Please use a PC Browser to access Register-Tadawul

Get It

Evertec Dimensa Deal Shifts Brazil Exposure And Valuation Opportunity

EVERTEC, Inc. EVTC | 27.54 | +1.62% |

For investors watching NYSE:EVTC, this move comes with the stock recently trading at $30.21 and mixed multi year returns, including a 5.3% gain year to date and a 16.3% decline over three years. The transaction puts a spotlight on how EVERTEC is positioning itself within Latin American payments and financial technology services.

Acquiring Dimensa introduces new exposure to Brazil and adds B2B solutions across several financial segments, which could reshape how EVERTEC earns revenue over time. As regulatory reviews progress, investors may focus on integration execution, potential synergies and how the combined business might change EVERTEC's risk and opportunity profile in the region.

Stay updated on the most important news stories for EVERTEC by adding it to your watchlist or portfolio. Alternatively, explore our Community to discover new perspectives on EVERTEC.

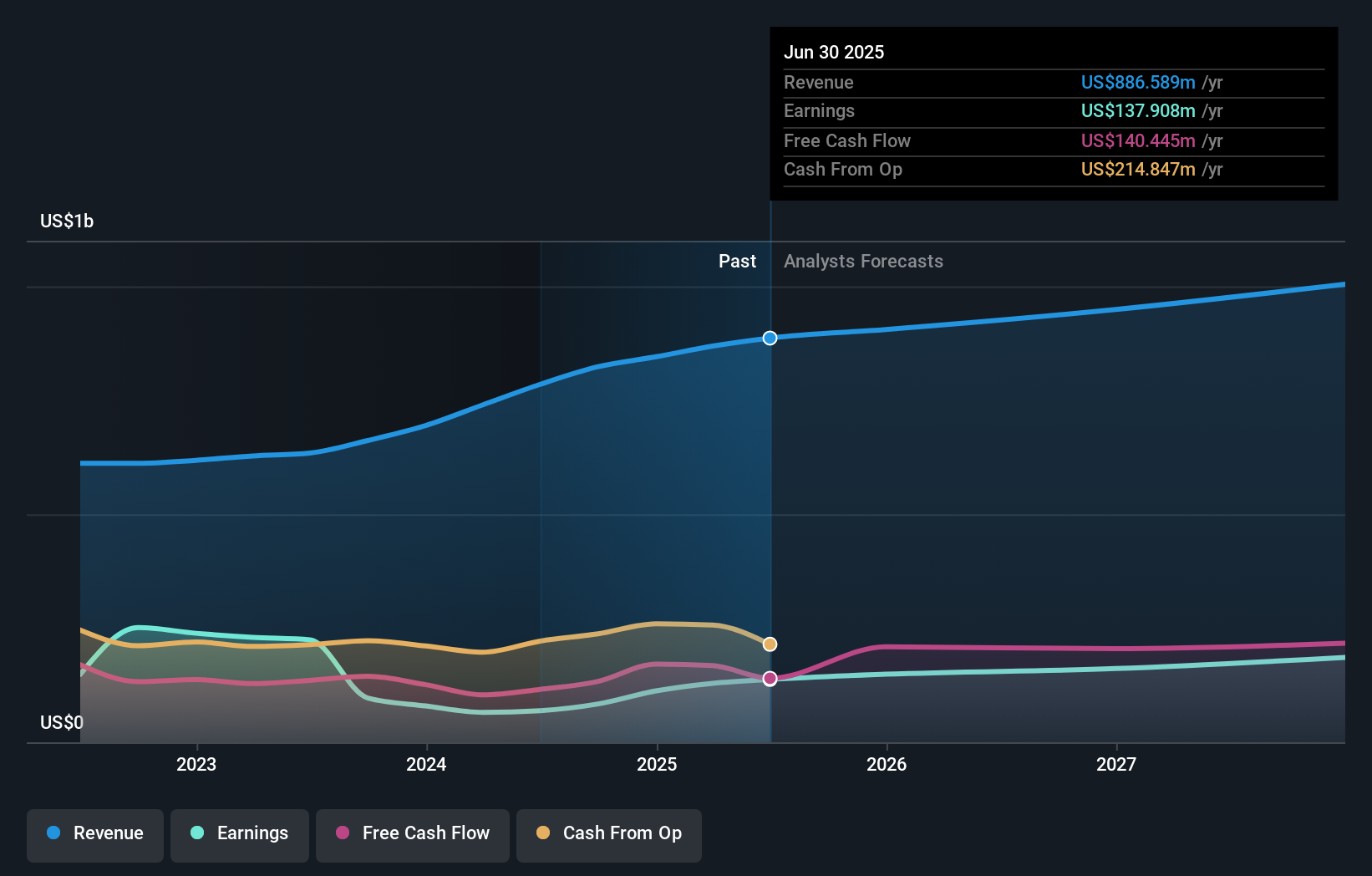

Check out Simply Wall St's in-depth valuation analysis for EVERTEC.

For a fuller picture including more risks and potential rewards, see the complete EVERTEC analysis.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.