Entegris (ENTG) Margin Decline To 7.4% Tests Bullish Earnings Growth Narratives

Entegris, Inc. ENTG | 137.44 | -0.46% |

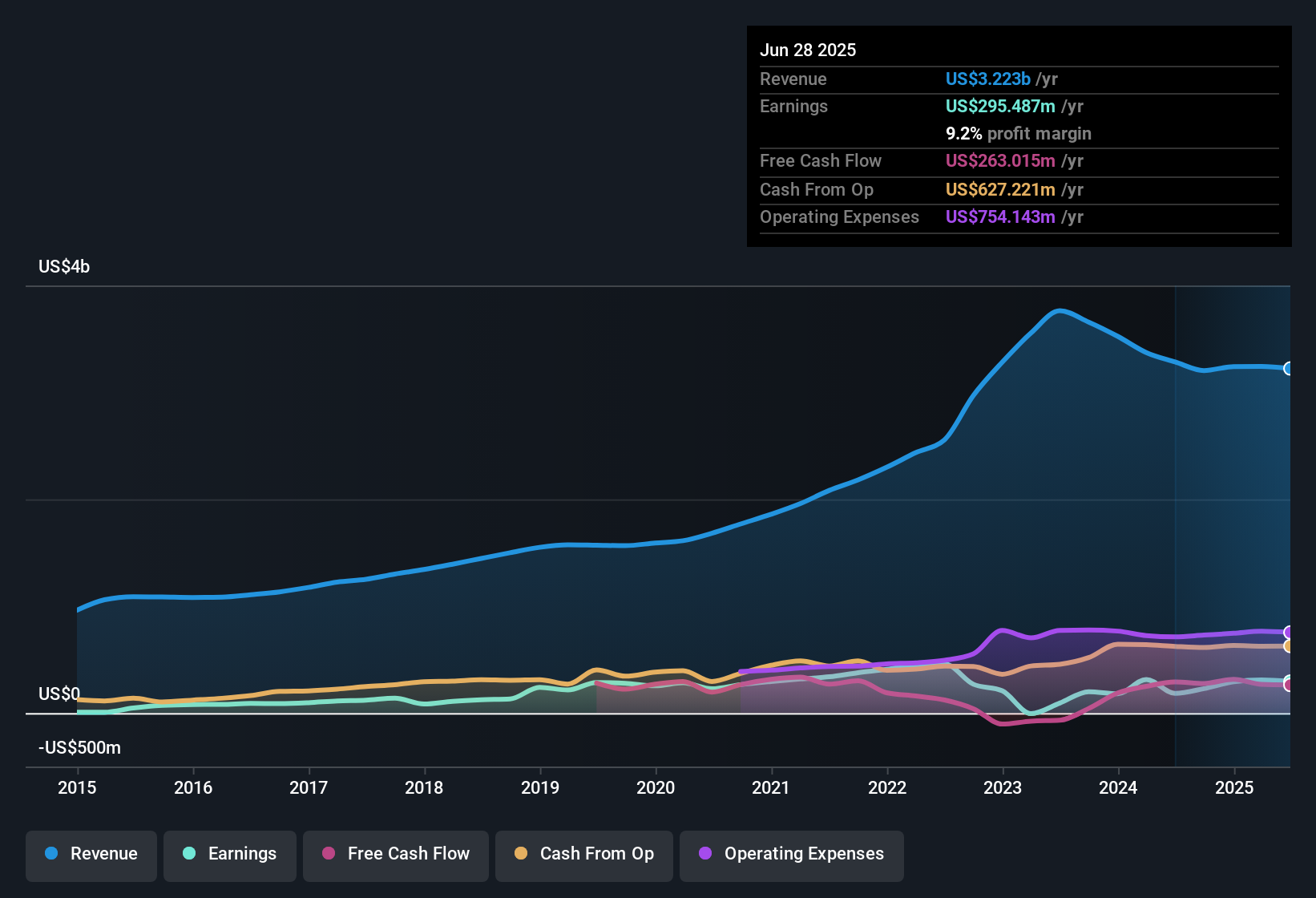

Entegris (ENTG) has wrapped up FY 2025 with fourth quarter revenue of US$823.9 million and basic EPS of US$0.33, alongside trailing twelve month revenue of about US$3.2 billion and EPS of US$1.55. Over the past six reported quarters, revenue has moved within a tight band from US$773.2 million to US$849.8 million, while quarterly EPS has ranged from US$0.33 to US$0.68. This gives investors a clear view of how the top line and EPS have tracked together through the cycle. With net income over the last twelve months at US$235.6 million and a net margin of 7.4%, the focus now shifts to how sustainable these margins look in light of recent results.

See our full analysis for Entegris.With the latest earnings on the table, the next step is to see how these numbers line up with the widely followed narratives around Entegris, and where the data may challenge or reinforce what investors currently believe about the business.

Margins Slip From 9% To 7.4%

- On a trailing twelve month basis, Entegris earned US$235.6 million of net income on US$3.2b of revenue, which works out to a 7.4% net margin compared with 9% last year according to the risk summary.

- Consensus narrative expects profit margins to move higher over time. However, the recent step down from 9% to 7.4% means investors are watching how quickly new facilities and cost initiatives translate into the higher margin profile analysts have in mind.

EPS Trend Versus Bullish Growth Story

- Trailing twelve month basic EPS has moved from US$2.05 at FY 2025 Q1 to US$1.55 at FY 2025 Q4, even though analysts are forecasting around 20.1% yearly earnings growth from here.

- Bulls see Entegris as a long term earnings compounder. Yet the recent TTM EPS drift from US$2.05 to US$1.55 invites a closer look at how quickly AI and advanced node demand might need to feed through to support the higher earnings paths bullish investors are focusing on.

Rich Valuation With 85.9x P/E

- The shares trade at a P/E of 85.9x versus 44.2x for the broader US Semiconductor industry and 45.1x for peers, while the current price of US$133.44 also sits well above the DCF fair value estimate of US$67.83.

- Bears point to this valuation gap and the weaker interest coverage as key concerns, and the combination of an 85.9x P/E and margins that softened to 7.4% gives those cautious views plenty of concrete numbers to anchor on.

Next Steps

To see how these results tie into long-term growth, risks, and valuation, check out the full range of community narratives for Entegris on Simply Wall St. Add the company to your watchlist or portfolio so you'll be alerted when the story evolves.

See the numbers differently? If this data points you in another direction, shape your own take in just a few minutes and share it with the community. Do it your way

A great starting point for your Entegris research is our analysis highlighting 1 key reward and 1 important warning sign that could impact your investment decision.

See What Else Is Out There

Entegris currently combines a 7.4% net margin, softer trailing EPS and an 85.9x P/E, which leaves little room for comfort if expectations shift.

If that rich valuation and tighter margin profile feels like a stretch, it is worth checking companies on our 51 high quality undervalued stocks that pair more grounded pricing with solid fundamentals.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.