Please use a PC Browser to access Register-Tadawul

Get It

How a Surge in Analyst Upgrades and Options Activity Will Impact PDD Holdings (PDD) Investors

PINDUODUO INC. PDD | 111.96 111.96 | -0.01% 0.00% Pre |

Find companies with promising cash flow potential yet trading below their fair value.

To be a shareholder in PDD Holdings means believing in the company’s ability to pursue large-scale investment in its e-commerce ecosystem while still driving sustainable earnings and international expansion. The recent wave of analyst upgrades and options activity reflects stronger short-term optimism, but does not fundamentally shift the biggest near-term catalyst: whether PDD’s ongoing investments will deliver improved customer and merchant engagement before competitive intensity erodes margins further. The largest risk remains that heavy spending could pressure profits if financial returns from these investments are delayed or disappoint, this news does not materially change that risk profile.

Among recent developments, PDD’s August 2025 earnings announcement stands out as most relevant. Although sales climbed compared to last year, net income and diluted EPS both declined, showing the immediate profit impact of expansive ecosystem investments. This result puts the spotlight on whether analyst optimism is warranted, given the company’s willingness to accept margin pressure in pursuit of future growth. As investors weigh this, attention naturally turns to how quickly these investments can translate to lasting benefits for shareholders.

Yet, alongside the positive market momentum, investors should not overlook the risks tied to PDD’s ongoing commitment to large-scale support programs and what could happen if...

PDD Holdings is projected to achieve CN¥555.7 billion in revenue and CN¥147.1 billion in earnings by 2028. This outlook assumes a 10.7% annual revenue growth rate and reflects a CN¥49.2 billion earnings increase from the current CN¥97.9 billion.

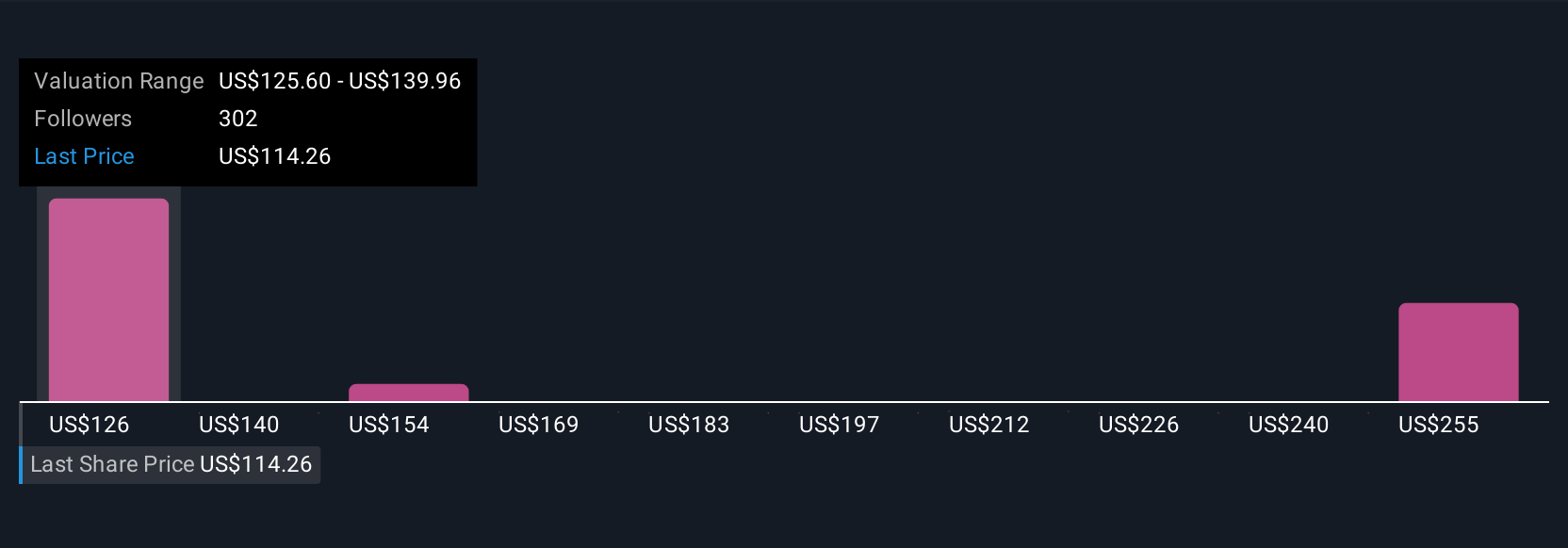

Uncover how PDD Holdings' forecasts yield a $143.36 fair value, a 14% upside to its current price.

With 21 individual fair value estimates from the Simply Wall St Community ranging from US$143.36 to US$354.52, investor views span a wide spectrum. As so many weigh PDD’s heavy long-term investments against short-term profit pressures, consider how sharply opinions can differ and explore several alternative viewpoints.

Explore 21 other fair value estimates on PDD Holdings - why the stock might be worth over 2x more than the current price!

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

Markets shift fast. These stocks won't stay hidden for long. Get the list while it matters:

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.