Please use a PC Browser to access Register-Tadawul

Get It

Expedia Group (EXPE): A Fresh Look at Valuation Following Strong Q3 Results and Upbeat Guidance

Expedia Group EXPE | 228.37 | +0.32% |

Expedia Group (EXPE) delivered its third quarter earnings, showcasing year-over-year growth in both revenue and net income. The company also completed a major share buyback, declared a dividend, and raised its full-year outlook.

Expedia Group’s strong third quarter has clearly energized the market, with the share price climbing an impressive 26% over the past month. Momentum is building as investors responded positively to rising revenue, higher net income, and a series of shareholder-friendly moves such as the sizable buyback and dividend. This has pushed Expedia’s 1-year total shareholder return to nearly 47% and its 3-year total return to an eye-catching 167%.

If Expedia’s breakout quarter has you thinking about what other companies are catching investor attention, now is a smart time to discover fast growing stocks with high insider ownership.

But with the stock rallying and trading near its analyst price targets, the real question is whether Expedia Group remains undervalued or if investors have already accounted for all the company’s future growth potential.

Expedia Group’s most followed narrative places its fair value well below the latest close, suggesting the market is pricing in more growth than analysts anticipate. This dynamic sets up a critical debate around whether Expedia’s recent momentum can sustain such rich valuations.

Ongoing shift in consumer preference toward digital and mobile channels, paired with increased adoption of AI-powered search and personalization on Expedia's platforms, is driving higher conversion rates and improved retention. These factors may support sustained revenue growth and margin expansion.

Curious which bold financial forecasts justify this valuation? What could disrupt it? Dig into the full narrative to uncover the projections and the tensions underlying this contentious fair value call.

Result: Fair Value of $227.03 (OVERVALUED)

However, persistent weakness in the U.S. travel market or intensifying competition could quickly undermine these optimistic growth projections for Expedia Group.

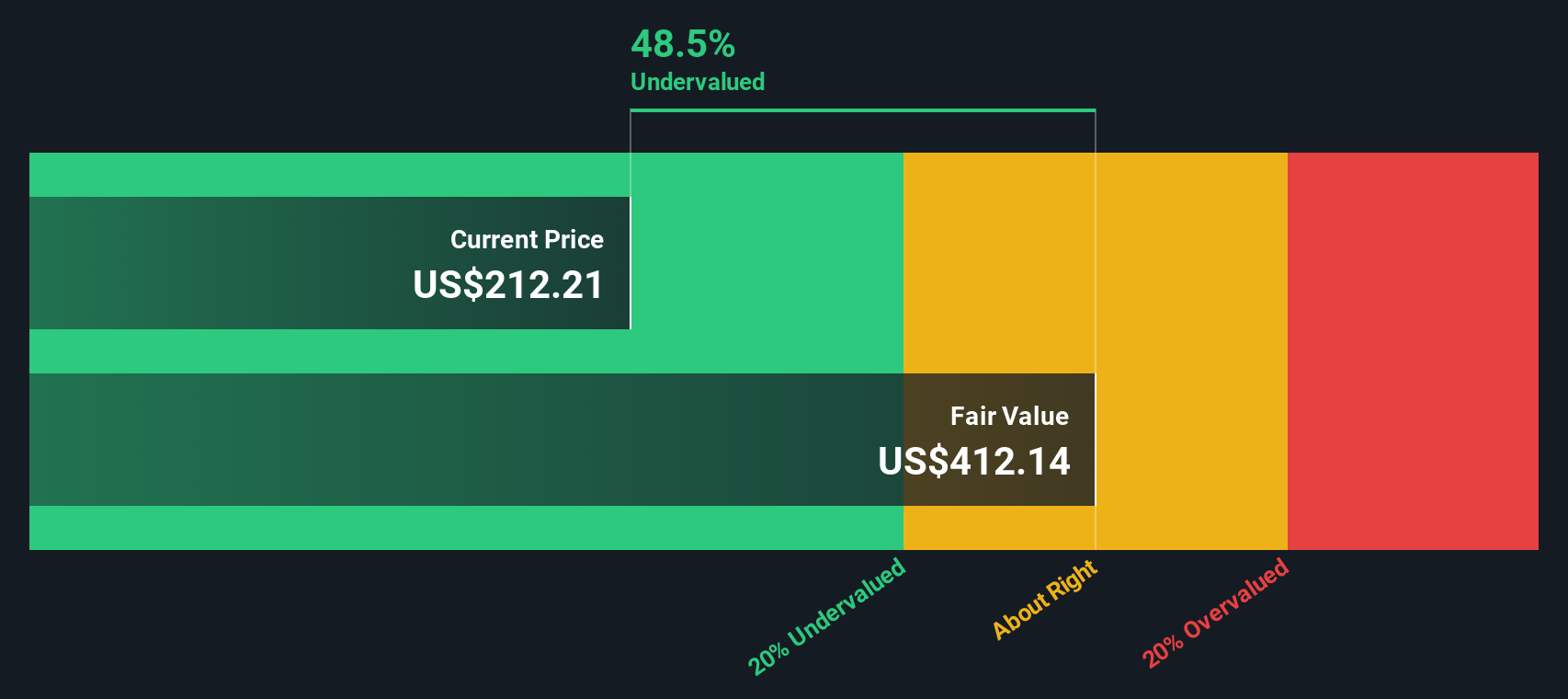

While most analysts see Expedia as overvalued based on traditional price targets, our SWS DCF model tells a different story. This approach estimates Expedia's fair value at $440.25, which is dramatically higher than its current share price. Could the market be discounting future growth too heavily?

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Expedia Group for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 855 undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

If you see things differently or want to dig into the data yourself, crafting your own view of Expedia Group is quick and easy. Just a few minutes is all it takes. Do it your way

A great starting point for your Expedia Group research is our analysis highlighting 3 key rewards and 1 important warning sign that could impact your investment decision.

Smart investors never limit their watchlists to just one company. Uncover fresh opportunities that align with your strategy and maximize your market edge today.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.