Please use a PC Browser to access Register-Tadawul

Get It

Enova International (ENVA) Earnings Jump 47.2% Challenges Longer Term Bearish Narratives

Enova International Inc ENVA | 145.33 | +0.21% |

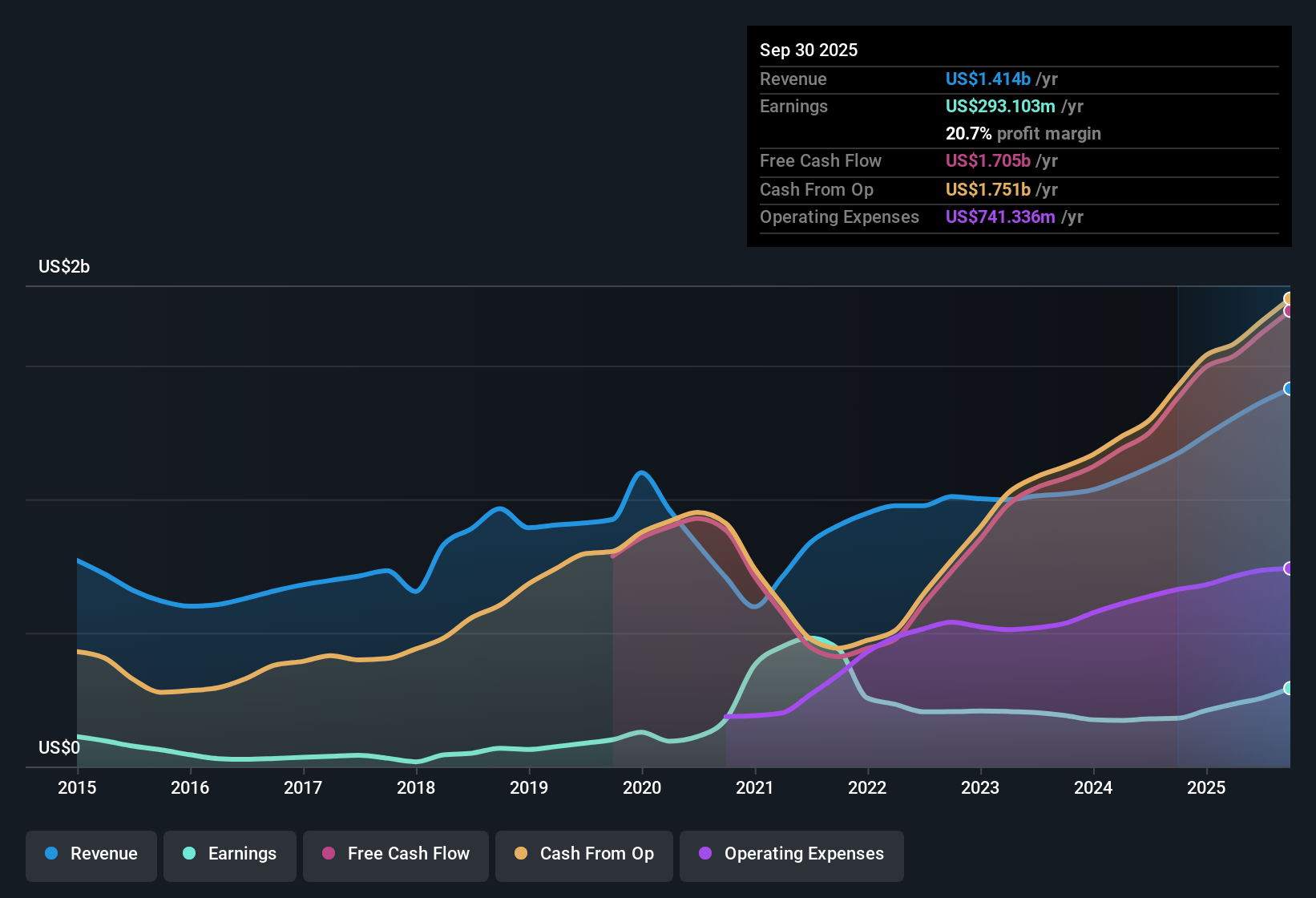

Enova International (ENVA) has capped FY 2025 with fourth quarter revenue of US$412.9 million and basic EPS of US$3.19, while trailing twelve month EPS sits at US$12.25 on revenue of about US$1.5 billion. The company has seen quarterly revenue move from US$323.5 million in Q3 2024 to US$412.9 million in Q4 2025, with basic EPS over that stretch ranging from US$1.64 to just above US$3 per share. With net margin at 20.7% over the last year versus 16.9% previously, the latest numbers indicate profitability that has become more supportive of the current earnings story.

See our full analysis for Enova International.With the headline results set, the next step is to compare these margins and growth figures with the widely followed narratives around Enova and to consider where the story investors tell themselves might differ from what the numbers suggest.

Don't just look at this quarter; the real story is in the long-term trend. We've done an in-depth analysis on Enova International's growth and its valuation to see if today's price is a bargain. Add the company to your watchlist or portfolio now so you don't miss the next big move.

Enova's 47.2% one year earnings gain and 20.7% net margin sit against a five year earnings decline of about 12.3% per year and a DCF value well below the current share price.

If that mix of long term earnings pressure and valuation questions feels uncomfortable, use our these 876 undervalued stocks based on cash flows today to focus on ideas where the price tag appears more closely aligned with fundamentals.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.