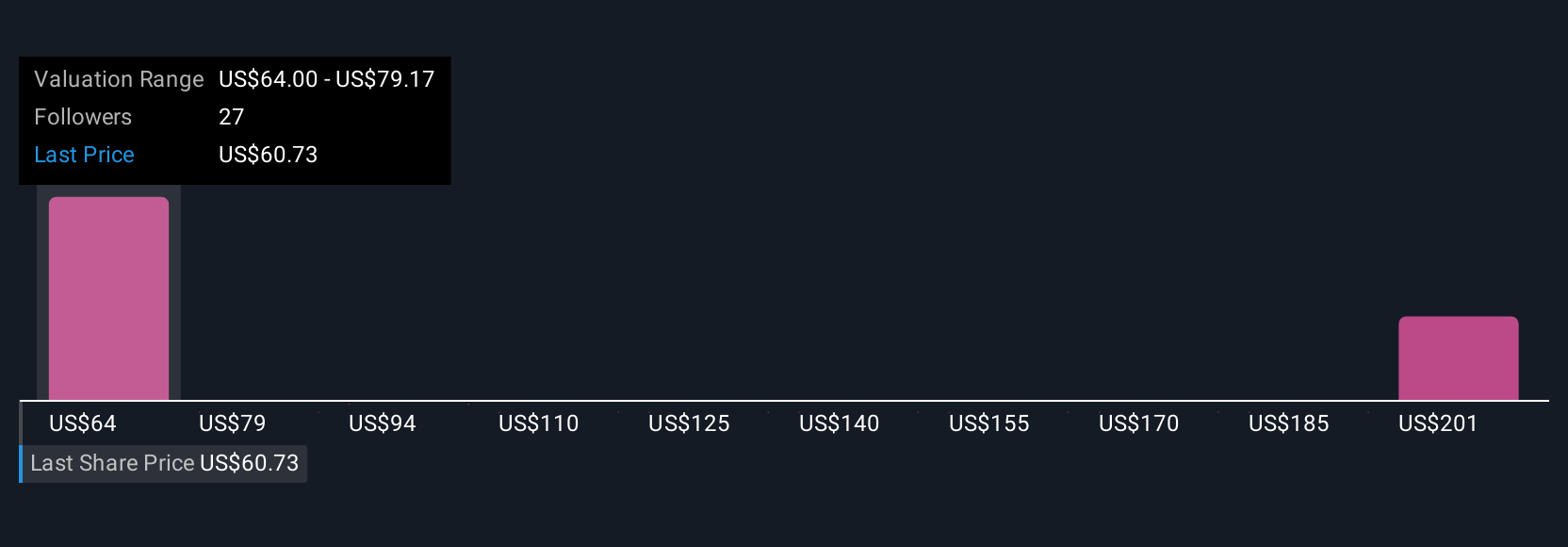

Private investors within the Simply Wall St Community assigned fair values ranging from US$65.67 to US$210.44 across 5 personal estimates. While optimism around Blue Creek’s capacity increase is strong, persistent pressure on coal pricing could challenge these assumptions and shape your own view of Warrior Met Coal’s outlook.

Explore 5 other fair value estimates on Warrior Met Coal - why the stock might be worth just $65.67!

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

Our top stock finds are flying under the radar-for now. Get in early:

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.